Core-Cast is our nowcasting model to track the Fed's preferred inflation gauges before and through their release date. The heatmaps below give a comprehensive view of how inflation components and themes are performing relative to what transpires when inflation is running at 2%.

This is a truncated version of the preview initially made available to our exclusive distribution on Thursday. Please reach out to us if you would like to access the full preview when it is first made available.

Summary

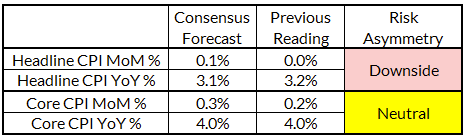

Headline CPI is poised to grow slower (0.05%) than consensus (0.1%), while there are balanced risks around consensus expectations for core CPI.

Our forecast is in line with consensus for Core CPI (0.31%) with a relatively high wedge to Core PCE (10-15 basis points).

A Core PCE reading lower than 20 basis points would keep a potential March "normalization cut" in play in our view, but to fully materialize, it would require further progress in December and January as well. We define a "normalization cut" as a cut motivated primarily by a decline in inflation and not by visible labor market, financial market, or general growth deterioration.

Forecast Details

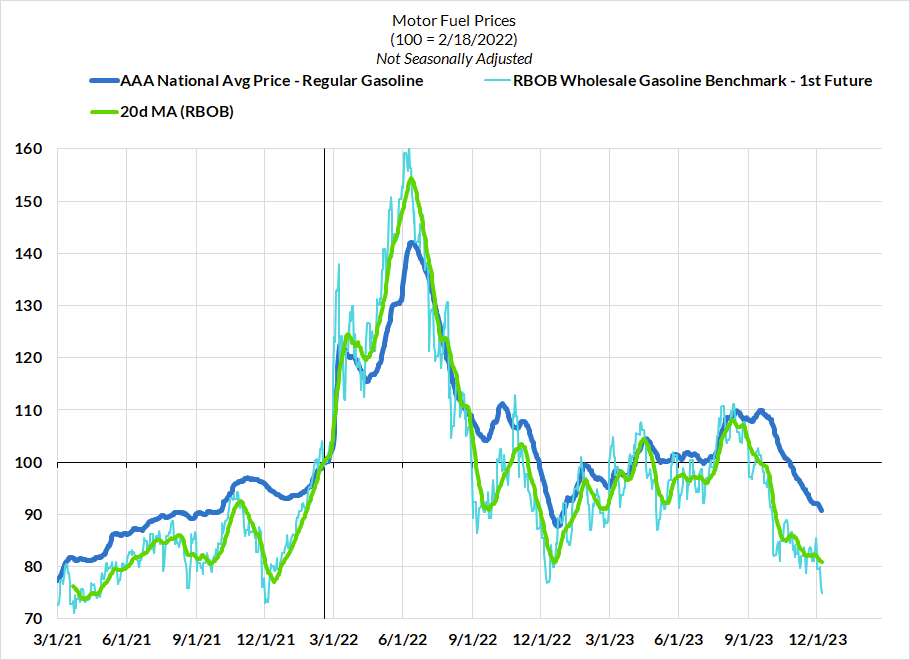

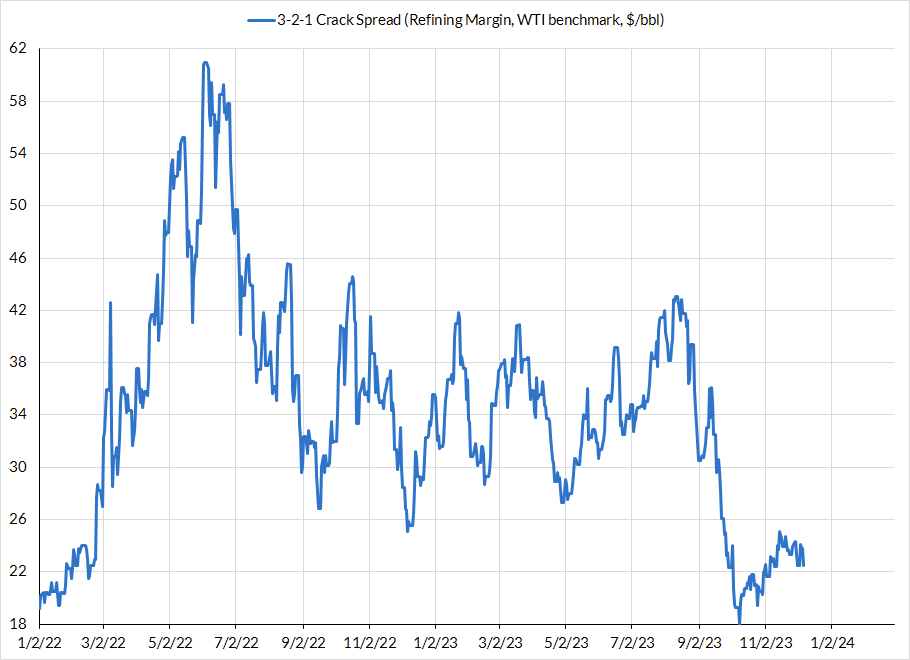

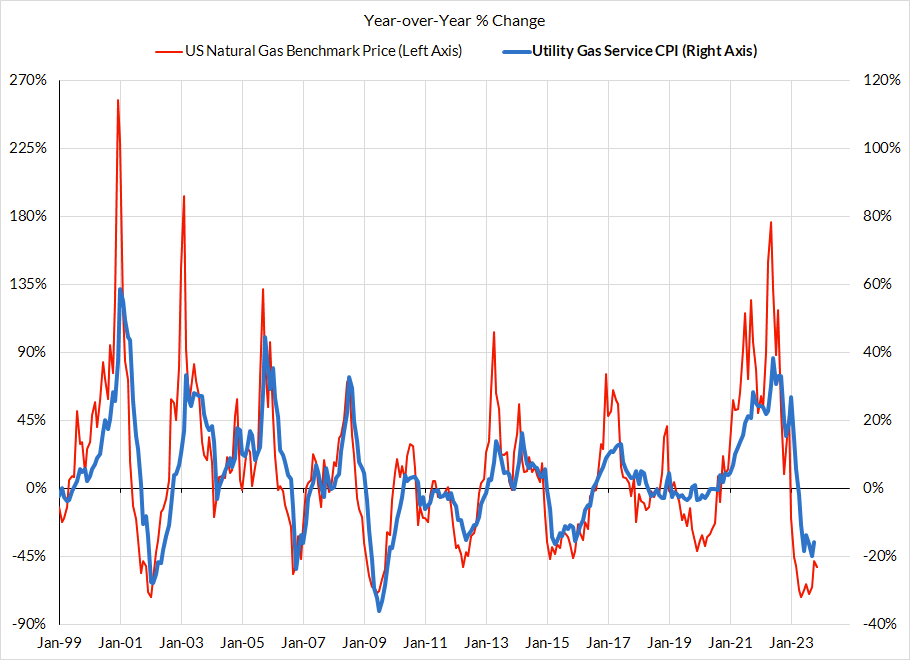

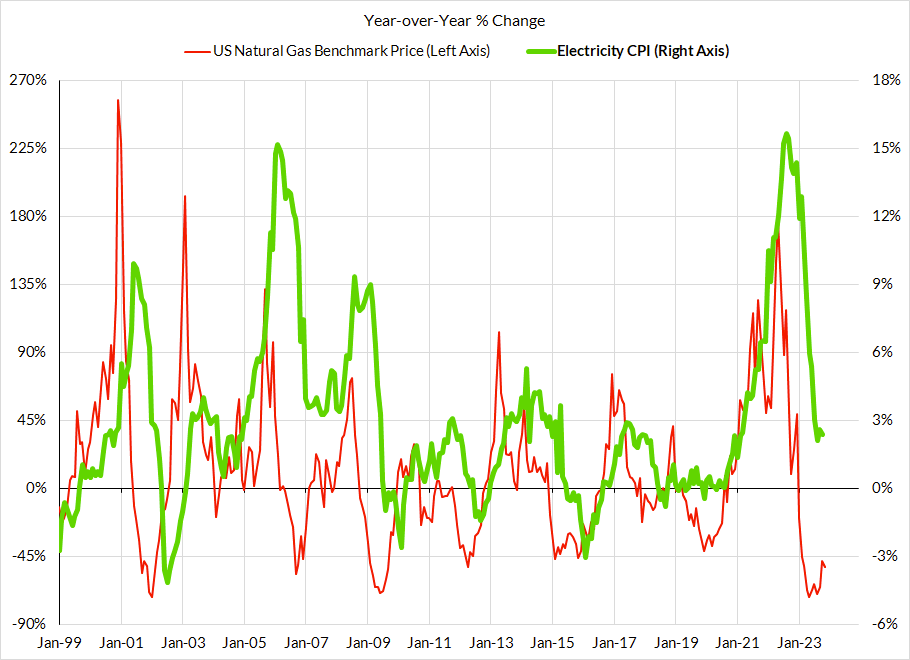

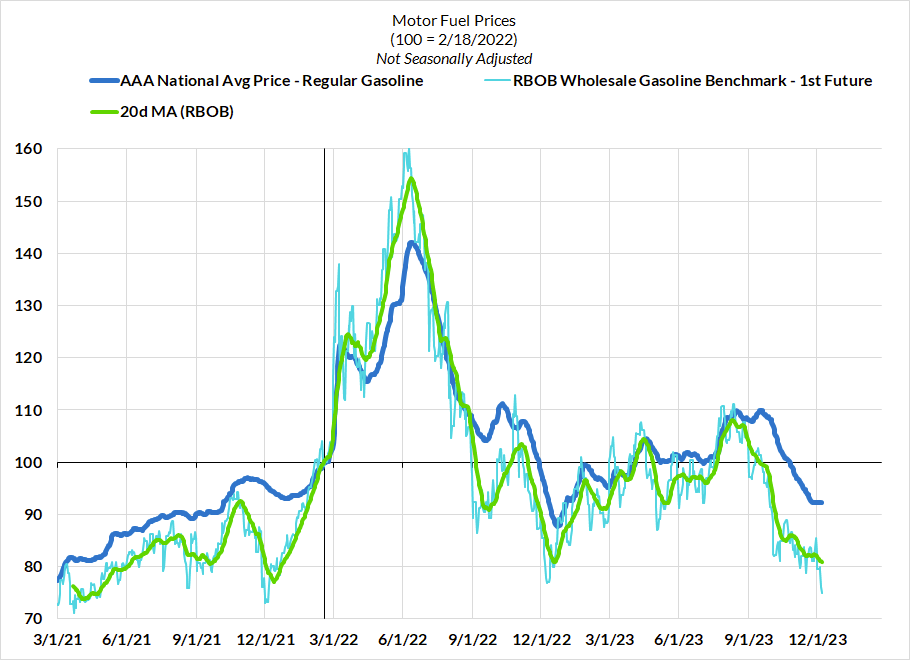

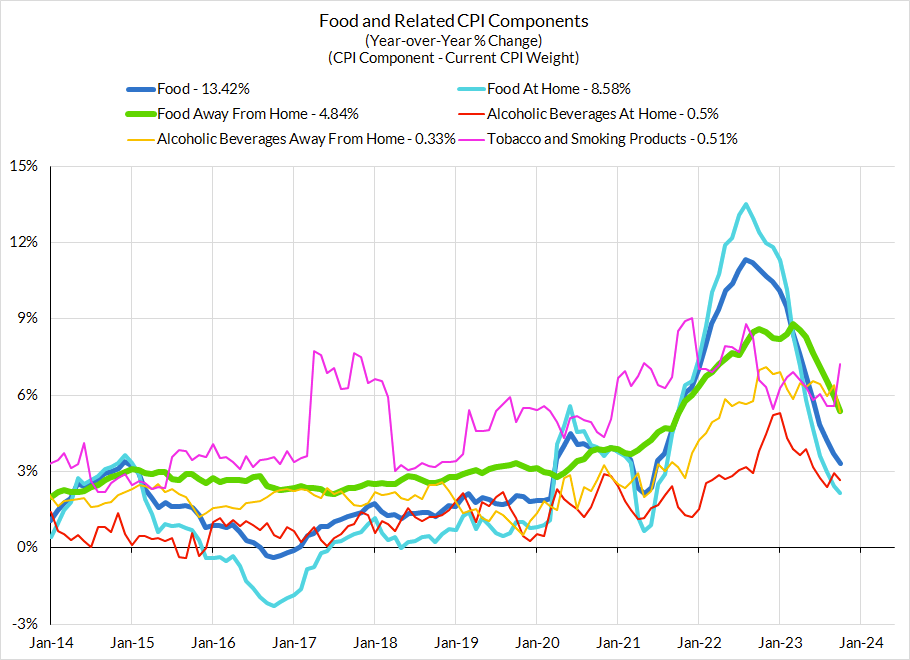

The primary reason for headline inflation downside (0.05% vs 0.1% consensus) is the late decline in gasoline prices at the end of November. To a lesser extent, there are good reasons to believe in favorable commodity price passthrough to energy services (from natural gas) and to food categories (from diesel primarily).

Our core CPI forecast is for 0.31% increase, in line with consensus. The risks appear balanced, with downside likely to be driven by broad goods deflation (household furnishings, apparel, recreation goods, information technology goods) and upside to be driven by volatile service prices (lodging, airfares, healthcare services). The easiest path to CPI upside surprise involves shallower goods deflation in November. The easiest path to CPI downside surprises involve faster services disinflation in goods-adjacent categories (e.g. value-sensitive motor vehicle services).

Core PCE can materially underperform Core CPI if healthcare, airfares and vehicle insurance PPI materially underperform their CPI analogues. Our base case is for core PCE to come in around 19 basis points. A Core PCE reading lower than 20 basis points would keep a potential March "normalization cut" in play in our view, but to fully materialize, it would require further progress in December and January as well. We define a "normalization cut" as a cut motivated primarily by a decline in inflation and not by visible labor market, financial market, or general growth deterioration.

Key Dynamics Within Baseline View

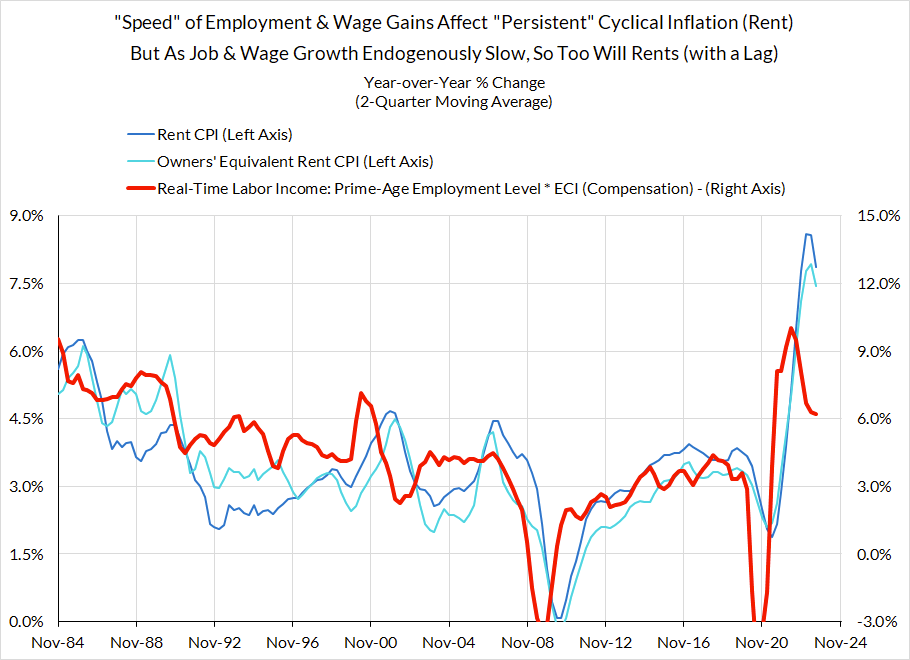

The most important driver of core inflation will be the trajectory of rent and owners' equivalent rent (OER). Market rents have continued to slow and arguably deflate on some measures. These outcomes should, with some diminished sensitivity and a longer lag, feed into CPI and PCE outcomes. As it currently stands, the last 3-6 months of core PCE overshoot vs the Fed's 2% target would disappear if rent and OER CPI were replaced with real-time market-rent measures. Over the course of 2024, core PCE should slow purely because of slowing rent and OER inflation

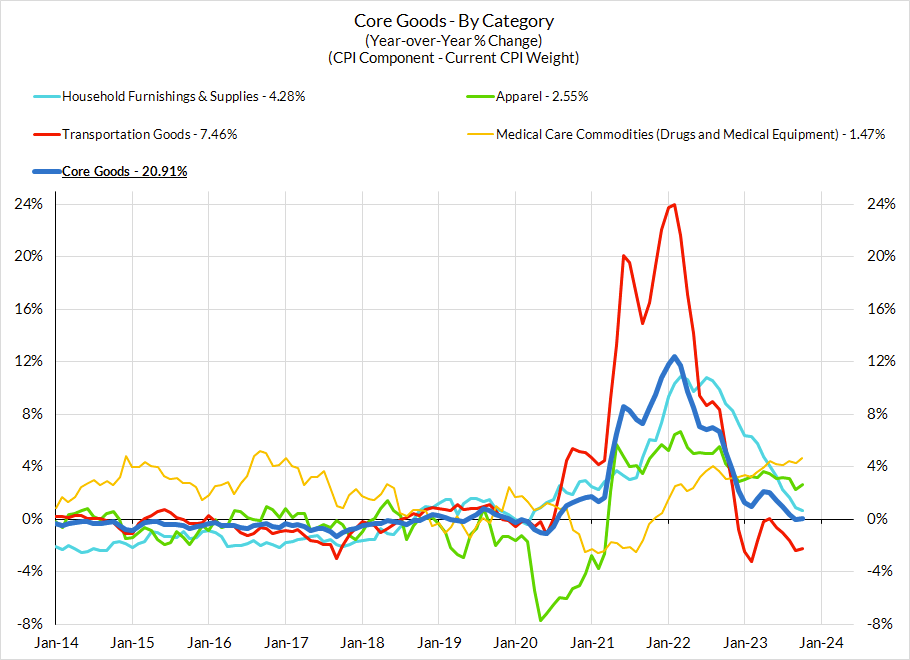

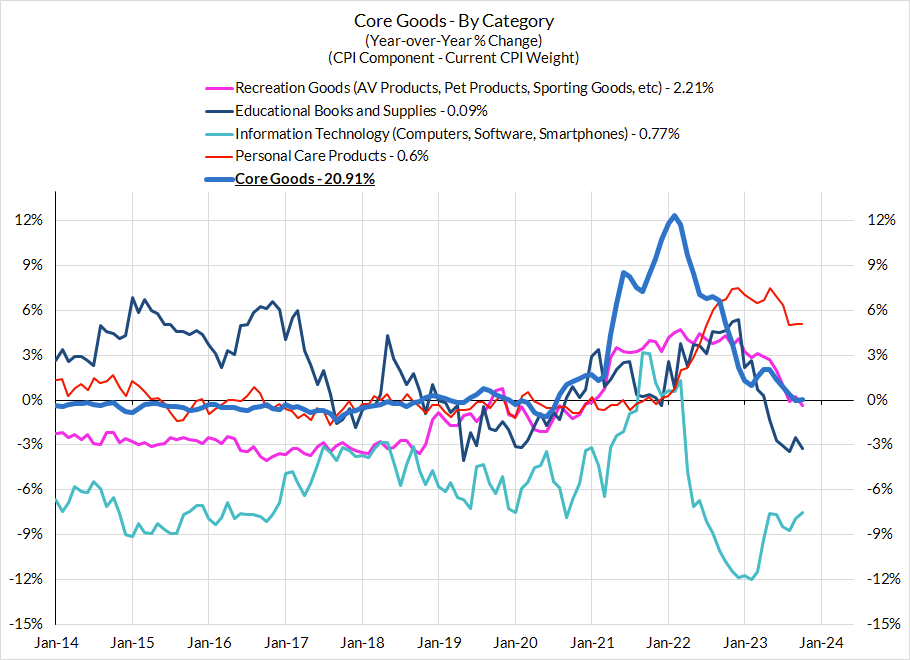

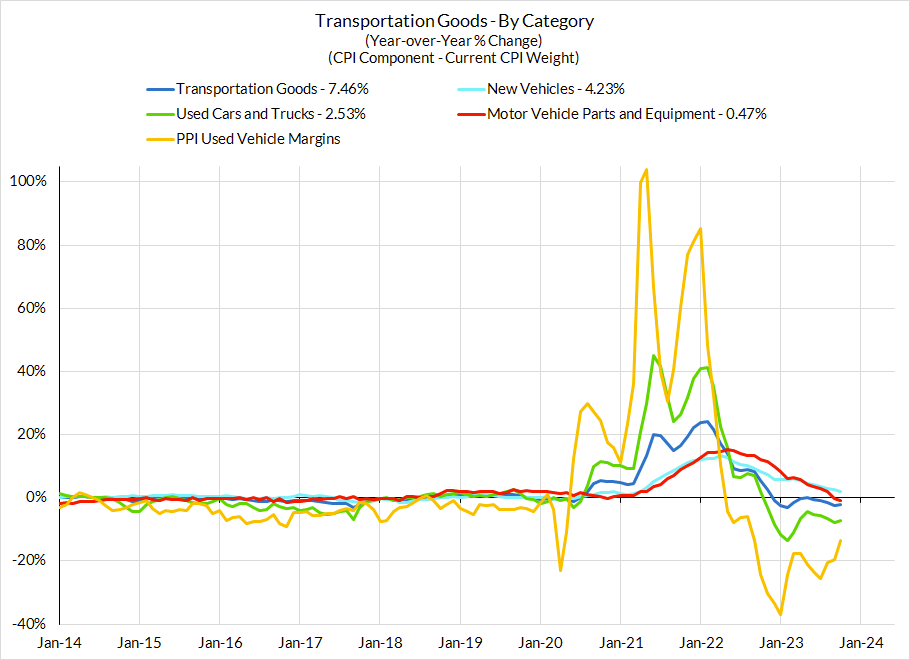

Core goods deflation should continue, but expect it to be a shallow but persistent contributor to the disinflationary process. Price levels for a number of key core goods categories are still elevated and thus have room for sustained underperformance in a manner that supports achievement of the Fed's 2% target. The pace of this deceleration might be dismissed as transitory, but it likely will not be symmetric to the surge we saw in 2021 and 2022. Instead, we see good evidence and reason to believe that price transmission from key cost and supply chain shocks will be asymmetric. While prices rocketed higher as these shocks first hit, they will likely deflate at a slower pace (rockets vs feathers). For November, we are expecting less vehicles deflation than what has transpired in recent months, but there will be a deflationary resurgence in the coming few months given what the weekly wholesale auction data currently signals.

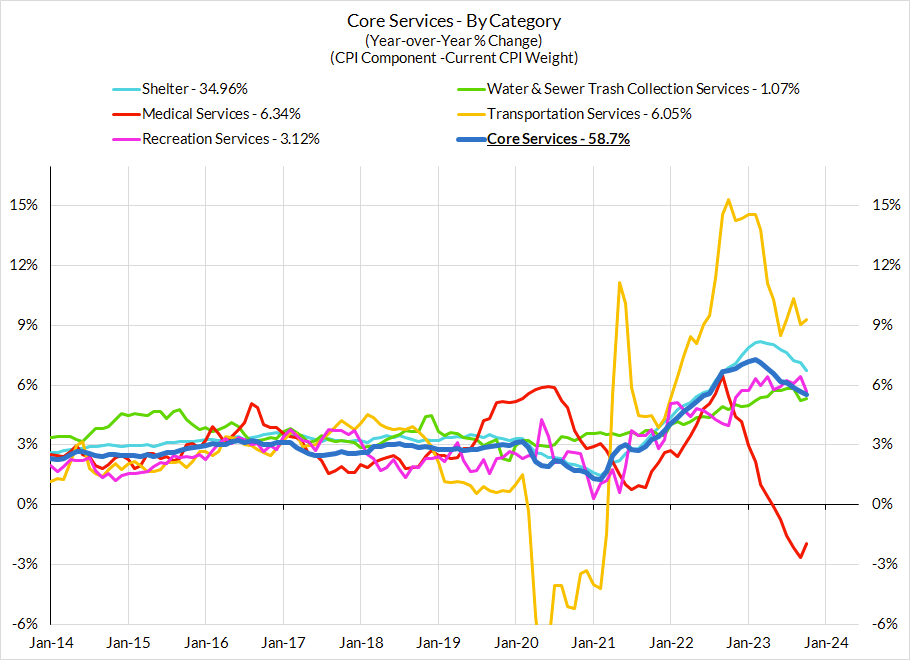

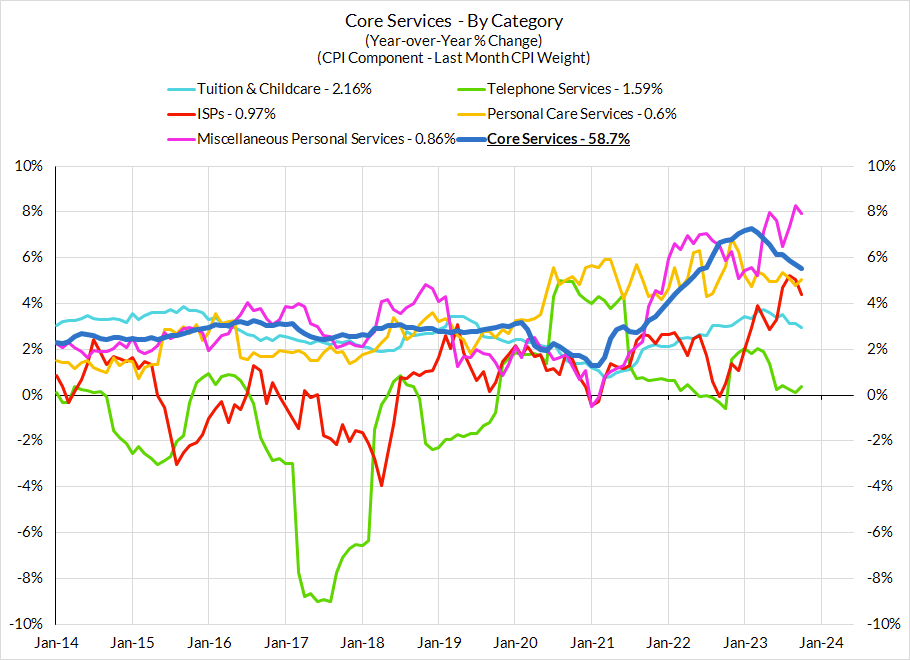

Core services disinflation will ultimately materialize but the road will be bumpy and noisy between CPI and PCE: While we have calculated a "supercore" CPI forecast for this preview, it's worth flagging that this supercore is only partially aligned with "supercore" PCE. Some volatile prices are likely to flare higher in November thanks to residual seasonality issues (lodging) and general volatility (airfare CPI). Other service prices are ultimately poised to disinflate in a manner that lags related goods prices (e.g. value-sensitive motor vehicle services, food services).

Commodity price passthrough on the downside: Over the next six months, we expect to see more encouraging signs from lower commodity prices. Two key mechanisms: diesel->food at home -> food services and jet fuel -> airfares. Energy prices likely matter to a number of core nondurable goods too.

CPI Charts

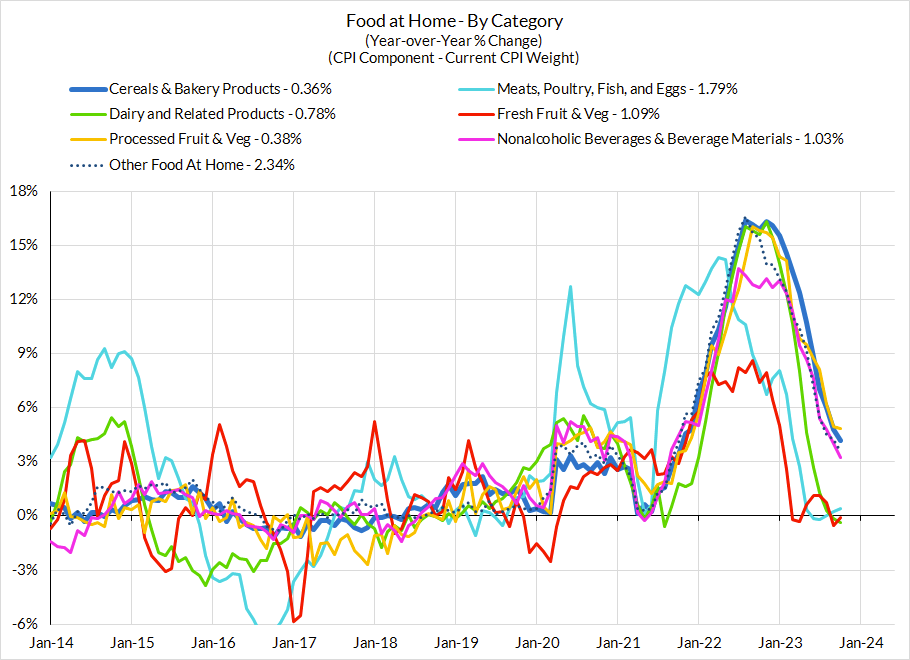

Non-Core CPI Components

Core Goods CPI Components

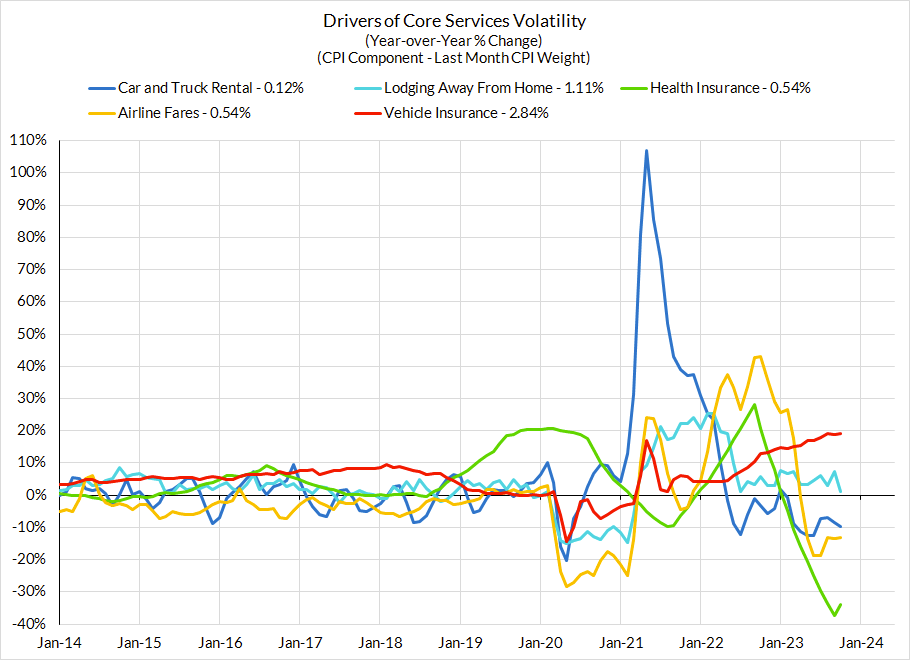

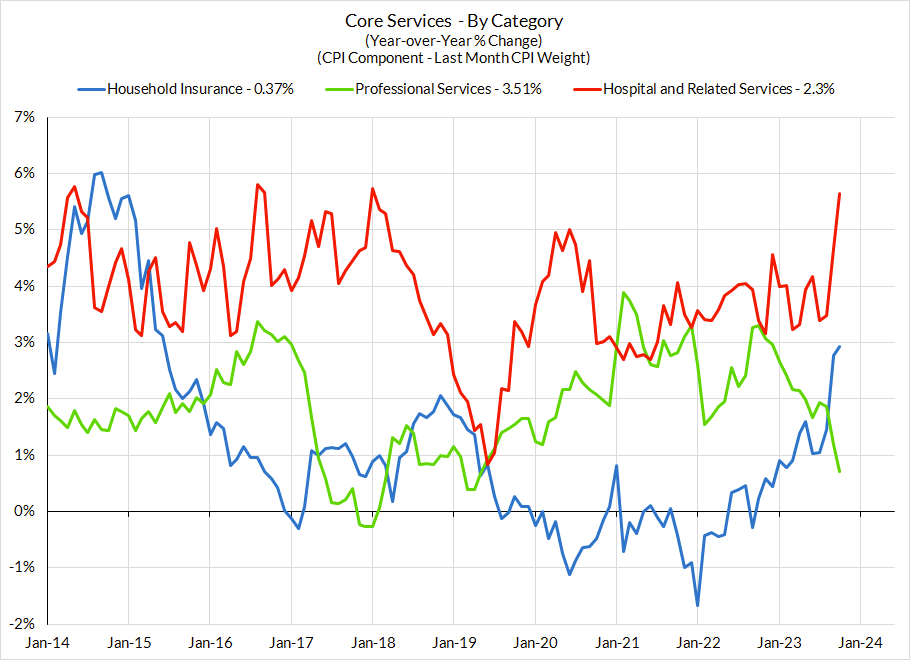

Core Services CPI Components (Not All Feed Into Core PCE)

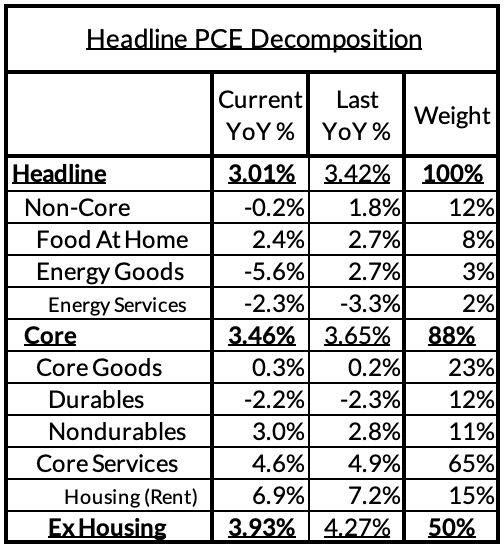

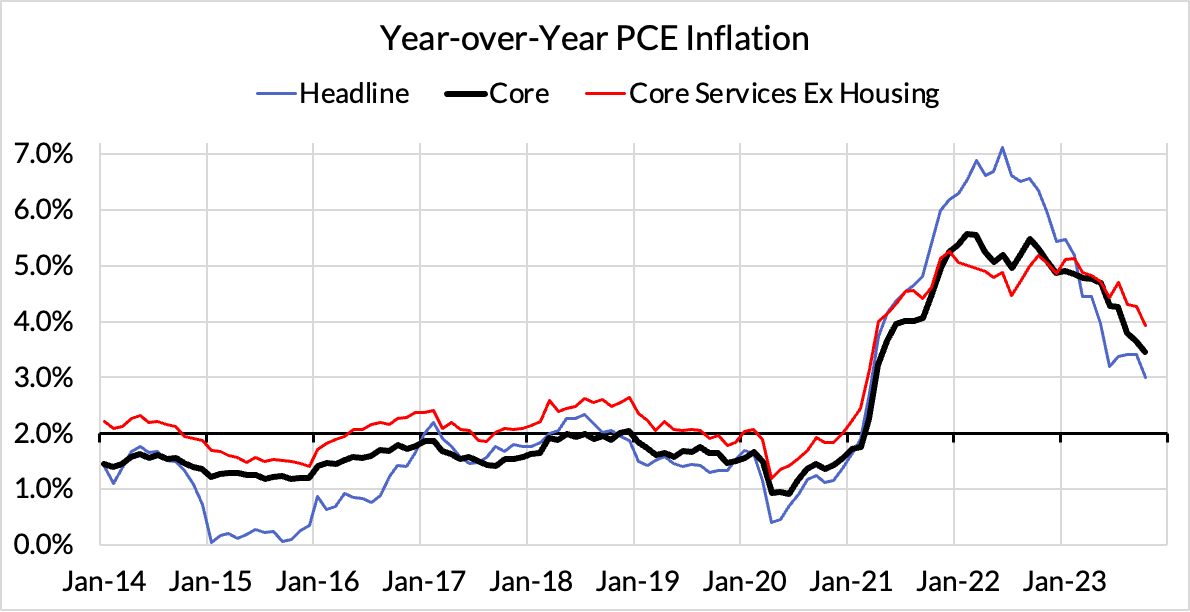

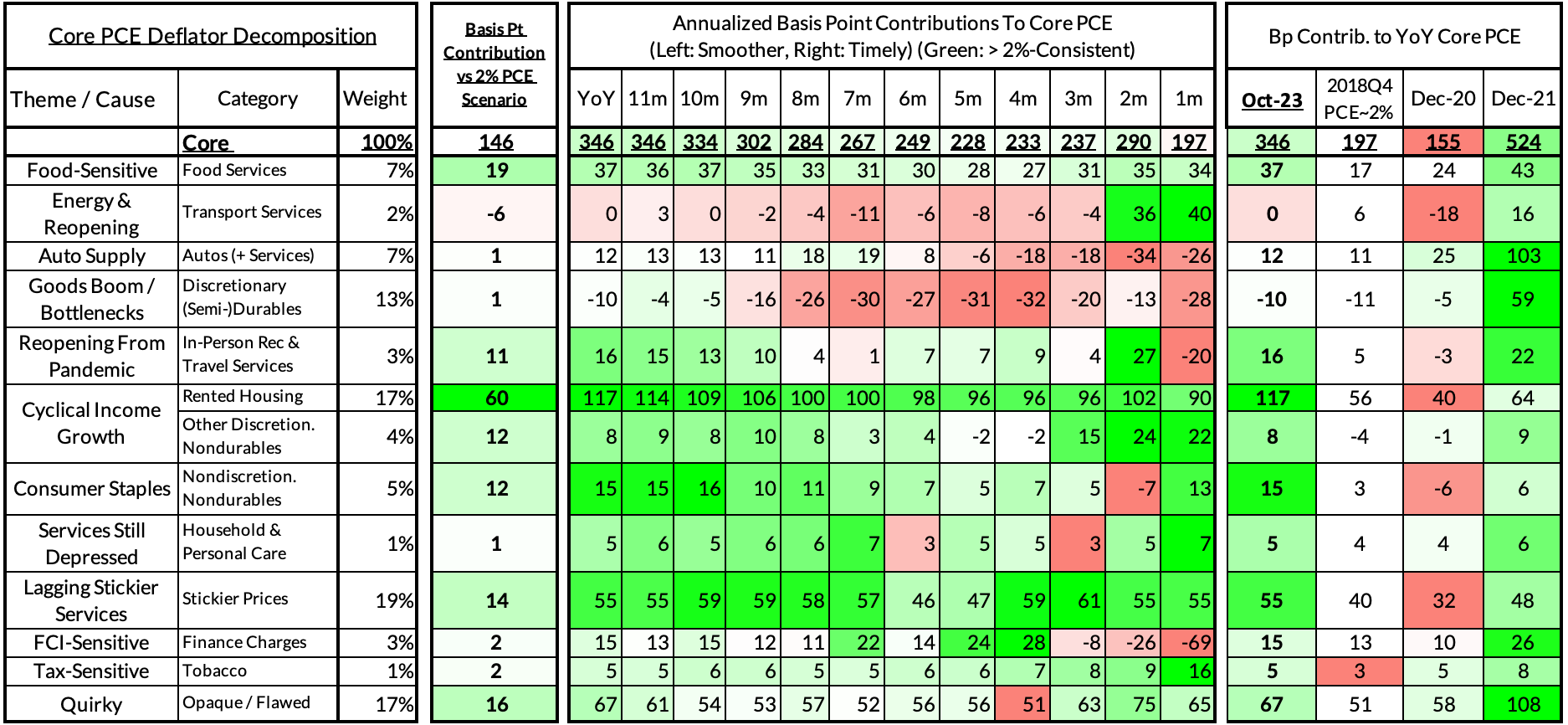

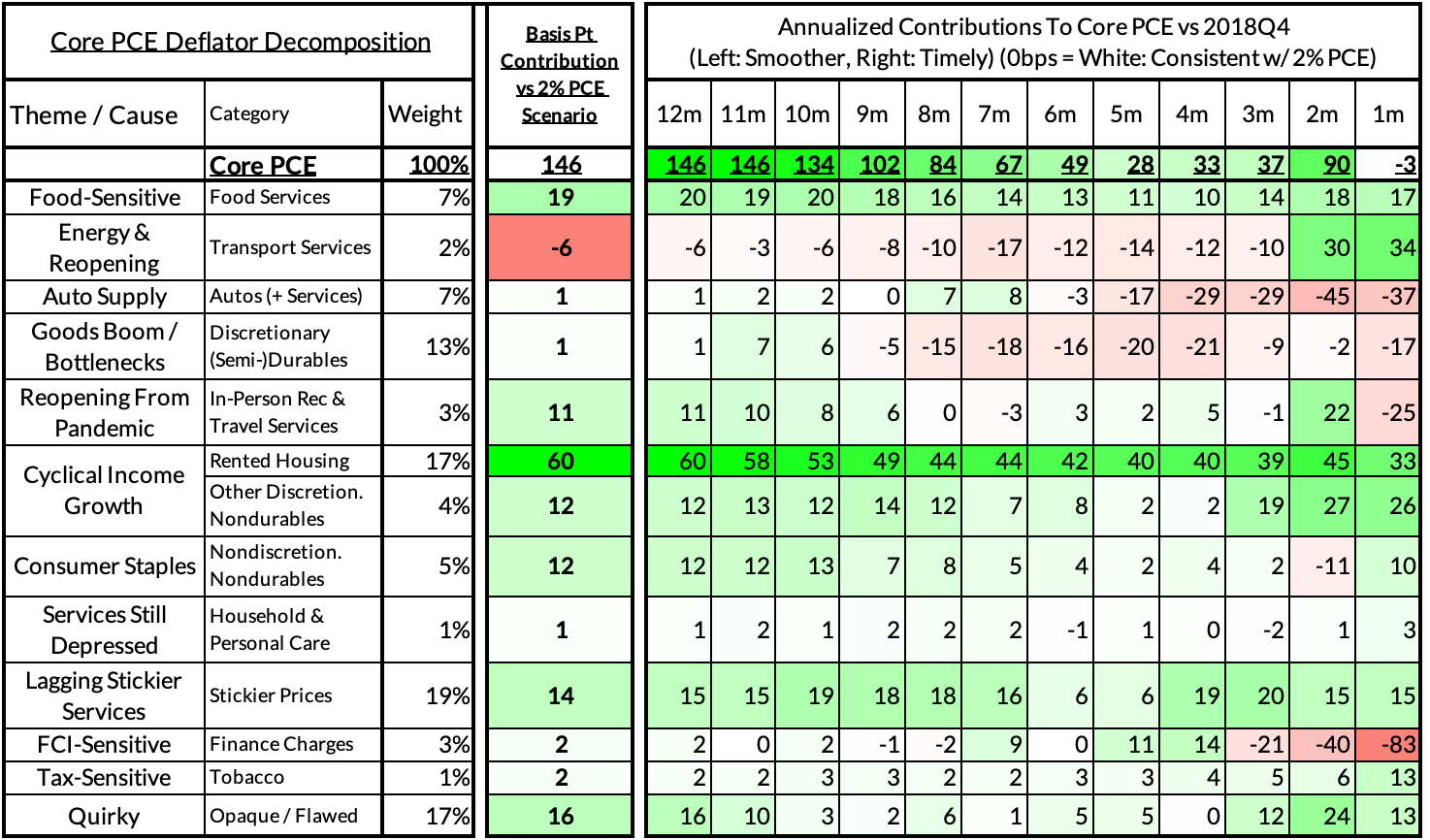

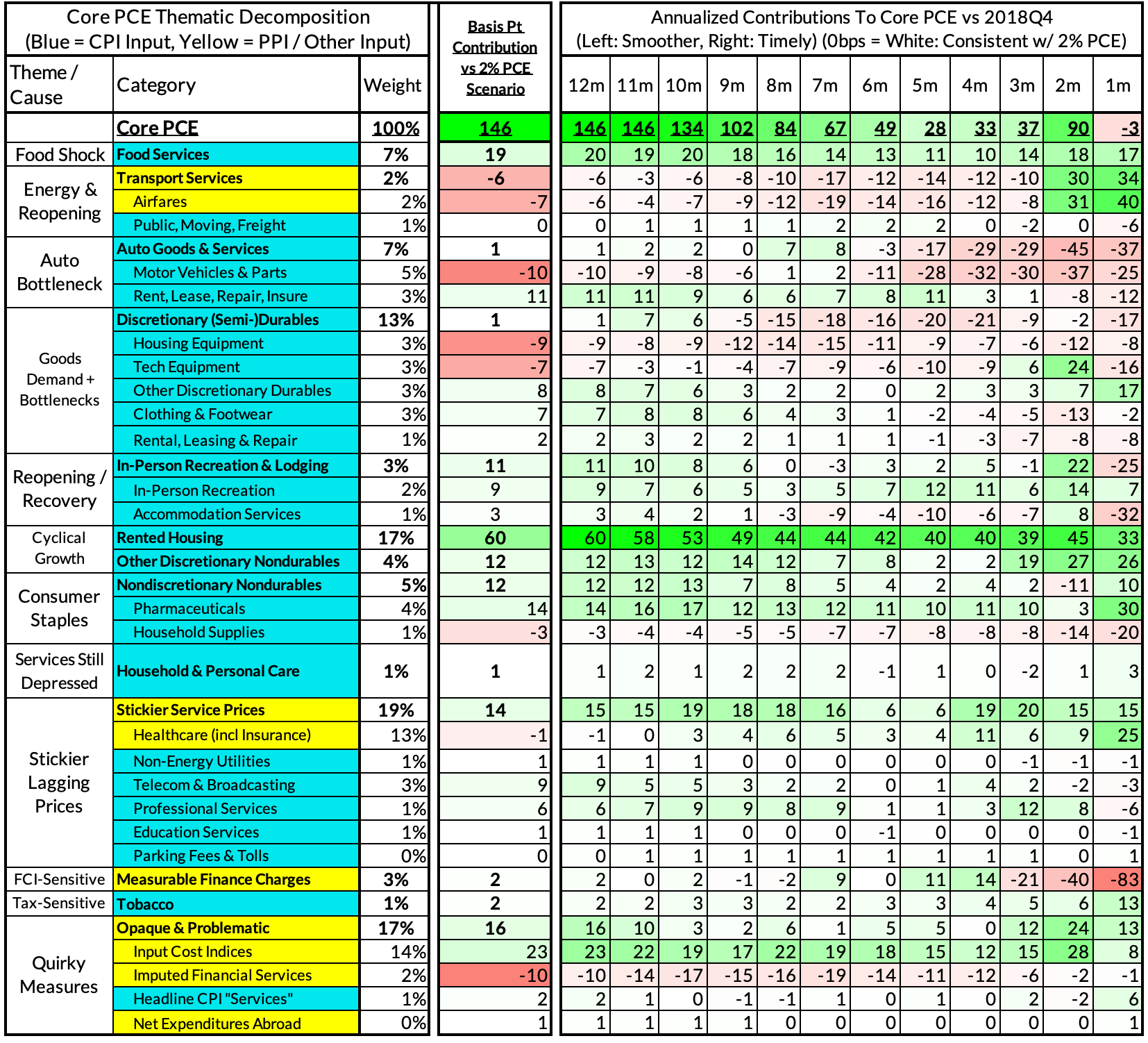

Right now Core PCE (PCE less food products and energy) is running at a 3.46% year-over-year pace as of October, 146 basis points above the Fed's 2% inflation target for PCE. That overshoot is disproportionately driven by catch-up rent CPI inflation in response to the surge in household formation (a byproduct of rapidly recovering job growth), which caused market rents to surge in 2021. Rent is contributing 60 basis points to the 146 basis point core PCE overshoot.

There are other contributors to the overshoot:

Some more supply-driven (automobile bottlenecks are likely to explain only 1 basis point now, while food inputs likely added 19 basis points to the overshoot)

Some more demand-driven (in-person recreation and travel services likely added 11 basis points to the overshoot)

So with demand- and supply-side drivers (consumer staples and discretionary goods likely added 25 basis points).

Some oddball segments have offsetting effects (measured financial service charges now likely added 2 basis points, while contributions from input cost indices and imputed financial services likely added 13 basis points to Core PCE vs 2%-consistent outcomes).

The final two heat maps below gives you a sense of the overshoot on shorter annualized run-rates. October monthly annualized core PCE yielded a 3 basis point undershoot vs 2% target inflation (1.97% annualized).

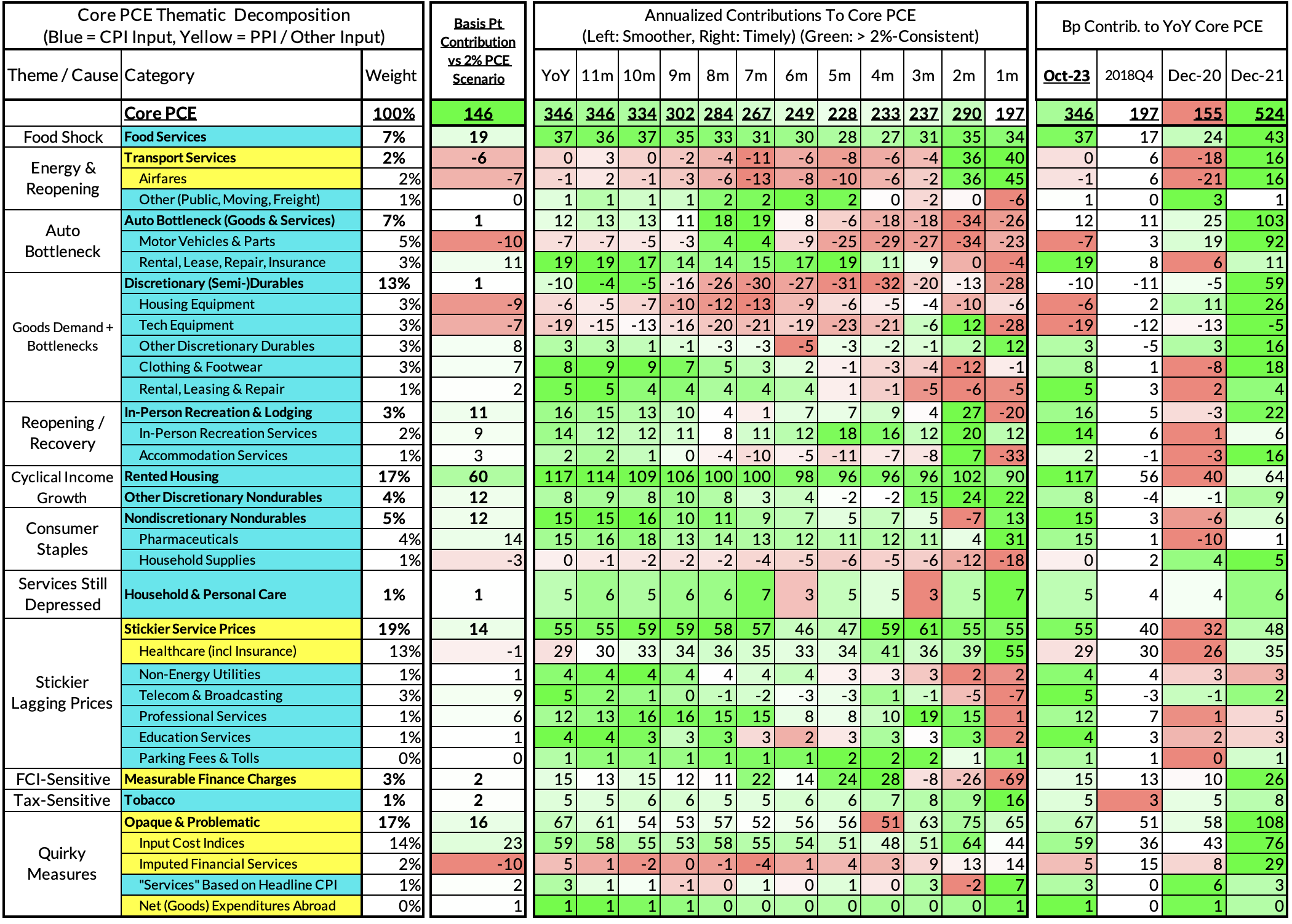

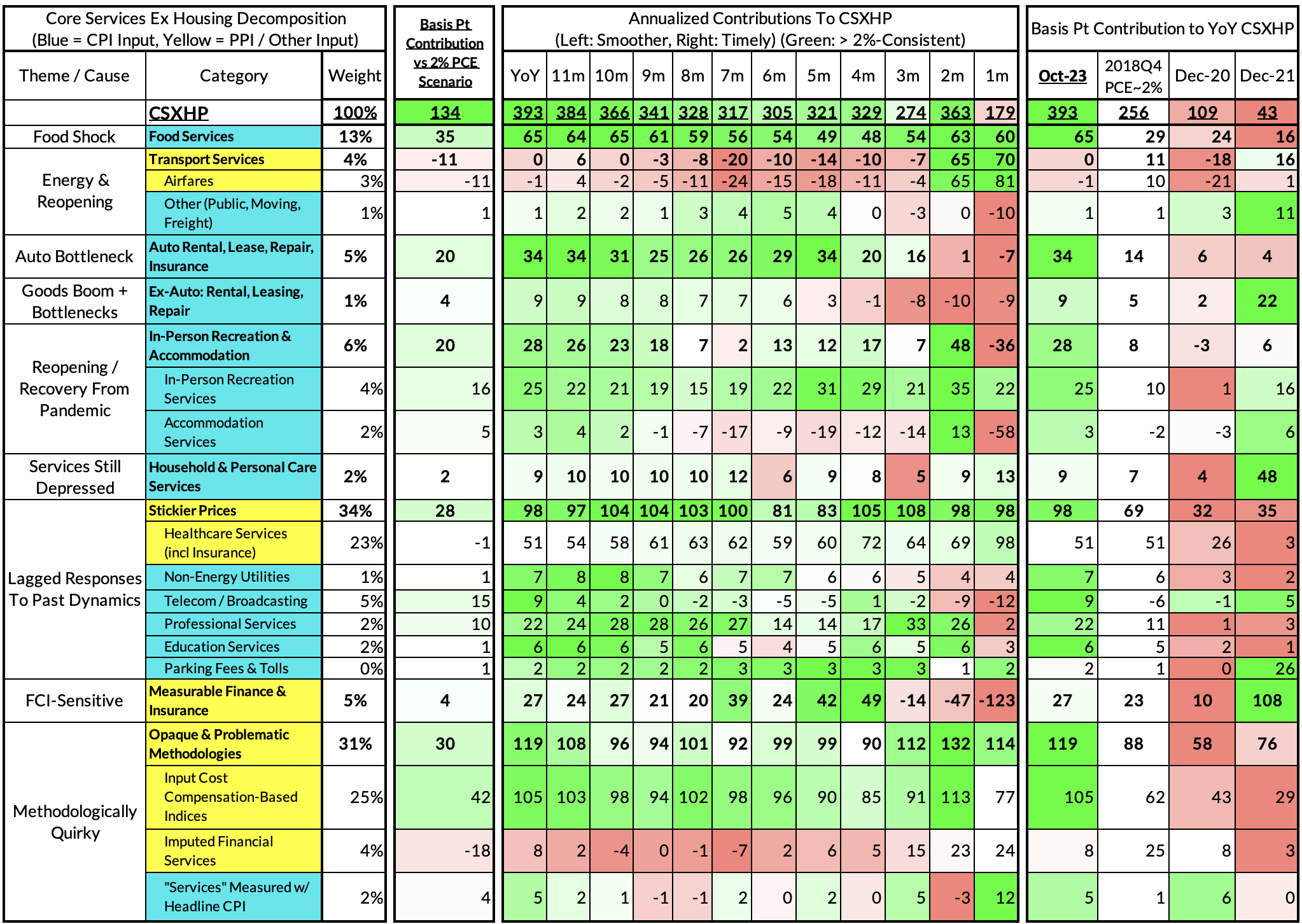

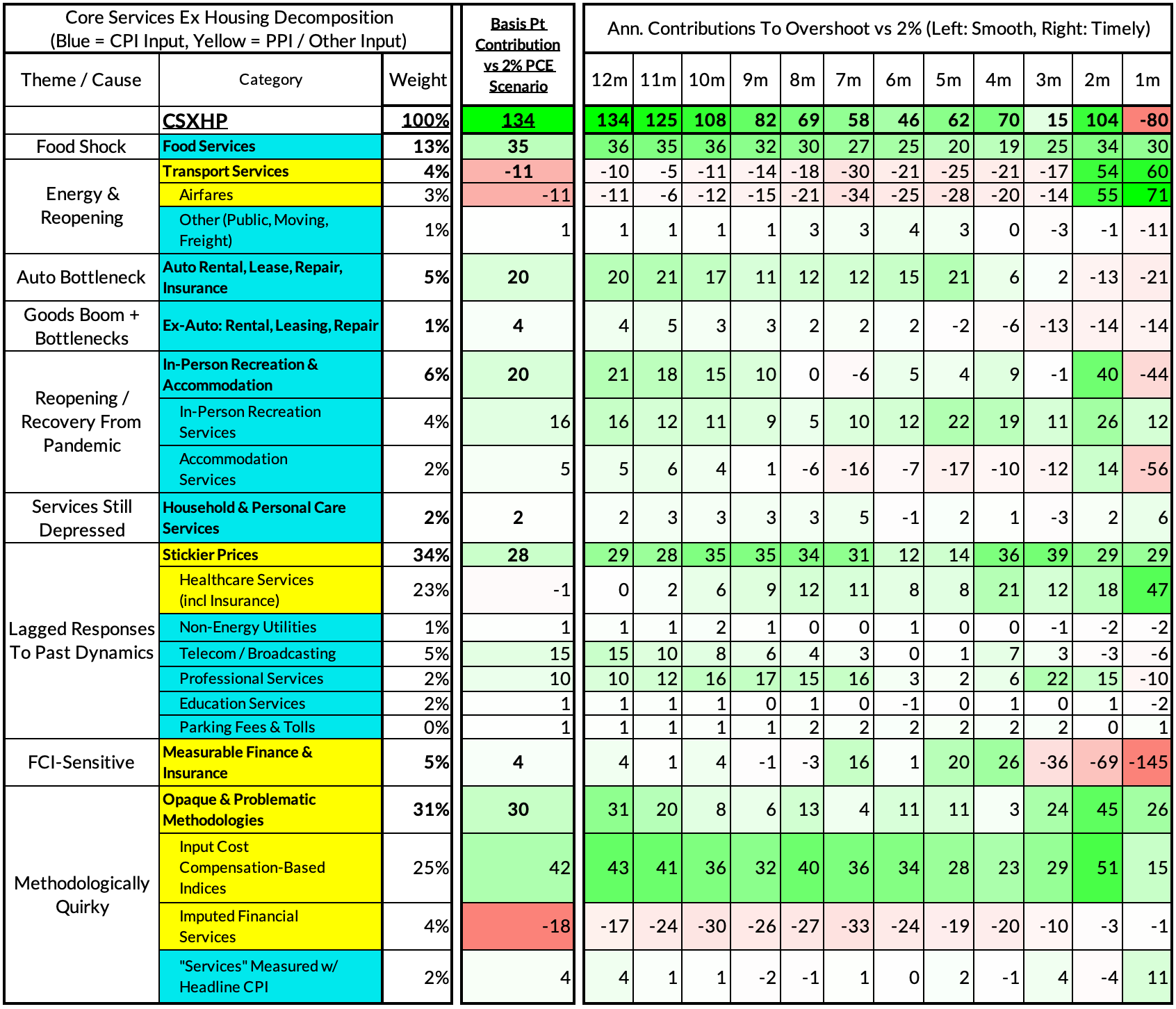

For the Detail-Oriented: Core Services Ex Housing PCE Heatmaps

The October growth rate in "Core Services Ex Housing" ('supercore') PCE ran at 3.93% year-over-year, a 179 basis point overshoot versus the 2.56% run rate that coincided with ~2% headline and core PCE.

September monthly supercore ran at a 1.79% annualized rate, an 80 basis point undershoot of what would be consistent with 2% headline and core PCE.