Ten Thoughts On The Tribal “Transitory” Debate As We Enter 2024

There will be a time and a place for a more thorough retrospective of this still-unfolding (dis)inflationary episode, but it would be premature to make strong declarations at this juncture. We should all be thrilled by the past 6-7 months of inflation data, but it is ultimately only 6-7 months of data with plenty of scope for future bumps in the disinflationary road. Patience is a virtue, as impulses from supply- and demand- shocks have lasted longer than were initially predicted, and many key dynamics still remain at play. The subsequent economic trajectory—for better or for worse—will inevitably re-color our perspective on the past four years. We enter 2024 with a deep sense of gratitude and an aspiration that we're sure many of you also share: to exit the insufferable tribalism of the “transitory” debate.

It’s easier to take uncharitable strawmen views of your opponents’ claims, but harder to introspect about your own forecasting errors. There were many aspects of this inflation and macroeconomic episode that drastically surprised us and which have (hopefully) humbled us. We also know that the future shapes our understanding of the past, and there is much we will still learn from the coming year that recasts what we thought we knew about 2021 through 2023.

Macro data and episodes are inherently sparse and it all becomes a kind of small sample size theater. That's why it's important to reckon parsimoniously with all of the macro facts of the past 3-4 years. We are all vulnerable to convenient cherry-picked and univariate assessments, but if we are not going to go in circles with confirmation bias, we have to diligently and holistically learn from forecasting errors, both of the outright and conditional variety.

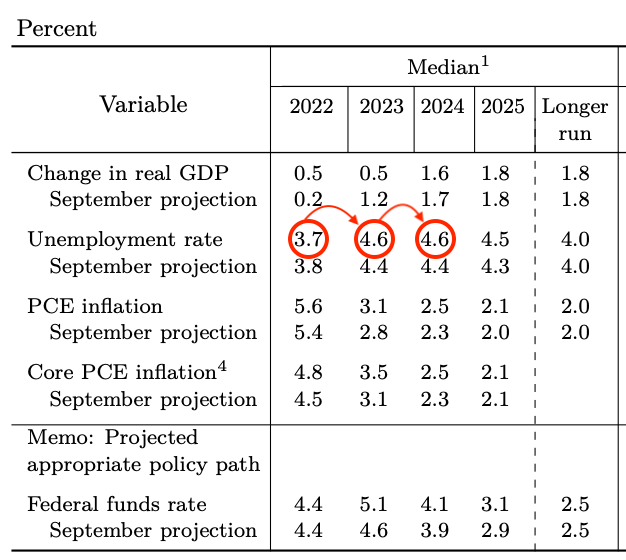

Growth proved to be highly resilient in 2023, and to Chair Powell’s credit, his assessments shifted opportunistically. In September 2022, he was claiming there was no way to bring down inflation that would be painless to the labor market and that unemployment would necessarily have to rise. In June 2023, he recognized that resilient growth was a blessing, not a curse, in the effort to achieve a soft landing. In September 2023, the rest of the FOMC was sending the same message in their projections.

The pivot in the Fed’s internal perceptions has helped. The pressure to dogmatically hike eased up. Supply has had a chance to “catch up” to consumer demand in the United States, which proved to be more immediately insulated from Fed hikes than most predicted. This story is a great one, but also stands in marked contrast to what is transpiring right now in central Europe, where supply shocks and monetary tightening have weighed on economic activity before supply has had a real chance to recover.

The only thing worse than an ugly tradeoff is a misperceived one. If more policymakers can see how inflation is resolvable without resorting to policies aimed at higher unemployment, the implications can be generationally transformative. Such an outcome is far from secure. A lot still has to go right, including forces that go beyond economics. But at least in January 2024, that possibility remains alive and kicking. To the extent central bank patience can be paired with more supply-side monitoring and root-cause policy remedies, navigating business cycle tradeoffs will come with fewer long-term costs over the coming decades.

While the causal source of inflation and the relative breadth of inflation might both be related to matters of timeline, labor market slack, and inflation expectations, they are both ultimately separable dimensions of inflation analysis. (For those who like to think in terms of linear algebra, they are not orthogonal to each other, but they are linearly independent).

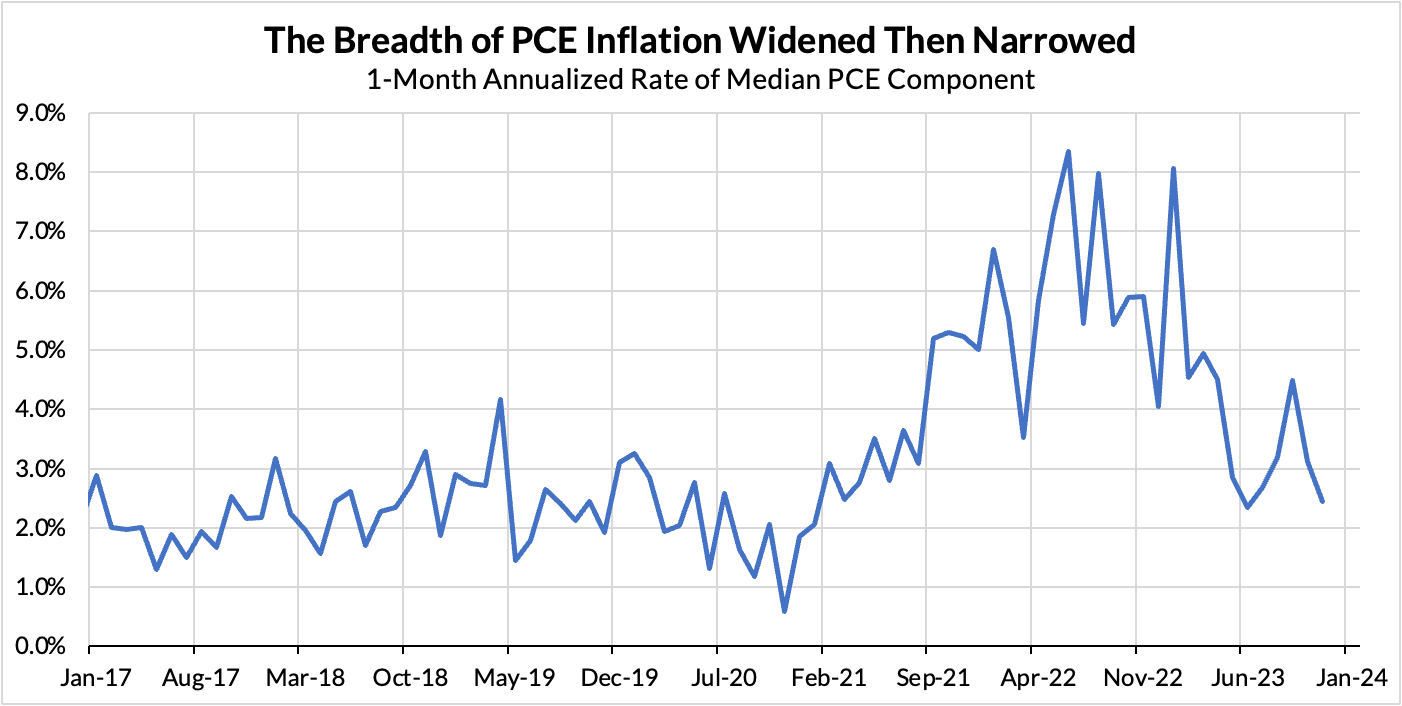

Causal sources of inflation will always be debatable, but the breadth of inflation is a simple matter of fact. Inflation first spread from “narrow” to broad-based only to show increasing signs of narrowing again. Time was confused with breadth, but they are different dimensions.

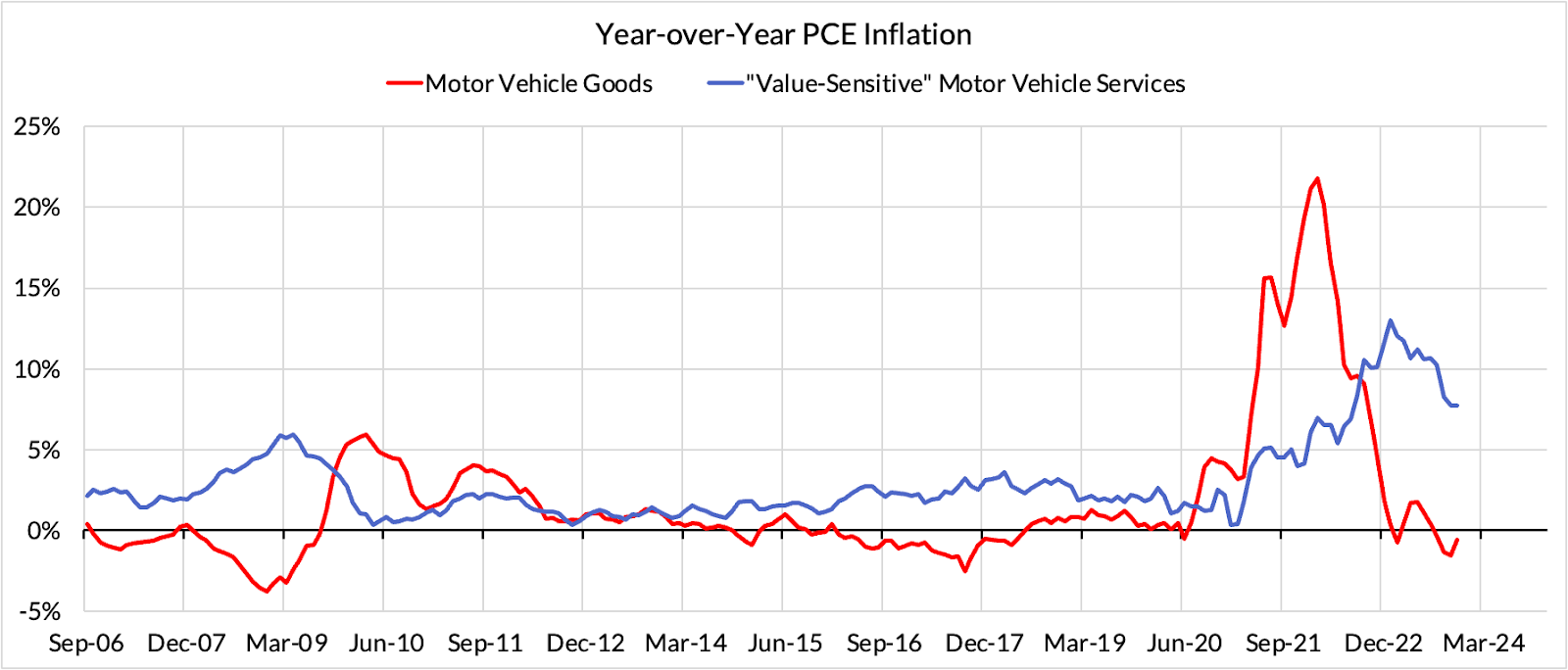

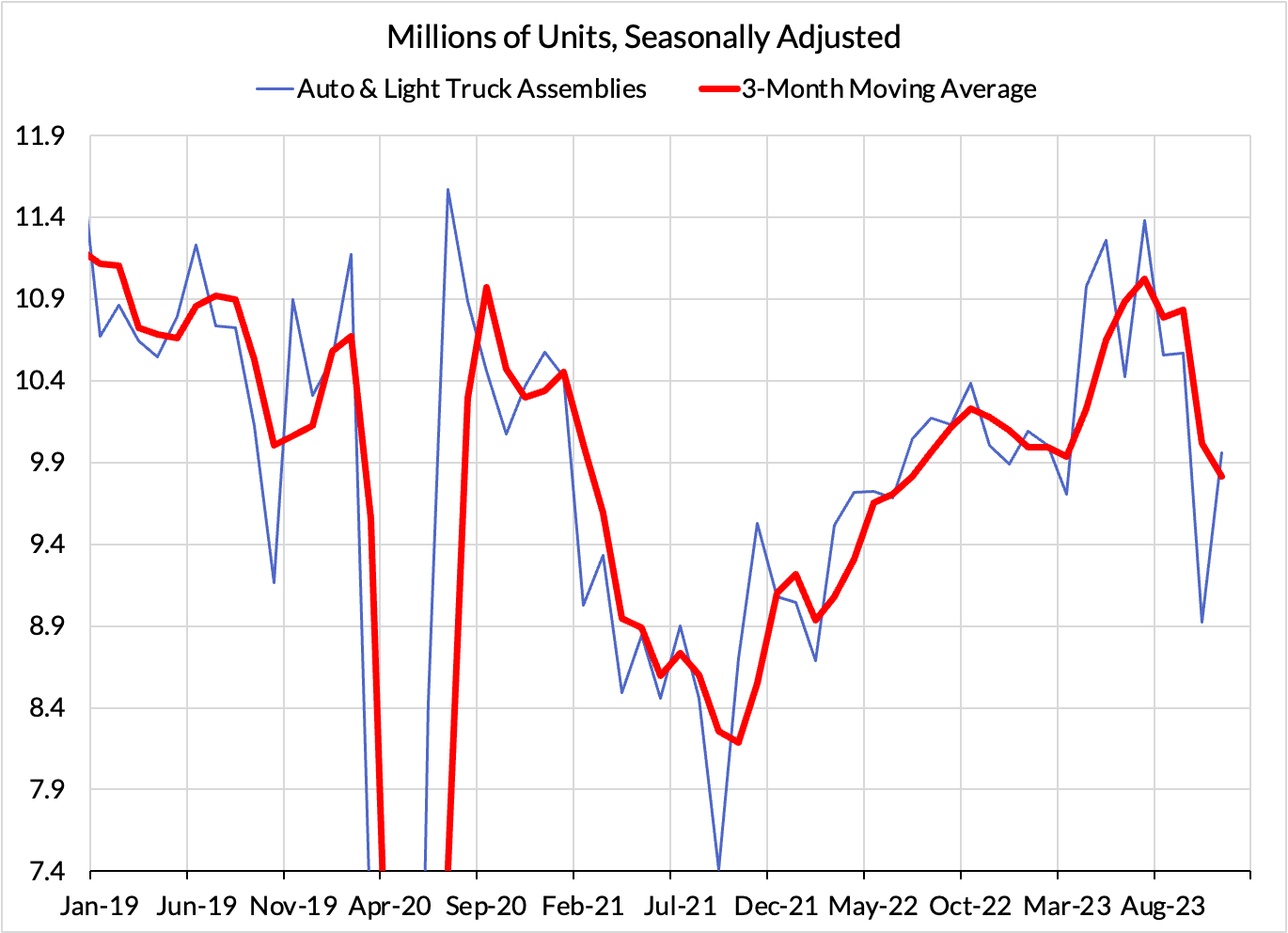

Many of the initial reasons for inflation to ultimately revert lower were rooted in the idea that narrow price spikes (that were not reflected in trimmed mean or median aggregations of inflation) driven by supply phenomena (e.g. automobiles) would fade quickly. With the benefit of hindsight, these reasons were both bad and totally wrong. Local supply dynamics persisted far longer than virtually anyone predicted. Motor vehicle production only began to achieve something close to pre-pandemic levels of production after more than 2 years, with plenty of lost stock to catch up on. It’s also true that the initial narrowness of inflation was a bad predictor of future inflation breadth. Inflation grew more broad-based over the course of 2021 and 2022.

Errors could be found on the other side of the fence too: so much of the inflationary upswing could be found in a broad range of CPI and PCE categories, last for a long time, and yet be attributable to supply and ultimately revert. This is not a statement about the entirety of inflation dynamics, but supply does appear to be a highly substantial explanation for 2023 disinflation. You can’t have accelerating and relatively rapid growth in real consumption, output and productivity alongside disinflation, without a major role for improving supply. The historic nature of this coincidence makes no sense in the absence of understanding the role of adverse supply shocks in previous years that finally began to unwound. And even when thinking about supposedly “narrow” supply shocks affecting used car prices, the effects were broader: a persistent production shortfall of motor vehicles affects the prices of new vehicles and parts, along with the prices of value-sensitive services (rental, leasing, repair, maintenance, insurance).

Even “demand” as an explanation had multiple dimensions. Some dimensions of demand were viewed to have “one-time” effects while others were said to persist more indefinitely. Here too, predictions about timelines and scales were underestimated ex-ante, but most of these phenomena look more time-limited. The role of the pandemic, reopening, fiscal policy, and monetary policy need to be carefully disentangled.

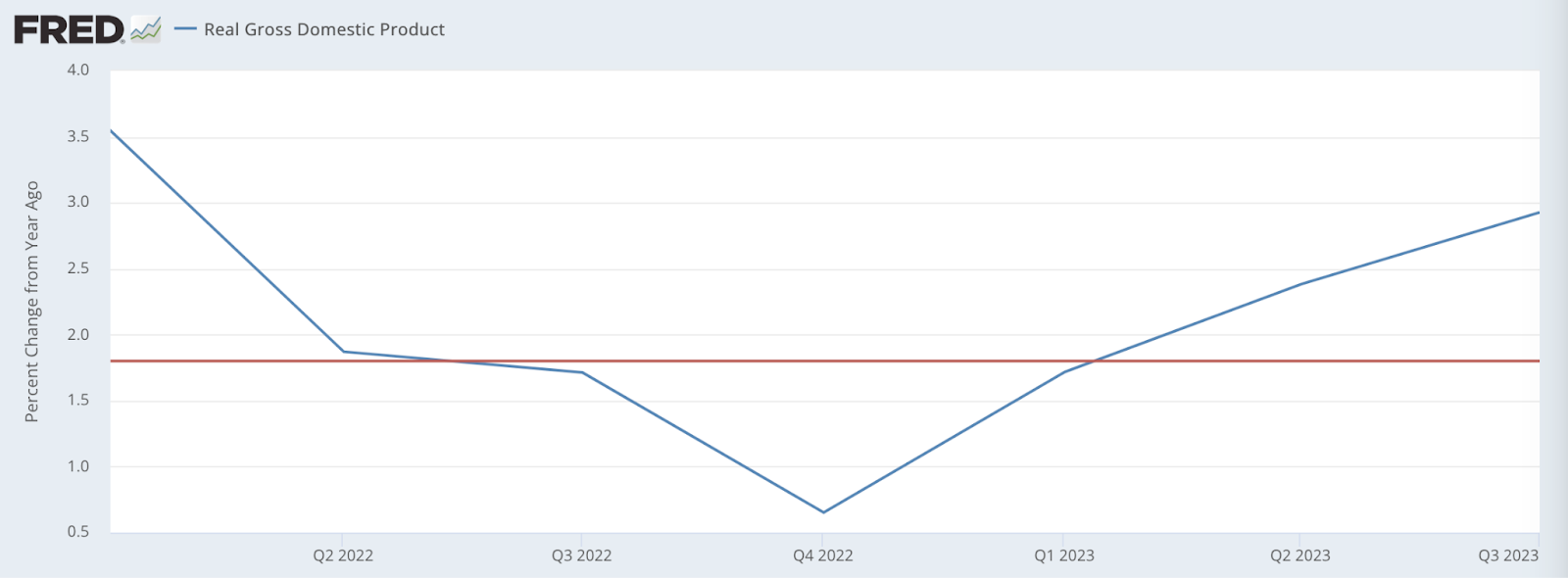

Supply is hidden in the error terms of the New Keynesian macroeconomic model, which instead views labor market slack and inflation expectations as the central forces behind inflation dynamics. But 2022 and 2023 reveal why it’s important not to sideline supply. Over the previous four quarters, real output and productivity grew in a manner that substantially outperformed 2023 expectations and the pre-pandemic trend. Most people did not anticipate that real GDP would grow at 3% year-over-year over the last four quarters.

Gabriel Chodorow-Reich made a tongue-in-cheek criticism of the Fed for penciling in “Immaculate Disinflation” in their projections. Yet it takes even more immaculate thinking to make sense of accelerating above-trend real GDP and productivity growth, unless there is some appreciation for the scale of supply shocks that hit the economy in 2021 and 2022. The resilience and local re-acceleration of growth in 2023 makes more sense in the context of supply shocks unwinding, with commodity markets normalizing, automobile production recovering, and global pandemic normalization from Covid-era policies all playing their part.

Was all of the inflation about supply shocks? Heck no. We had some big demand forces at play too, and made some segments of inflation inevitable even if supply-side inflation was completely abssent.

Start with the effects of reopening the economy: risk-preferences associated with in-person services substantially eased, as did the institutional constraints for accessing them. That was going to show up first and foremost as a demand shock, one in which consumers were likely ready faster than businesses and workers. The surge in in-person services demand was inevitably going to be asymmetrically strong relative to the drop-off in goods demand.

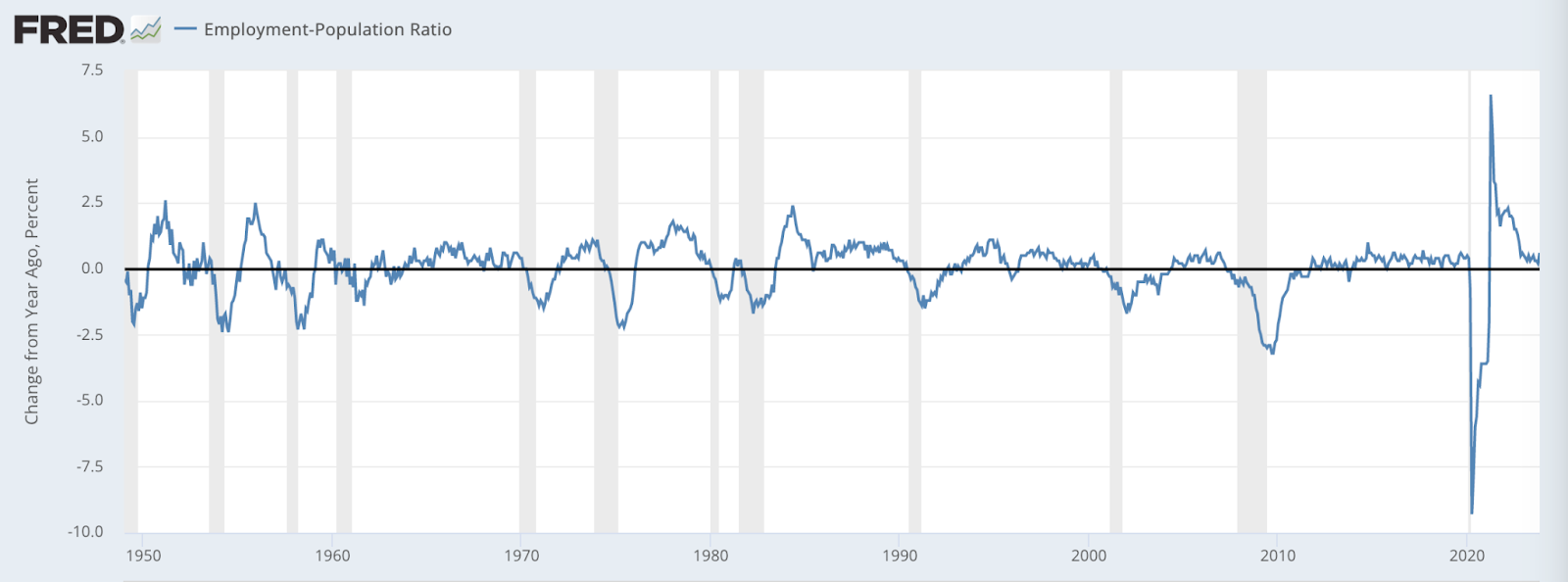

On top of this, there was the sheer force of bringing millions and millions back into the labor market, almost instantaneously. The surge of job growth in 2021 and early 2022 meant millions of people earning market incomes again and a corresponding boost to spending. A transfer is a helpful benefit for smoothing consumption but a new income is always more powerful. The St. Louis Fed will eventually need a y-axis adjusting function for FRED, simply because 2020 and 2021 outcomes were off the charts.

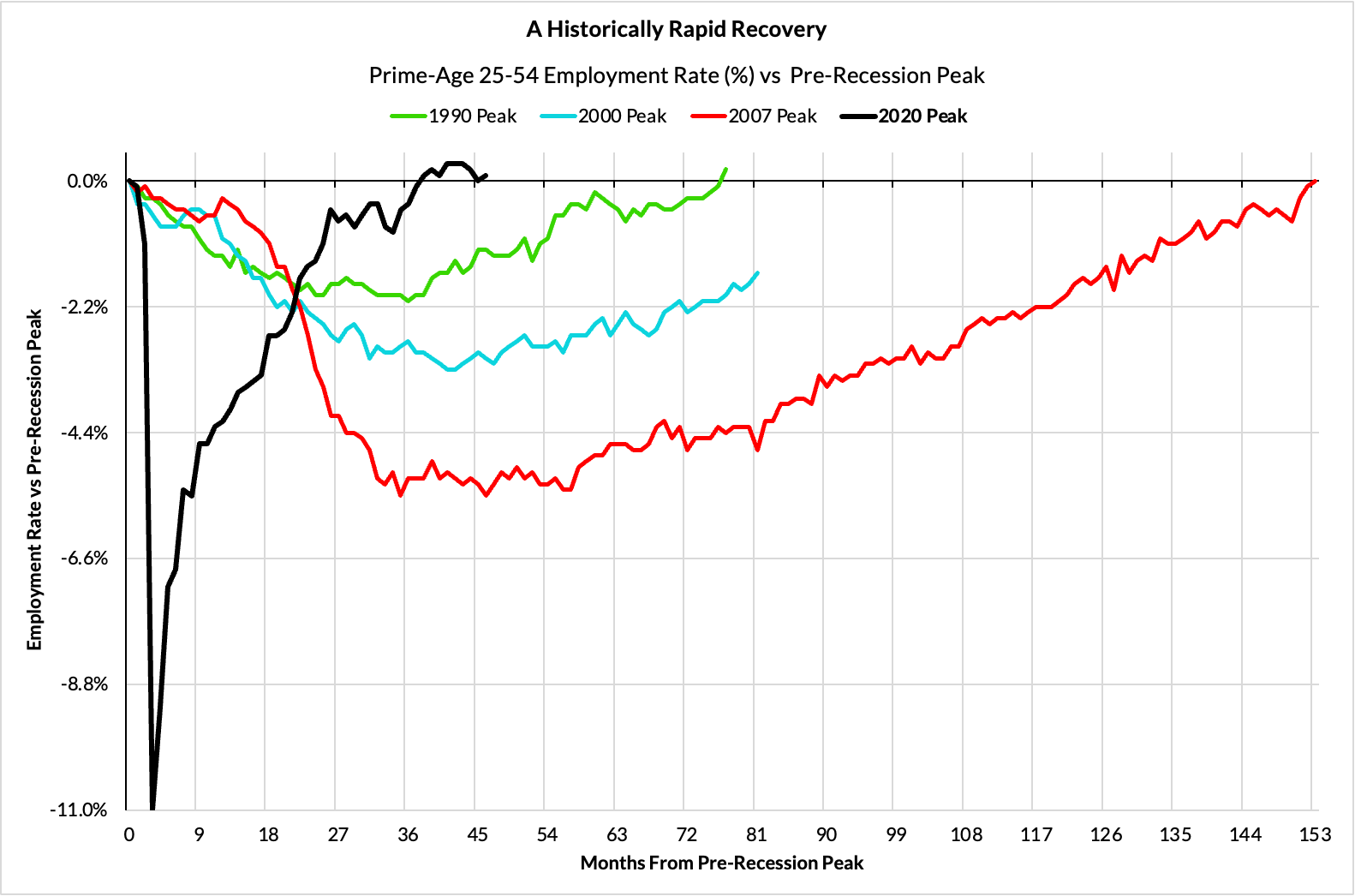

To be clear, the surge in job growth is a demand-effect worth defending. To secure a swift recovery in the *level* of labor utilization–which was secured–a surge in job growth was required. Enacted fiscal tailwinds from 2020 and 2021 added to these demand effects in tangible ways. They added to consumption demand as the economy was still in the midst of transitioning out of the pandemic, and fueled labor demand secondarily.

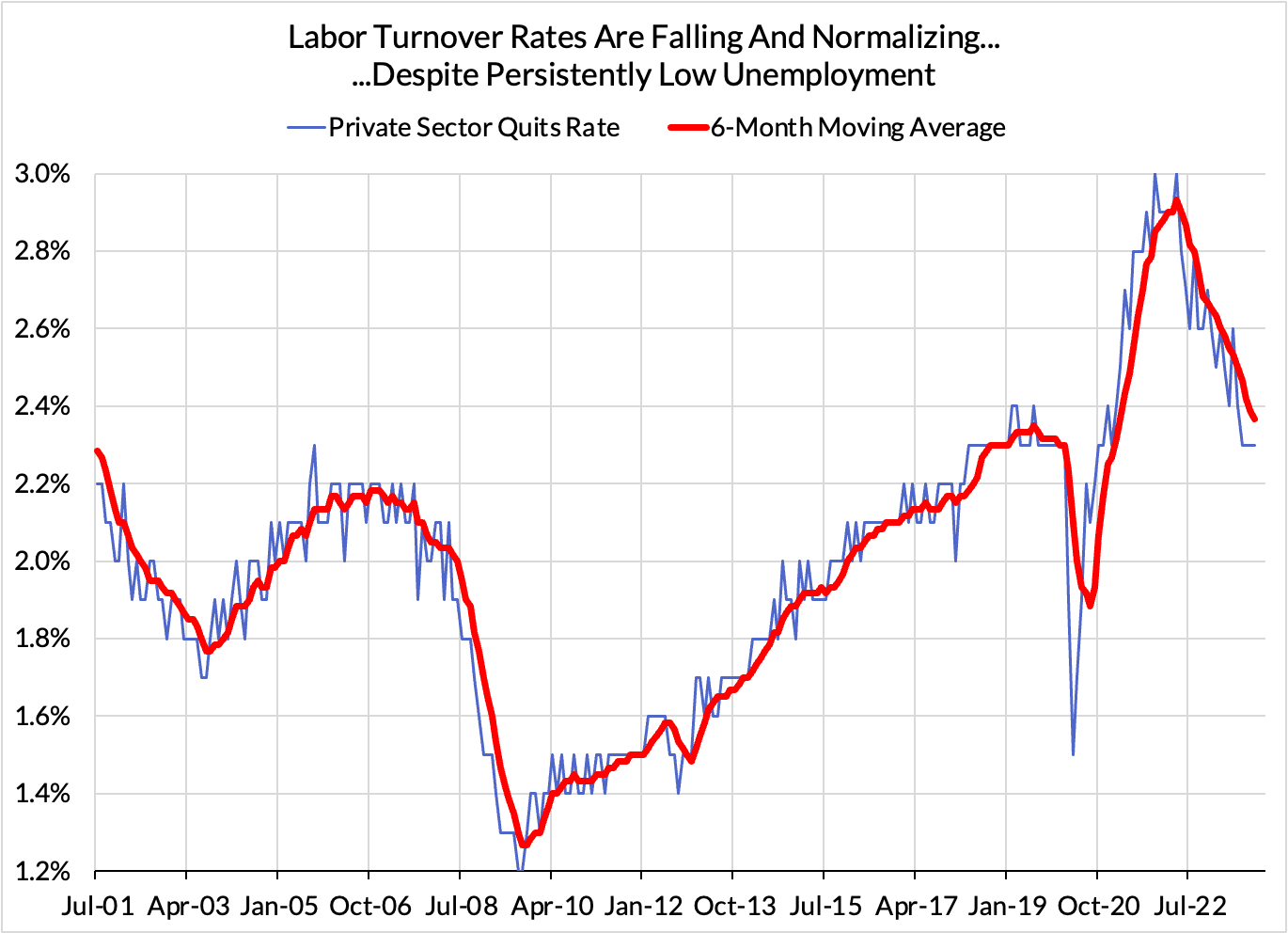

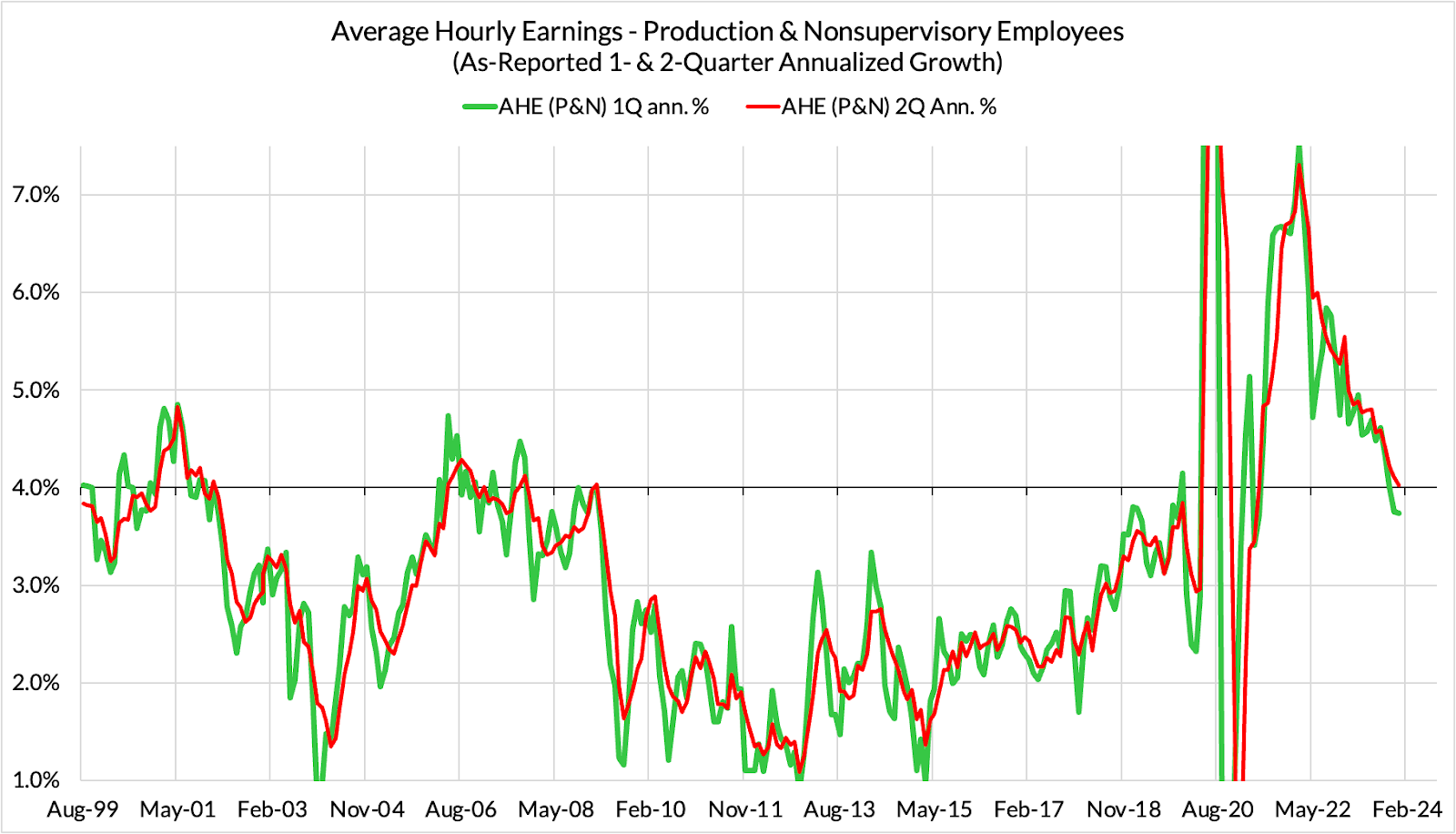

In the process of achieving strong job growth, the economy also saw record rates of voluntary labor turnover, along with upward pressures on search costs and wages.

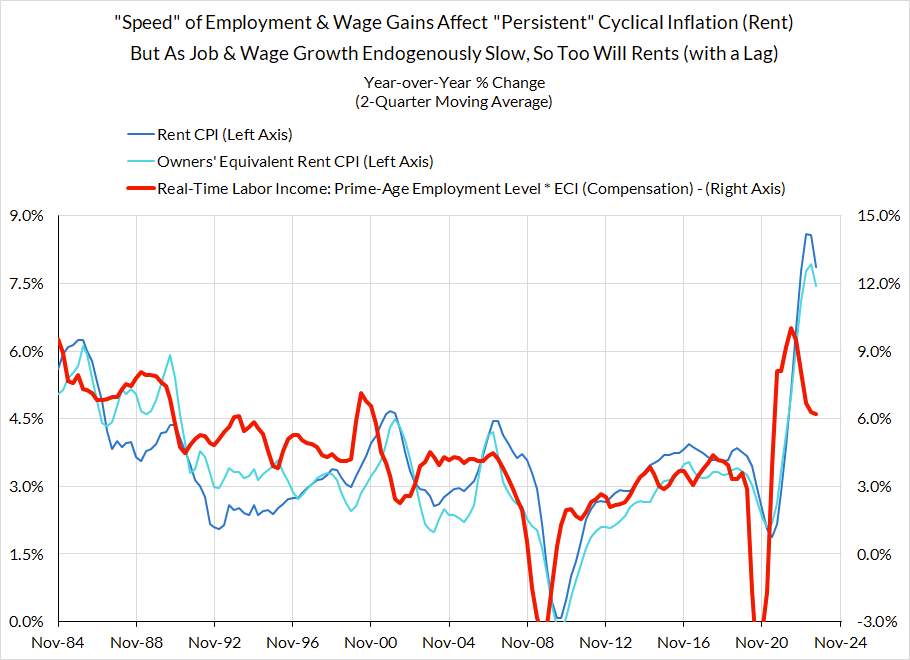

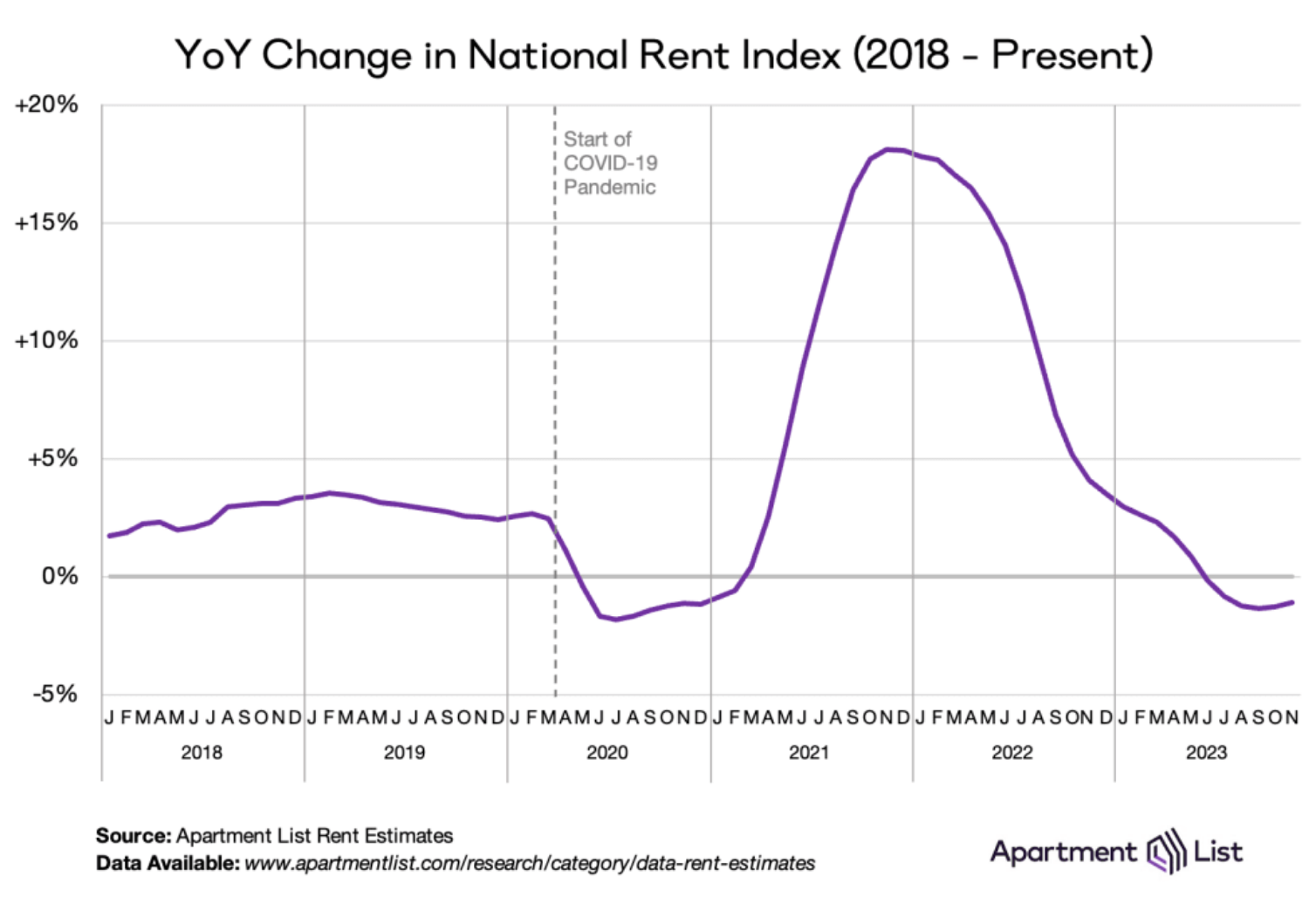

Strong labor income growth tends to coincide and foretell strong market-rent growth in the present, as both did in 2021, along with future housing PCE inflation due to a methodology-driven lag. This was purely a demand-driven phenomenon, but also one that would sort itself out so long as the labor market normalized to more stable rates of job growth and wage growth.

As job growth normalized, market-rent inflation stabilized too and the outlook for housing PCE inflation has been improving as a result.

With labor turnover and search costs normalizing as we moved further away from the pandemic, wage growth has also cooled off, all while unemployment has stayed low, and employment rates have still climbed higher.

All of these explanations were expected to support demand to higher levels of activity before leveling off as the impulses faded away. The spike to growth was real, and the cooldown was too. The absolute scale and the timeline of these dynamics were broadly underestimated, both on the way up and on the way down.

The Fed hiked 525 basis points, ergo it must have mattered, right? Sure, but how? And how much?

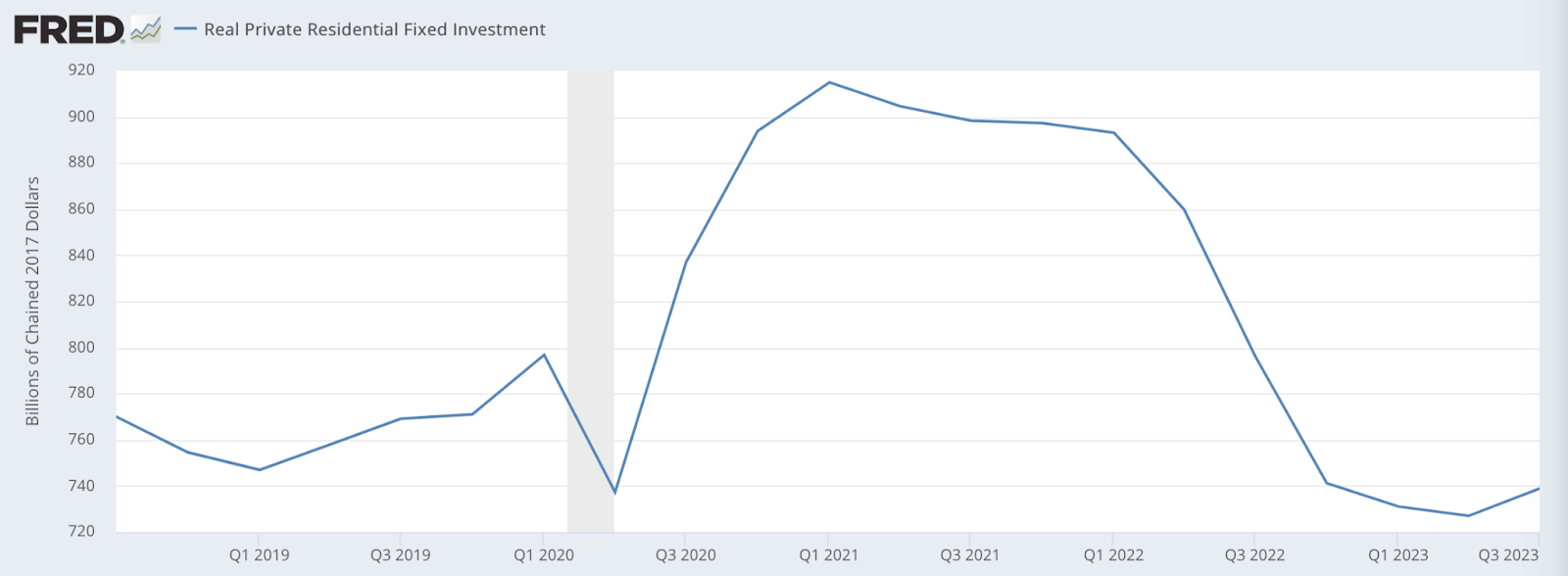

It’s easy to see the Fed’s effects on asset prices broadly. It’s very easy to see their affirmative effects on the housing market. Mortgage rates spiked. Mortgage purchase applications fell. Home sales fell. Housing starts fell. Building permits fell. All align nicely with the timing of mortgage rate increases. There is no need to hide behind a “counterfactual shield” to say the Fed mattered here. We could say similar things about aspects of bank lending channels; the regional banking mini-crisis likely required higher interest rates as a catalyst and choked off some credit supply in the process.

The trouble is that these well-identified mechanisms have everything to do with the fixed investment side of GDP and inflation, and not a lot to do with consumption and the PCE deflator (the Fed’s inflation gauge of choice). Home sales commissions and residential construction are both segments of fixed investment. The identifiable real effects of Fed tightening hit investment (future supply). There is a “housing” segment of services PCE inflation, but this is entirely based on rent data, including Owners’ Equivalent Rent. The Fed might affect rental housing demand through a cooler/weaker labor market, but neither the timing of market rent stabilization nor causal intuition align with the idea that rent was directly sensitive to interest rates.

To tell a story about the Fed helping lower inflation through the demand-side, the Fed would have to be lowering consumer spending on some level. Does lower homeownership lower spending on durable goods for homes, like furniture and furnishings? Sure, and that was a slice of the overall inflation picture, but a small slice. Do lower asset prices lower financial services PCE inflation? Yes, but there too, the effects are not large or persistent in the context of how PCE inflation evolved. For all the talk about the importance of wealth effects (which surely exist at the margin), these too are hard to see in the data. Remember, real consumption accelerated (and nominal consumer spending still grew at a very solid clip).

Could we say that the Fed’s effects on fixed investment had downside implications on consumption through the labor market? Not obviously. Speculatively, a cooler housing market might free up resources to devote to the supply of consumption but the causal linkage still seems speculative. In contrast to the 2004-06 hiking cycle, construction employment continued to make additional gains despite the Fed’s depressing effect on the housing market. The investment-sensitive segments of the labor market seem to be buffered by some of the major legislative acts of the past 3 years (IIJA, IRA, CHIPS).

Did the Fed’s hikes hasten the broader labor market deceleration and normalization we have witnessed? Could job growth and wage growth have decelerated more slowly in the absence of Fed hikes? Absolutely. It seems very likely at the margin and against a simple counterfactual. But if we are trying to determine how much, we lack the kind of smoking gun identifiable evidence here (in contrast with the housing activity data). Given just how much employment has *outperformed* expectations–even those expectations forecasted and formed prior to the Fed’s hikes—it is not clear how much “demand reduction” is left to be explained by Fed tightening.

In the New Keynesian macroeconomic model, the dominant explanations for inflation are with respect to (labor market) slack / the output gap, or else inflation expectations. A period in which inflation falls but (1) unemployment stays low, (2) employment rates climb higher and, most damningly, (3) real GDP growth accelerates to an above-trend pace…that flagrantly violates a demand-driven Phillips Curve view of how Fed tightening enables disinflation. It isn’t even consistent with a nonlinear Phillips Curve, which usually can be abused as a “get out of jail free” card. We didn’t even see a modest GDP growth slowdown; we saw outright acceleration to an above-trend pace.

The data is getting very uncomfortable for those who cling hard to the expectations-augmented Phillips Curve as a touchstone for understanding inflation. If slack isn’t doing the trick, then must it be through inflation expectations? This seems dubious on its own. What exactly is the underlying economic mechanism that causes agents to change their inflation expectations in response to Fed policy, if not the credible prospect of a weaker economy and more potential slack? If there is no credible outcome from higher interest rates that economic agents are front-running, are expectations supposed to change based on a Jedi mind trick? Not that the rational expectations revolution has served macroeconomics entirely well, but this kind of ad hoc departure can quickly veer into the absurd. Calling the Fed's actions a "credibility bonus" that helped reduce inflation—independent of any credible intermediate outcome–is simply not credible.

Empirically, there are additional problems with expectations-based explanations. Fed hikes are supposed to robustly affect inflation expectations, which then affect inflation itself. Household survey measures of expectations showed the most movement in both directions, but they largely lagged inflation itself. Financial market measures of expectations, which involve the highest financial incentive for accuracy, were remarkably and excessively stable. The ultimate mapping here needs to show both (1) the Fed influenced expectations, and (2) those influenced expectations affected price-setting behavior.

Our biggest worry through this episode was that the Fed’s hikes might spark a nonlinear downside outcome. But that scenario was always best understood as a risk, rather than in purely deterministic terms.

Interest rates can be raised dramatically and yet the impact on consumption can be largely invisible at first; see the 2004-2006 hiking cycle, in which financial conditions barely tightened at first. Interest rates can also be raised only marginally, as they were in December 2015, only to incite very visible financial market panic. And sometimes things break merely because interest rates are left too high for too long, even in the absence of hikes, as proved to be the case in 2007, 2000, and 1990. All of these episodes are reasons to treat every interest rate decision with caution but not be overly judgmental about the precise level of interest rates at any given point in time. The elasticity between Fed policy and the real economy can change on a dime.

This should be a bigger wake-up call that if the goal is to reliably manage inflation outcomes with minimal collateral damage, we need to develop better policy tools and frameworks, ones that can better assess supply dynamics and manage demand more equitably.

The rush to say “I was right, you were wrong” on all sides looks increasingly crass, especially when it’s just based on 6-7 months of Core PCE inflation data running at a 2% annualized rate. These inflation outcomes are impressive when compared to the grim consensus at the start of 2023, but let’s all take a deep breath here. We don’t even have 12 months of solid data to point to yet. That 6-month snapshot of inflation fails to capture what has proven to be the hottest quarter of inflation over the past few years: Q1. We would not be shocked if there were a few more bumps in the disinflationary road, whether due to residual seasonality in Q1 or simply due to new shocks emerging. Hold your horses, and chill out. It’s not as if anyone has nailed all of their predictions over the last 4 years; you can be admirably early or late to predict something, but even that is still a version of “wrong.”

The labor market is standing strong even as inflation has fallen faster than most forecasters expected. Entering 2023, the Fed largely thought that appropriate monetary policy to achieve 2% inflation would involve a recessionary rise in joblessness. If joblessness had risen as the Fed had projected to happen under "appropriate monetary policy," the Fed likely would not have tried to stabilize the economy until it was too late. Thankfully, joblessness did not rise like that, despite a mini-banking crisis emerging in March. We are all fortunate that Fed policy did not have its full set of intended/projected effects.

Our biggest critique of the Fed in 2023 was about the willingness to concede recessionary labor market outcomes for the sake of lower inflation under appropriate monetary policy. The Fed, to their credit, pivoted away from this dark view, starting in June 2023 and more formally in September 2023. If the Fed was fortunate through much of 2023, 2024 is now their opportunity to capitalize on their good fortune.