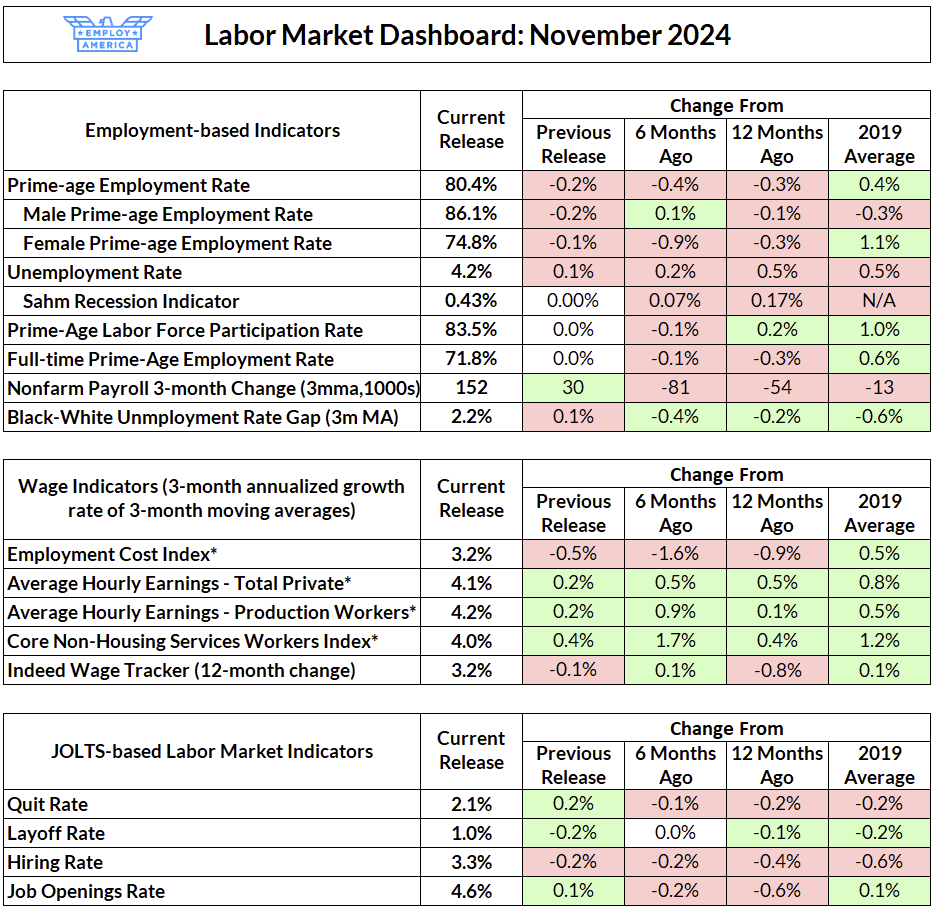

The labor market added 227,000 net jobs in November, with slight positive revisions to previous months. The unemployment rate rose by 0.1pp to 4.2%; prime-age employment fell by 0.2pp, and prime-age labor force participation was flat. Average hourly earnings growth was up slightly, and is growing at around 4.0% in recent months. JOLTS measures improved slightly, with little sign of layoffs, but hiring rates are still sluggish.

The past two months have been difficult to read due to the effect of, and the bounceback from, hurricanes and strikes. If one takes the average over October and November’s payroll growth, employment has grown by 131,500 jobs a month. That is comfortably at least the breakeven level of employment growth if demographics were “normal”, but it’s perhaps too low in a laboar market with higher immigration than previously expected. Employment rates, while strong, have been essentially stagnant for nearly two years as the unemployment rate has risen from its historical lows. Wage growth is historically elevated but rationalized by productivity growth.

The labor market is treading water at this point. It’s not drowning, but it’s unclear how long it can remain in this state. Austan Goolsbee is fond of saying that if we could keep the labor market as it is currently, that would be a great outcome—but the question is, how much do rates need to normalize to keep it that way?

How Long Can We Stay Here?

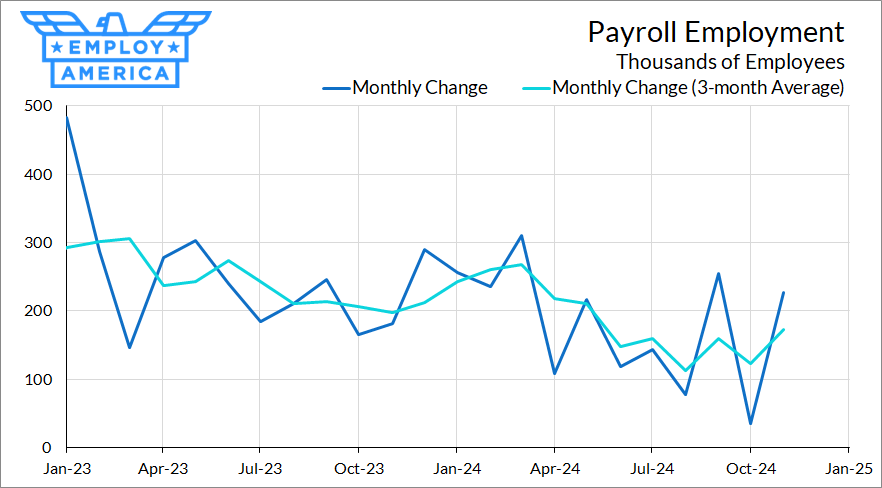

Monthly payroll growth numbers are notoriously difficult to draw conclusions from due to noise, one-off variations, and revisions. The last two months were no exception, with October depressed due to strikes and weather and November’s count rebounding from said effects (to wit, transportation equipment employment grew by 32,000 in November). However, taking a longer view with some smoothing shows short-run job growth falling from 200,000-250,000 to 100,000-150,000 over the course of this year.

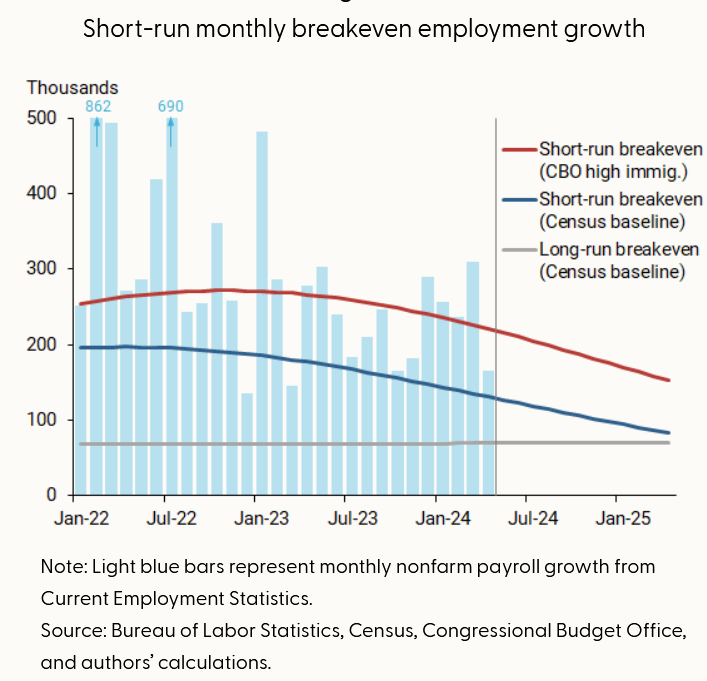

During normal times, payroll growth north of 100,000 would be considered more than acceptable. However, things haven’t been normal due to the high levels of immigration seen over the past few years. As Powell once said: "More people working, bigger economy." An article from Petrosky-Nadeau and Stewart at the San Francisco Fed earlier this year estimates monthly breakeven employment growth rates (required payroll growth to maintain a 3.8% unemployment rate) based on different assumptions about how immigration has evolved.

Under a higher immigration scenario, short-run breakeven employment growth is currently somewhere around 200,000 (well above current levels of payroll growth) and may not return to “normal” levels until 2027. We may need to judge payroll growth by a higher standard for a few years.

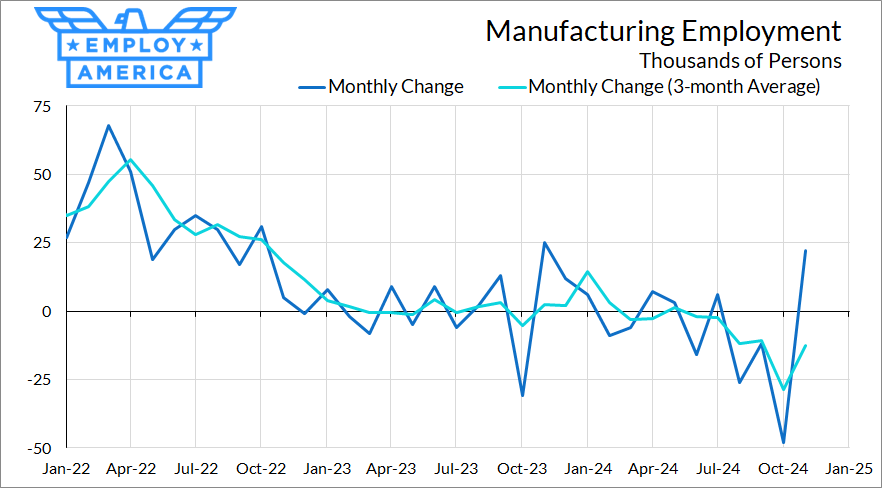

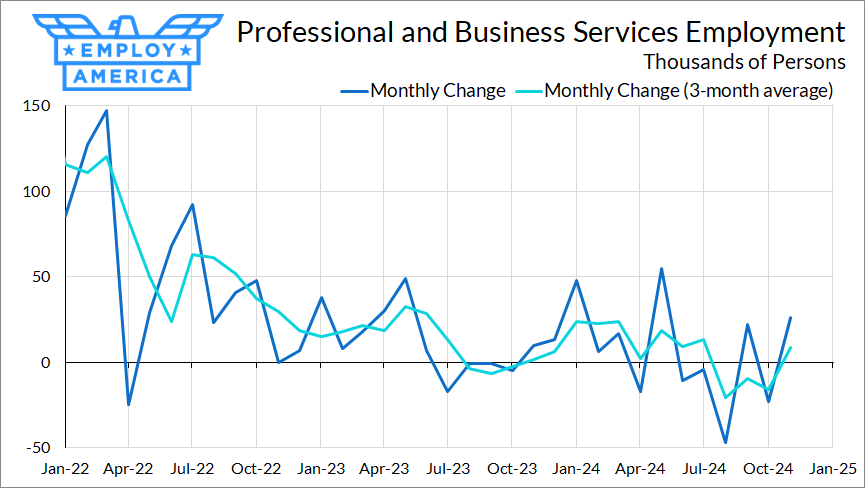

Looking at a sectoral level, it does appear that more cyclical, rate-sensitive sectors are also the weak points of the labor market. In recent months, sectors like education, healthcare, and government have contributed a disproportionate amount to employment growth. Meanwhile, manufacturing employment is falling and professional and business services employment continues to stagnate.

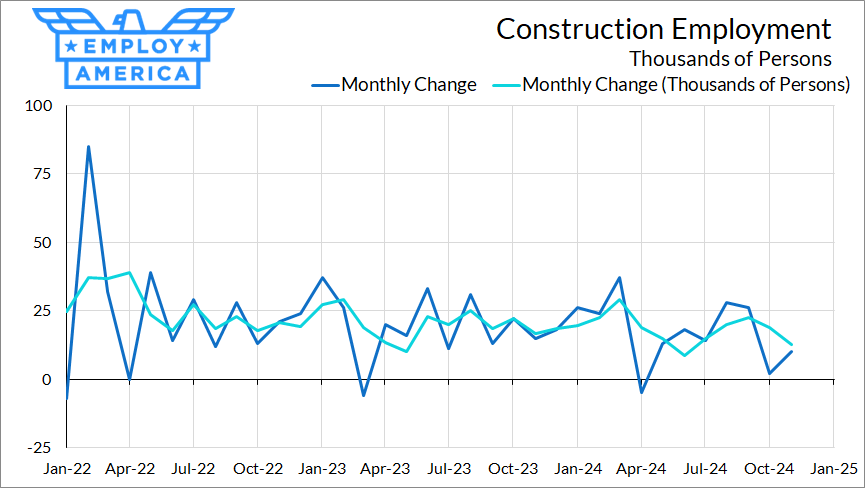

Bucking this trend is construction employment, which continues to post solid gains. Construction employment is up 2.6% year-on-year, versus 1.4% for all sectors.

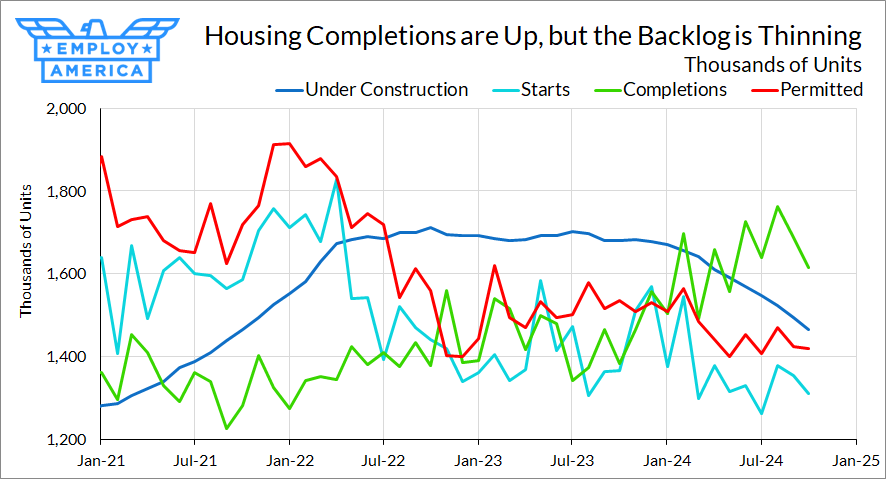

Right now, construction seems solid—but how long can this continue? Right now, completions are at their highest levels in nearly 20 years, but permits and starts are depressed, and housing units under construction have been falling throughout the year. Unless something picks up in new construction, it seems unlikely that construction employment can maintain its strength.

Household Survey Weakness

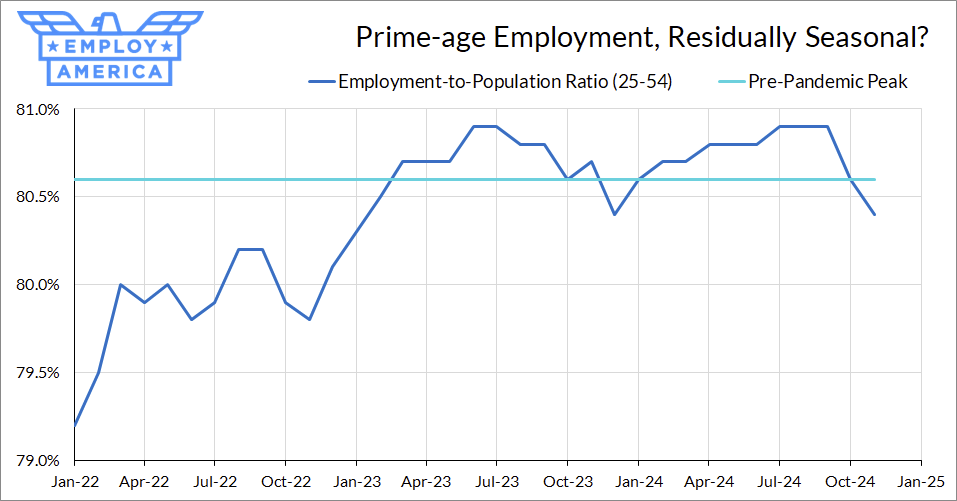

The household survey showed some signs of concern, with the prime-age employment rate falling to 80.4% in November, down 0.5pp from its historical high just two months ago. That’s a concerning drop, but it could be that we’re just seeing the same hump-shaped pattern in employment we saw in 2023 and there’s some residual seasonality that hasn’t been adjusted away.

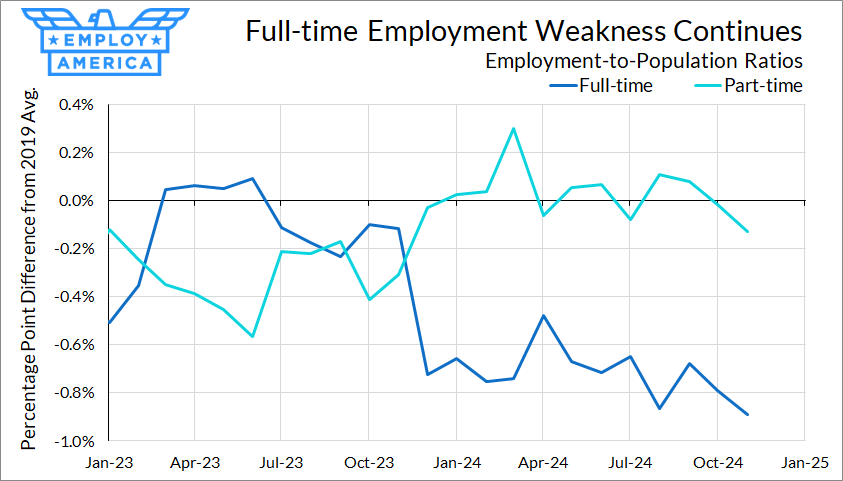

The rest of the household survey looks relatively uninteresting. Full-time employment continued to fall, and is at its lowest level in the past two years.

Normalizing versus Weakening?

In a recent essay, Atlanta Fed President Raphael Bostic is asking the right question: “The salient question for me today is whether the labor market is cooling more dramatically than I had imagined when I developed my outlook for the economy.” What makes this question hard to answer is the fact that we are still left with the ripple effects of COVID disruptions, even as we move past 2024 and into 2025. The top question in mind for me with the labor market is: how much labor market softening is simply the result of COVID disruptions gradually dissipating versus more traditional cyclical weaknesses that merit stronger intervention from policymakers? The presence of the former makes it much more difficult to discern the extent of the latter.

Take, for example, the sectoral differences in employment growth happening right now. On one hand, the stronger growth of less-cyclical sectors like education and government can be rationalized by the catch-up of those sectors after the stronger growth in sectors like professional and business services earlier on in the pandemic. On the other hand, it could mask genuine weakness in rate-sensitive sectors from restrictive monetary policy.

Bostic’s essay cites another example of the muddy waters of renormalization and weakness: the net employment growth from establishment entry and exit, which was very high in the early 2020s due to strong business formation, appears to have dissipated. This removes an upwards impulse to employment growing forward.

So far the Fedspeak has remained open to a December cut. We think the labor market data from November was weak and murky enough to bolster the case, both positively and normatively, for doing so.