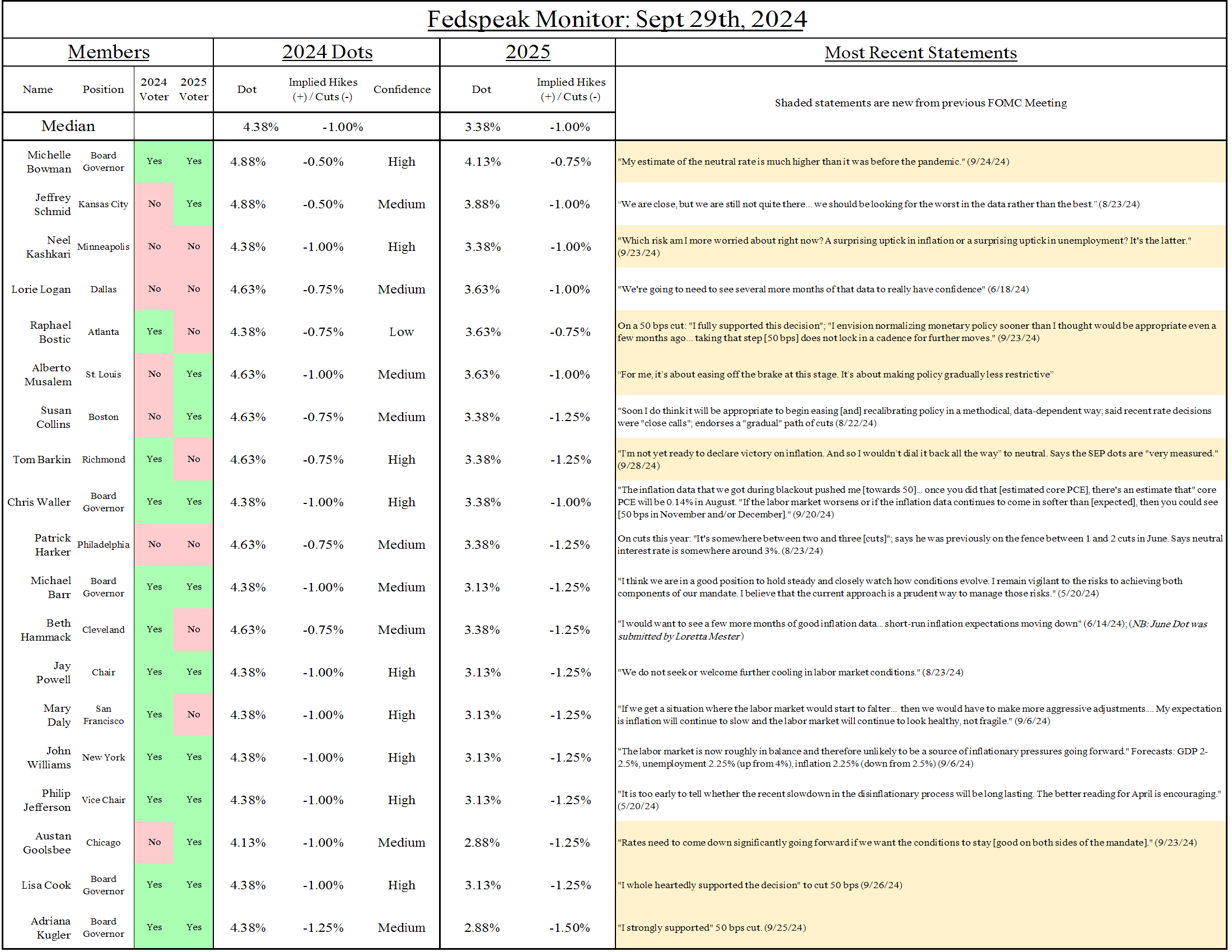

With labor market risk rearing its head, Kashkari and Bostic sound dovish again.

Kashkari revealed his personal dots in an essay this week: 100 bps of cuts this year, 100 bps of cuts next year, and a 2.9% long-run federal funds rate (the Committee median). He's more worried about the labor market risk ("I look forward and I think, which risk am I more worried about right now? A surprising uptick in inflation or a surprising uptick in unemployment? It's the latter"), but even if he thinks the long-run rate may have risen, he's happy to frontload cuts now and then feel out neutral by going slower later—exactly the strategy we've endorsed.

Bosticsounds encouraged by the latest inflation data, especially in supercore services, and is willing to go faster if the labor market worsens: "Any further evidence of material weakening in the labor market over the next month or so will definitely change my view on how aggressive policy adjustment needs to be."

MusalemandBarkinare less in a hurry to lift restrictions. Musalem is worried that the economy would react "very vigorously" to financial conditions loosening and thinks the risks between over and underheating are "roughly balanced." Unsurprisingly, Cook, Goolsbee, and Kugler came out in strong support of the 50 bps cut move.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.