Executive Summary

Inflation expectations play a key role in many influential macroeconomic models. Commentators and policymakers often use the results of, or structures from, these models without delving too far into the underlying methodology. However, on closer examination, it becomes clear that the standard models of "inflation expectations" are sharply at odds with the underlying data. As such, great caution should be exercised when making policy recommendations in response to reports of elevated "inflation expectations." An unthinking reliance on these models may lead one to prefer tighter monetary policy than would be optimal for securing a robust labor market recovery.

Introduction

As the US economy continues to recover from the pandemic, commentators and policymakers alike have grown worried about the possibility of rising inflation and rising inflation expectations. These expectations may seem relatively harmless to a casual observer, but inflation expectations play a key role in many models used by policymakers, especially when assessing the need for tighter monetary policy and reduced fiscal support for the recovery. A number of different models argue that the simple expectation of higher future inflation will, by itself, bring that higher inflation into being. The trouble is, the evidence supporting these stories is very thin, and the causal structures implied by these stories are highly suspect. An over-reliance on these models risks a premature cutoff of monetary and fiscal support, choking off the recovery in response to a phantom threat.

As bottlenecks, slow re-openings, and capacity pressures have led to increases in measured inflation, measures of inflation expectations have risen as well. For example, survey measures have shown a sharp rise in consumers’ inflation expectations in 2021, while other measures - primarily market-based or those of professional forecasters - have risen only modestly.

Some commentators present these elevated inflation expectations as evidence that inflation might be here to stay, and that avoiding a return to the high-inflation regime of the 1970s will require sharp tightening of monetary policy. In their worst-case scenario, above-target inflation can “de-anchor” long-term inflation expectations and create a self-fulfilling spiral. While policymakers at the White House and the Federal Reserve have not fully embraced this view, they do consider rising inflation expectations a source of upside risk:

In monitoring the inflation outlook, the FOMC considers a variety of financial and economic data in order to gauge whether inflation expectations are consistent with meeting its inflation objective. Recent readings on these measures indicate that inflation is expected to return to levels consistent with the Committee’s 2 percent longer-run inflation objective after a period of temporarily higher inflation. That said, some measures suggest that the upside risks to the inflation outlook in the near term have increased.

The problem is, none of the arguments that purport to explain how inflation expectations themselves create higher inflation hold up to close scrutiny. The stories that link expectations to inflation are inconsistent with the patterns of observed inflation as well as the evidence on how households and firms respond to changing inflation expectations. Meanwhile, household and firm inflation expectations are often poorly informed, poorly anchored, and most closely map to changes in noisy and highly visible inflation components like the price of gas.

Without a clear and convincing causal line from inflation expectations to observed inflation, policymakers should not consider higher measured inflation expectations to be a justification for tighter policy. Instead, policymakers should focus on concrete measures and realized outcomes. Basing policy decisions on inflation expectations rather than labor market tightness and actual inflation will likely lead to an unnecessarily timid policy response as the recovery progresses.

Three Stories about Inflation Expectations

When commentators and policymakers worry that inflation expectations may create a self-reinforcing inflation spiral, they are often relying on one of three stories. While the causal mechanism is slightly different for each, they all share a certain family resemblance.

The first is a story about consumption timing. If consumers expect higher inflation, they may increase their consumption - especially of durable goods - in the present, so as to avoid higher prices in the future. In this model, consumers base their decision to trade off between consumption today and in the future on the real interest rate, of which expected inflation is a component. An increase in inflation expectations pulls future consumption to the present; this increases today’s prices by increasing today’s demand. Thus inflation expectations have created inflation.

The second story centers on the wage channel. On this account, workers care about real wages and keep expected inflation in view when bargaining over nominal wages. If workers expect high inflation, they will demand higher wages, which increases labor costs for the firm. The firm then passes these costs through to consumer prices, which validates workers’ original expectation of higher inflation. This narrative is often called the “wage-price spiral.”

The third - and wonkiest - story comes from the microfoundations of the expectations-augmented Phillips curve, the backbone of many modern New Keynesian models. In this narrative, firms are unable to smoothly and constantly change prices to a level consistent with profit maximization. The firms know this, and so raise prices periodically based on their expectations of inflation, as well as their expectations of how much competitors will increase their own prices. The higher a firm believes its competitors’ prices will be tomorrow, the higher it sets its own prices today. Higher inflation expectations thus create higher current inflation.

Further, any of these stories could be combined with the adaptive expectations theory of how inflation expectations are formed to create an inflationary spiral. After experiencing high inflation, economic actors develop high expectations of future inflation. These elevated expectations would feed back into their behavior, creating a vicious cycle. In the worst case scenario, inflation expectations watchers fear that long-term expectations, which have remained fairly stable throughout this inflationary episode, become “unanchored.”

If, however, inflationary expectations become untethered from that target, prices may rise in a more lasting manner. This sort of inflationary, or “overheating,” spiral might then lead the central bank to raise interest rates quickly which then significantly slows the economy and increases unemployment. Economists refer to this scenario as “a hard landing,” so inflationary pressures are risks that must be carefully monitored.

Since the causal mechanisms for each story are broadly similar, their individual failures to fit the facts are similar as well. The first story falls flat on empirics: despite the fact that consumers largely do not or cannot consistently pull forward durable goods consumption, inflation is still most prominent in those goods. On the second, there is copious evidence that workers no longer have the bargaining power to ensure that wages keep pace with inflation, especially over the multiple iterated negotiations required for a full wage-price spiral. For the third, the empirical behavior of firm inflation expectations is far more volatile than observed inflation, indicating that that particular transmission mechanism is weak or nonexistent.

If premature tightening is going to be justified by high reported inflation expectations, we should demand a careful accounting of why exactly these expectations are so worrying. Otherwise, policymakers risk overreacting to a phantom threat at a critical juncture in the recovery.

Story #1: Do consumers bring consumption forward? Can they?

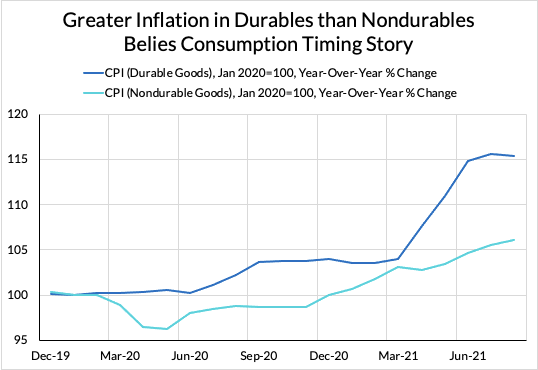

In the consumption story, households expecting higher inflation move some future purchases into the present to take advantage of the relatively lower prices. If all households do this, the boost in near-term demand from higher inflation expectations creates higher inflation in the present. However, only so many purchases can really be substituted across time: the purchase of a new car or refrigerator can be moved far more easily than the purchase of a head of lettuce or gallon of gasoline. Were this story to play out in real life, we would expect higher inflation expectations to drive a larger increase in purchases of - and thus sharper inflation in - durable goods, rather than in nondurables and services.

But for this story to work, households have to have the financial ability to shift future consumption earlier, whether through cash on hand or access to borrowing instruments. Research has shown their ability to do so is limited: around a third of households are “hand-to-mouth”, meaning they hold very little liquid wealth and have little ability to pay for increased present consumption. Despite the depressed consumption and substantial government support over the course of the pandemic, these findings still mostly hold today. While household assets (including liquid assets) have increased, the amount of “excess savings” remains small and the gains in net worth have not been evenly shared.

What evidence we do have suggests that the consumption story is off base. In a recent paper, researchers provided a random subset of households with information about monetary policy and inflation, measured their changes in inflation expectations, and tracked their consumption afterwards. The authors found that households increased consumption of nondurable goods and decreased consumption of durable goods when given information intended to raise their inflation expectations. This is consistent with the consumption patterns observed in 2021, but strongly at odds with the thesis that households will pull consumption of durable goods forward when they believe prices will rise in the future.

Recent data also puts the lie to this first story. At the same time that durables consumption has been falling, it is durable goods - not nondurables - that have driven recent elevated inflation readings. If the recent increase in inflation could be explained by changes in consumption behavior, we would expect to see the opposite–the price changes should follow the quantity changes. Rising prices on a constant consumption of durable goods does nothing to validate the overall consumption story.

Finally, even if households could cause current inflation by bringing forward their consumption in anticipation of higher inflation, it is hard to see how this could result in an inflationary spiral. Assuming households could and did respond to elevated inflation expectations by bringing consumption forward, they cannot do so indefinitely. At some point, household savings and borrowing capacity would run out. The subsequent fall in consumption afterwards should, by the same logic, depress inflation in the future, thereby choking off the cycle.

Story #2: Could Inflation Expectations Trigger a Wage-Price Spiral?

It is often asserted, without much evidence, that elevated inflation expectations alone could kick off a wage-price spiral. In this story, households expect inflation and bargain wages upwards, which raises costs for businesses who then pass these on as higher prices, which validate households’ original raised inflation expectations. Fears of a wage-price spiral have been raised time and again since the post-financial crisis recovery without ever coming to fruition. For this pathway to represent a real inflationary threat, there must be sufficient pass-through from inflation expectations to wages, and then back again from wages to prices. Without this, any inflationary spiral would be short-lived.

First, the story is inconsistent with the literature on household inflation expectations. Households tend to associate high inflation expectations with worse economic outcomes, such as lower household income and higher unemployment risk (Kamdar 2018, Coibion et al. 2019). These elevated inflation expectations should be assumed to lower - not raise - the wage workers are willing to accept, since households anticipate turbulent economic times ahead.

Second, the wage-price spiral requires workers to have far more bargaining power than we see evidence of today. The story assumes that workers with elevated inflation expectations can simply “demand higher wages”, skipping over any explanation of whether or not those demands would be met. Unionization rates in the United States are at an all-time low. In the past few years, we have also seen historically low unemployment rates fail to produce the expected dramatic upward wage pressures, leading to Chair Powell’s famous line that “to call something hot, you have to see some heat.” Beyond that, a large literature in labor economics shows that the rent-sharing elasticity, a measure of how much wages respond to changes in a firm’s value-added per worker, is very low (see Card, et. al (2018) for a review of the literature).

Finally, there is little empirical evidence directly linking wage increases to price increases. This part of the story is the most theoretically appealing: after all, labor makes up a large part of production costs, and it’s easy to imagine firms passing on rising costs through prices. Despite the fact that nominal wages and prices move together over the long-term, there is scant evidence that the two imminently predict each other. The literature generally finds that wages offer little to no additional power in predicting price inflation.

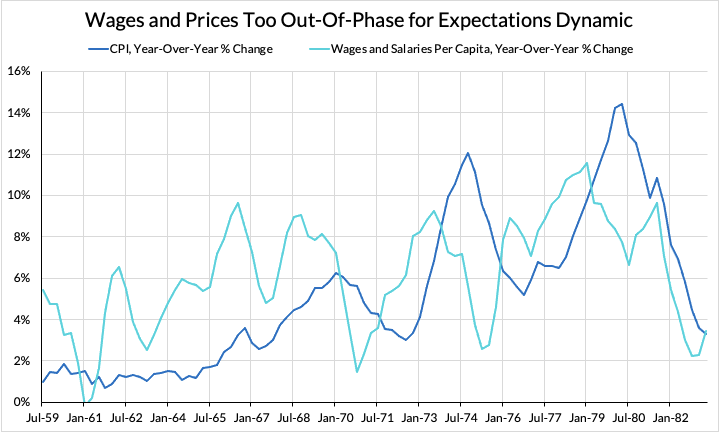

Labor markets and inflation ultimately have less to do with each other than textbook Phillips Curve dynamics would suggest. Even in the 1970s, often cited as a classic case of the wage-price spiral, it is hard to see the claimed tight connection between wages and prices:

Story #3: Inflation Expectations and New Keynesian Theory

The third story originates within the microfoundations of the “expectations-augmented” Phillips Curve, a core component of modern New Keynesian macroeconomics. These New Keynesian models are hugely influential beyond academic economics and often - whether they know it or not - inform the underlying framework used by policymakers and commentators generally. In fact, undergraduates generally learn a simplified version of this model, with the granular details and exact mechanisms often glossed over. Since these ideas are clearly in the intellectual groundwater, it is important to dive into the microfoundations of the expectations-augmented Phillips Curve to see how plausible this story really is.

In New Keynesian models, the inflation expectations of price setters within firms play a key role in determining current inflation. Since these firms are assumed to be unable to constantly and flexibly change prices to a profit-maximizing level, they set prices based on their own inflation expectations. When firms expect higher inflation in future, they raise prices today so as to avoid being stuck with excessively low prices as compared to future costs, and create higher current inflation. This dynamic is so powerful in textbook New Keynesian models that inflation moves almost one-for-one with expected future inflation.

Hazell, et. al (2021) illustrates well the power of inflation expectations in modern New Keynesian models. The standard Phillips Curve is estimated by looking at cross-sectional variation in inflation and unemployment rates. To add a measurement of expectations to the standard Phillips Curve, the authors use a time fixed-effect model to control for changes in long-term inflation expectations. They find that the Phillips curve becomes far flatter with the inclusion of time fixed-effects, which they claim indicates that much of the apparent inflation-unemployment tradeoff of the Phillips curve can really be explained through changes in inflation expectations. Rather than the unemployment-inflation tradeoff of traditional Phillips Curve models, almost all the action is in “inflation expectations.”

This finding leads them to offer a revised account of the American economy in the 1980s. Since they claim that “inflation expectations,” rather than an inflation-unemployment tradeoff, are the central determinant of current inflation, the traditional story no longer makes sense. On their reading, the inflation of the 1970s ended not because Volcker was willing to tolerate massive unemployment, but because Volcker was able to successfully shift long-term inflation expectations.

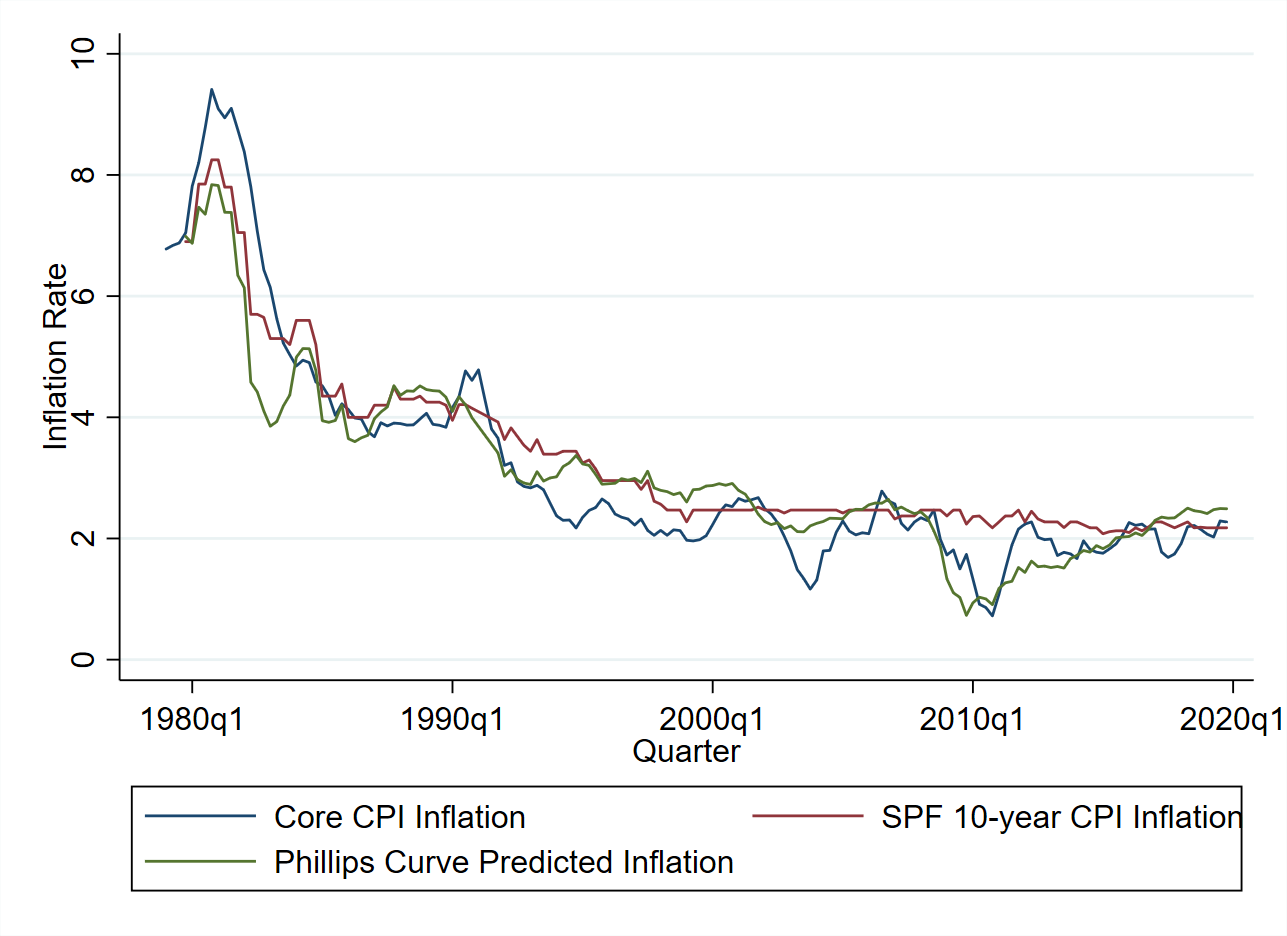

To argue this point, the authors combine their estimates of the coefficient on the unemployment gap with 10-year-ahead inflation expectations from the Survey of Professional Forecasters, and show that combining the two in a Phillips Curve dynamic produces a data series that fits the Core CPI Inflation series well. Using the same data, I’ve created a version of their dataset below:

Their argument is simple and the data above doesn’t contradict it. Inflation expectations were high in the 1980s, which produced high inflation. As those expectations declined, inflation followed. Afterwards, inflation expectations were stable, and so was inflation. In this story, changing inflation expectations alone are capable of explaining the falling, then stable, inflation of the 1980s and 1990s. Compatible curves seem evidence enough.

While this is a nice story, there is no obvious proof of which direction causality runs. The long-run changes in inflation are consistent with the inflation expectations story, but they are equally consistent with a story where changes in current inflation drive changes in long-run inflation expectations.

Even worse from the perspective of those who must make policy decisions today is the fact that the incredible stability of inflation expectations (as measured by the mean Survey of Professional Forecasters (SPF) forecast) provides little basis for forecasting or explaining changes in current inflation. Even if inflation expectations were in fact responsible for the difference between the 1980s and today, the available data provides little ability to detect these changes in real time. Despite the spike in inflation in the second quarter of 2020, SPF inflation expectations have barely moved from where they were in 2017-2018.

However, all these issues elide an even deeper theoretical problem for story #3. Inflation expectations as measured by the mean SPF forecast (the method used by Hazell et. al.) behave dramatically differently from the inflation expectations of price setters in firms. The choice of instrument has substantial implications. In Candia, Coibion and Gorodnichenko (2021), researchers fielded a survey of inflation expectations of U.S. CEOs and found that the inflation expectations of firms are much more unanchored than those of professional forecasters. This is true across a number of different metrics: firms expect inflation much higher than the target rate, they have high dispersion and low confidence in their predictions, they make large revisions, and their short-run and long-run expectations move closely together.

If inflation really moved one-to-one with the inflation expectations of price setters in firms, the evidence suggests that we should see wide and much more frequent swings in measured inflation. The fact that we don’t suggests that the evidence for this intuitively-appealing story is thin at best. Worse, the SPF measures used by many of these papers, as surveys of forecasters rather than firms or households, don’t even provide the kind of evidence necessary to test the New Keynesian theories themselves.

All of this raises a key issue for those looking to use inflation expectations to inform monetary policy: whose inflation expectations are relevant, and how can those expectations be influenced, if at all? There is a key disconnect in story #3: the exact actors whose inflation expectations need to be anchored in order to explain low and stable inflation have unanchored expectations.

How Should Policy and Commentary Respond to Inflation Expectations?

Although inflation expectations are often invoked to justify premature policy tightening, the causal stories behind this invocation are often full of holes. If inflation expectations are to be a useful metric for gauging the economic outlook, one needs to first be clear about how and why these expectations would exert an economic force, and then provide evidence of that force. It is a mistake to tighten policy and hamper the labor market recovery without clear and convincing proof of an inflationary threat.

It is also critical to remember that household and firm expectations of inflation are poorly informed and poorly anchored. Both respond to changes in expectations in counterintuitive ways. As shown above, firm expectations swing wildly with business sentiment, while household inflation expectations can be explained mostly through changes in the prices of salient but volatile economic indicators, like the price of oil. In Killian and Zhou (2020), the authors find that the increase in inflation expectations in the early 2010s can be explained almost entirely by gas prices. Basing a policy response on these expectations therefore risks tying the pandemic recovery to transitory shocks in noisy indicators.

Rather than chasing phantom stories about inflation expectations, policy should rely on realized measures of the state of the economy, such as actual inflation readings or measures of labor market tightness. Otherwise, monetary policy risks overreacting to inflationary threats that aren’t really there. Responding to these phantom threats risks prematurely cutting off a recovery as American households, businesses, and workers continue to rebound from the pandemic.