Post-December FOMC: The Fed Gets Pessimistic About Inflation, but Shouldn't Downplay Labor Market Risk

If there’s one takeaway from this meeting, it’s that the Committee wants to position themselves much more cautiously on the inflation outlook, but the Fed is just a couple of bad labor market prints from having to put more cuts back on the table.

On Wednesday, the FOMC decided to cut the target federal funds rate by 25bps, but delivered a hawkish rate path projection for 2025. In the Summary of Economic Projections (SEP), the median projection is solidly for two cuts in 2025, down from four in the September SEP.

This projection is more hawkish than the baseline in our preview to this meeting and appears to be driven by a substantially more pessimistic view of inflation in 2025. Part of this is a reaction to some recent warm inflation prints (September and October) but the press conference made clear that at least part of the Committee is taking into account the possibility of inflationary tariff policies under a second Trump administration.

Inflation Pessimism

If there’s one takeaway from this meeting, it’s that the Committee wants to position themselves much more cautiously on the inflation outlook. As Powell said during the press conference, “the single biggest factor is inflation has once again underperformed relative to expectations.” Core PCE inflation looks to be ending the year around 2.8 - 2.9%, upwards from the Committee’s projection of 2.6% in September.

In the SEP, Committee members substantially revised their projections of inflation upwards for 2025. At the last meeting, the bulk of Committee members saw inflation coming down to 2.1 - 2.2% next year; now, they see core PCE inflation only falling to 2.5 - 2.6%. Is this reaction to a few bad inflation prints warranted, or is it data point dependence? In response to a question about the Fed’s confidence in the trajectory of inflation, Powell went into the breakdown of where elevated inflation is coming from:

Housing inflation is elevated, but they’re confident in the downward trajectory even if they’re uncertain about the timeline;

Goods inflation is where it “should” be;

Market-based non-housing services are “in good shape”

Non-market-based non-housing services are elevated but don’t reveal much about the tightness in the economy.

In short, the primary reasons for inflation pessimism are housing inflation, which is known to be a lagging measure by construction and (b) non-“market-based” measures like measured financial services, which are essentially a proxy for equity prices. This is a pretty thin basis for such a large swing in the Fed’s inflation outlook, and two other things are going on.

First, besides the recent inflation prints, the Committee is now apparently taking into account forecasts of new tariff policies under a second Trump administration. Despite Powell explicitly disavowing this in the previous meeting, he made clear that this was a part of the analysis, saying “some people did take a very preliminary step and start to incorporate highly conditional estimates of economic effects of policies into their forecast at this meeting.”

Second, over the past few months, the Fed has received a lot of criticism for their 50bp cut in September and continuing to cut at this meeting despite inflation overshooting their September projections and unemployment backing off somewhat from its July reading. Under these conditions, penciling in fewer cuts and a pessimistic inflation projection looks like the path to least regret. It’s unlikely that too many people will be upset if inflation performs better and the Fed ends up cutting three or four times next year, but if they continue to underproject on inflation they will continue to look like they’re getting caught flat-footed by inflation.

On the bright side, the path to further rate cuts next year is somewhat more likely than the Committee has signaled. As Neil Dutta noted, the more pessimistic inflation projections mean that the bar for additional cuts, relative to expectations, has been lowered.

Labor Market Risks

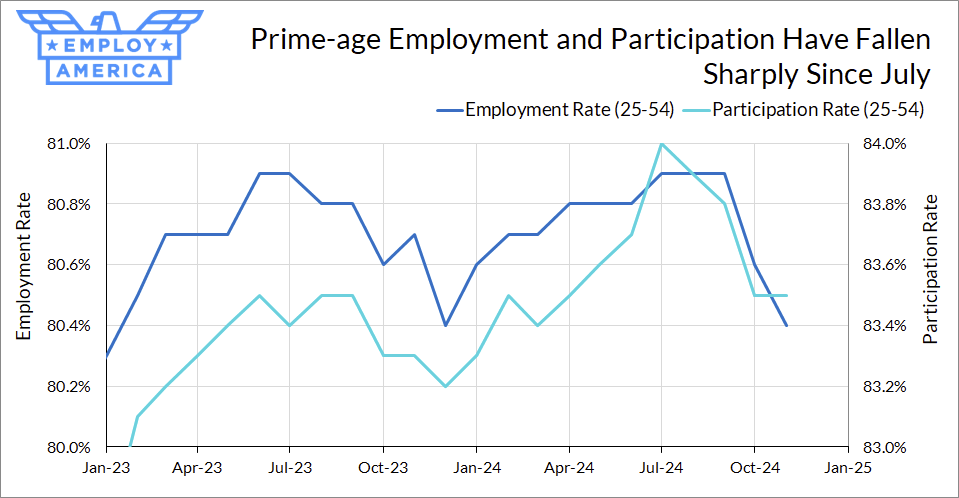

Another underrated reason why the Fed may end up cutting more next year is labor market risk. The Fed is still communicating the commitment they made in September to maintaining the labor market, but they may be underestimating the risk that the labor market continues to worsen over the next few months. While the unemployment rate has avoided the further deterioration that the Fed feared in September, the current level of 4.2% is a mere rounding error from the 4.3% the Fed is projecting over the next three years. In fact, the unrounded unemployment rate is less than a basis point lower than its peak in July.

For months now, FOMC members have been talking about the possibility that we may be looking at a period of higher sustained productivity and GDP growth. One reason that FOMC members across the spectrum have proffered for why r-star might be higher has been the spate of high growth and productivity. Kashkari, Musalem, and Daly all see higher GDP and productivity growth as a reason why the long-run rate may be higher. As strong growth has continued to persist over the past year, the median projection for the long-run neutral rate has steadily risen from 2.5% to 3.0%.

But if one were to look at the SEP, this belief is nowhere to be found in the GDP projections. For the last two years, the median projection for GDP growth in 2025 has stayed between 1.8 and 2.1% and the long-run growth projection has remained at 1.8%. In fact, the December 2024 distribution of the projections for long-run growth are almost identical to the projections a year ago.

There is an inconsistency here. They keep saying they’re not ready to buy into the high productivity narrative yet, attributing much of it to temporary supply recovery—but will happily accept it as an explanation for a higher neutral rate. Stubbornly keeping their GDP expectations low sets them up to get “surprised” by high growth, justifying keeping rates higher for longer.

With this much uncertainty, optionality is needed

Going into 2025, the Fed faces uncertainty on a number of fronts. Inflation is higher than anticipated and they face policy uncertainty from a new and unpredictable incoming Trump administration. Their decision to take two cuts out from 2025 demonstrates that they’re attuned to the inflation risk, but they may not be fully appreciating the downside risk to the labor market. With unemployment nearly at the July level that saw additional rate cuts, the Fed is just a couple of bad labor market prints from having to put more cuts back on the table.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.