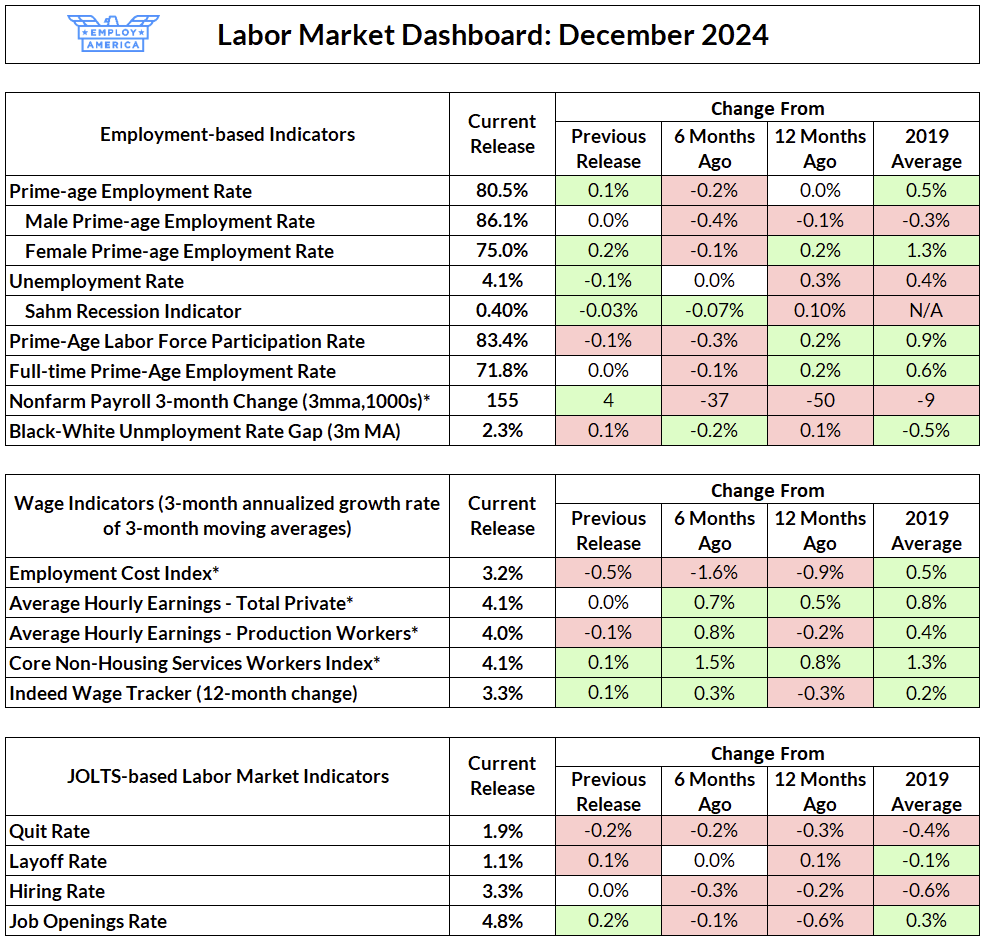

The labor market added 256,000 net jobs in November, with minor revisions to previous months. The unemployment rate fell by 0.1pp to 4.1%; prime-age employment rose by 0.1pp, and prime-age labor force participation fell by 0.1pp. The rise in prime-age employment follows a 0.5pp decline in the latter part of 2024. Average hourly earnings growth fell to 28bp month-on-month, bringing the year-on-year growth rate down slightly below 4.0%. Quits fell back to 1.9%, reversing its rise last month. Job openings rose.

Reading through the BLS report, there is a lot of “little changed over the month, and little change over the year.” In terms of levels, the labor market is broadly similar to last month—which means the further slowing we were worried about last month, particularly in the prime-age employment rate, did not materialize. This sets back expectations for earlier and more rate cuts this year, but it’s certainly a good report for anyone concerned about the left tail of labor market risk.

A Rebound in the Household Survey

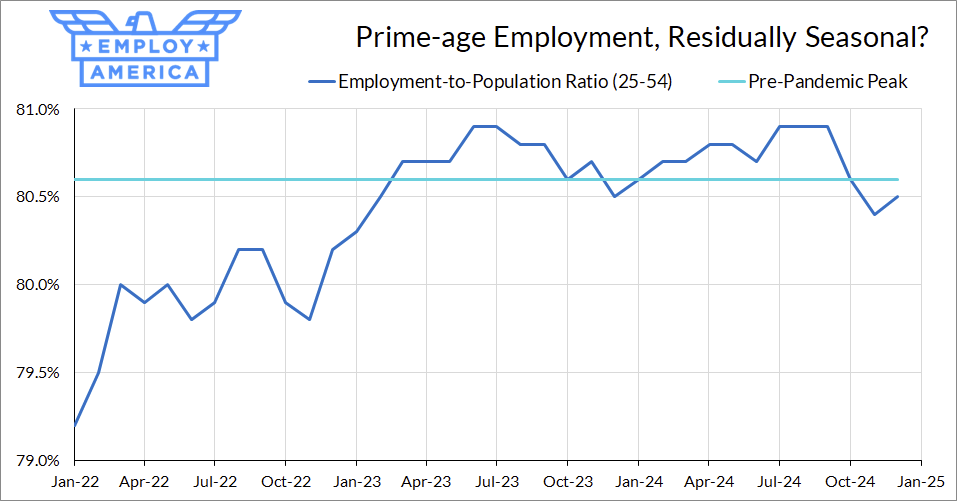

In previous months, we’ve flagged the falling prime-age employment rate as the most concerning figure in the jobs data. Despite the fact that the unemployment rate had stopped moving upwards, the prime-age employment rate had fallen by 0.5pp in just two months. However, we also saw a decline in the prime-age employment rate towards the end of 2023 before it rebounded back to decades-high levels. Today’s report is evidence either in favor of the recent decline being attributable to residual seasonality, or some local weakness that has reversed.

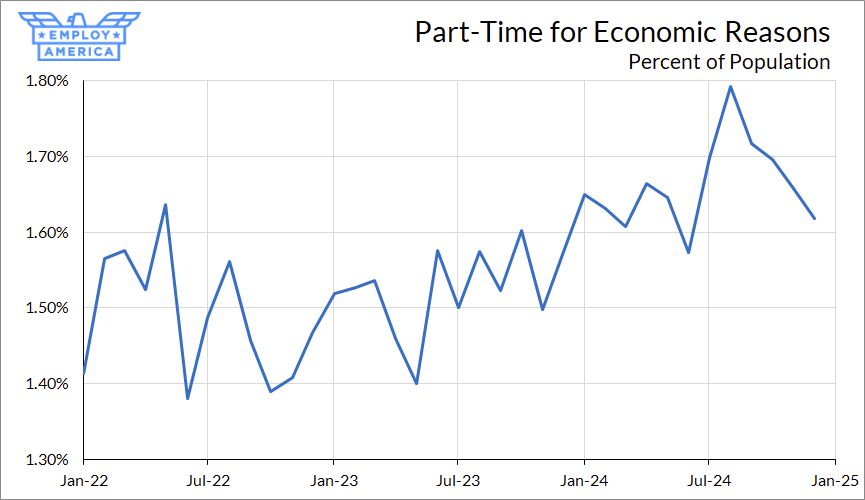

Some of the more niche indicators in the household report also show a reversal in some of the weakness earlier this year. The share of the population working part-time for economic reasons (insufficient demand) was on the rise since the beginning of 2023, but over the past few months has fallen back to January 2024 levels.

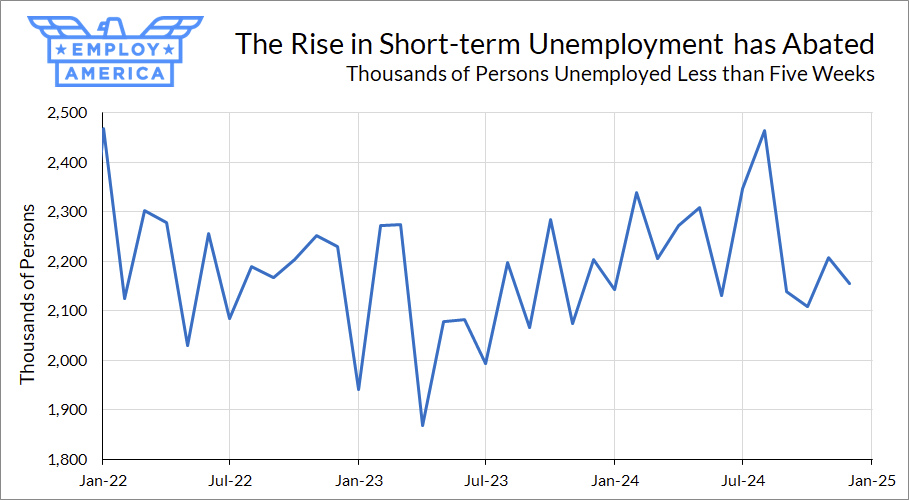

The number of short-term unemployed—those who recently became unemployed (think layoffs) and hadn’t been able to find a job by the time of the next survey followed a similar pattern.

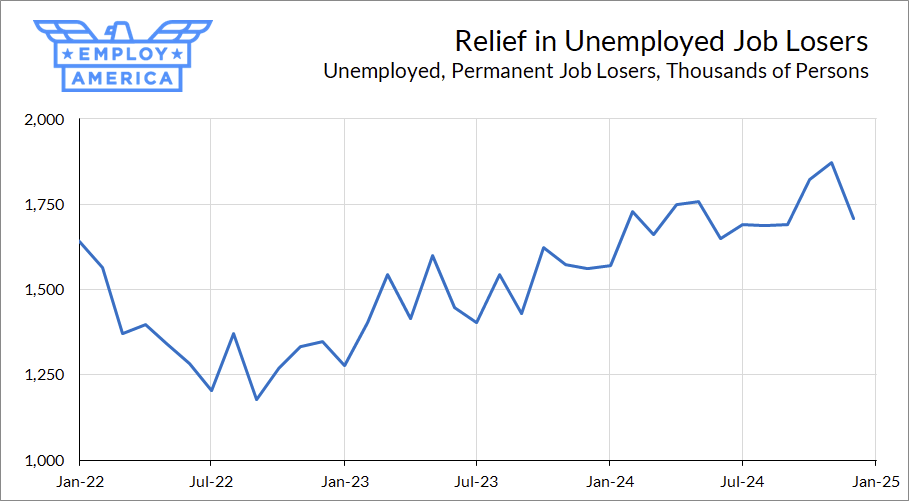

December also saw a fall in the number of unemployed persons who are permanent job losers after seeing that number rise the previous two months.

Make no mistake: we’re not out of the woods yet, and we still think there’s still a possibility that labor market risk forces a Fed pivot this year. But this month’s data is definitely a small step away from that outcome.

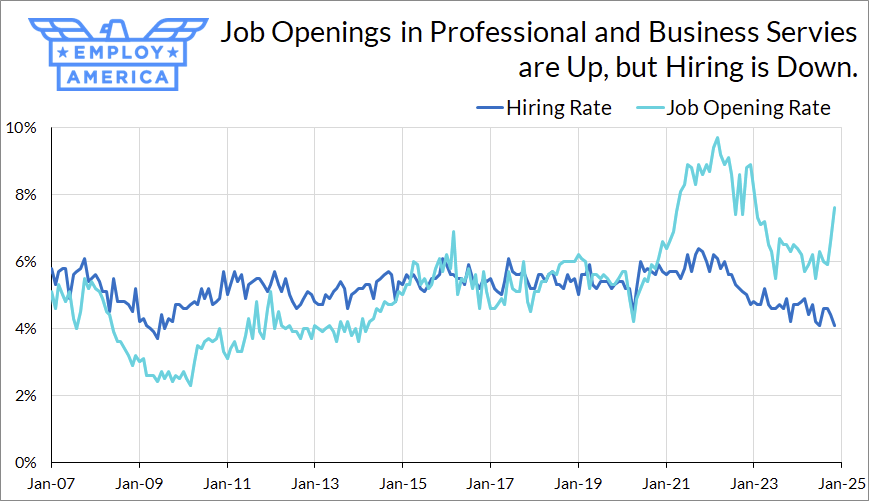

A Spike in Job Openings in Professional & Business Services

The downwards trend in job openings appears to have stalled or even reversed, as job openings rose for the second month in a row. In the latest release (covering November), the increase in job openings was entirely accounted for by the growth in job openings in professional and business services.

This beat in job openings coincides with the hiring rate in this sector falling to levels not seen since the depths of the Great Recession. In 2024, the job openings vs. other indicators debate has been quiet as they’ve been broadly moving in the same direction, but this sector is a great demonstration of the discrepancy between job openings and other indicators. Looking back through the past few years, it’s remarkable how insensitive actual hires are to job openings in Professional and Business Services—hire rates barely rose during the recovery. Don’t assume the beat in job openings is necessarily going to translate into a pickup in hiring activity.

A New Stage of the Expansion

Over the last year, we’ve seen falling inflation, a gradual softening of the labor market into something that looks, for now, to be relatively stable around levels seen in the late-2010s. Many labor market indicators are basically where they were at the beginning of this year. The Fed may not want to declare victory on the soft landing, but it’s clear we’re in a new chapter of this economic expansion.

What are the challenges to the labor market in this part of the cycle? Here are a few risks we think deserve greater attention (subscribers to MacroSuite will have seen some of this earlier).

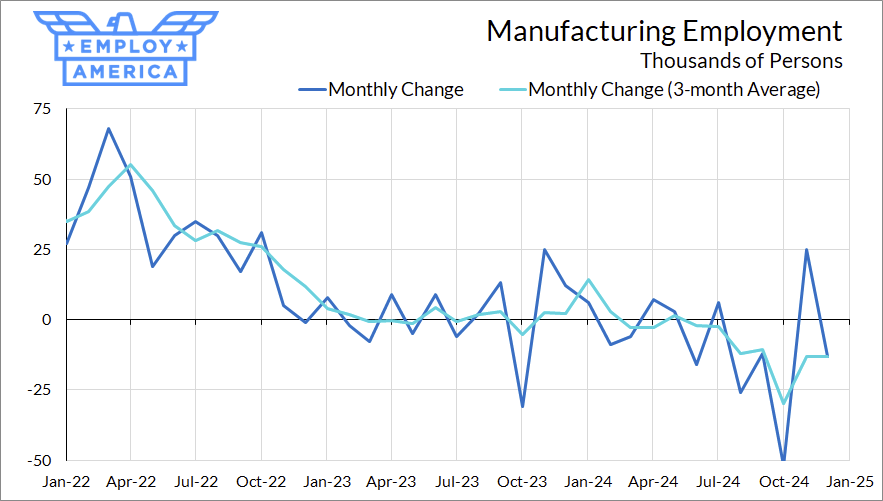

Sectorally speaking, employment growth is relatively strong in acyclical industries like education, health services, and government, and relatively weak in cyclical industries. Manufacturing employment has been shrinking over the latter half of 2024, and December’s report showed a fairly broad decline in durables manufacturing employment.

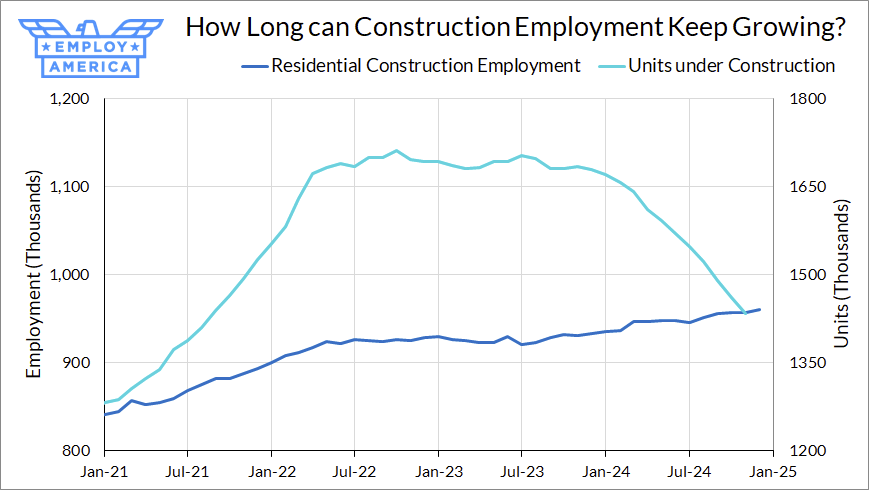

Construction employment is still growing, but housing activity is falling, with fewer projects in the pipeline to maintain construction levels. The ratio of residential construction employment to units under construction is nearly back to late-2010 levels, and the outlook for 2025 looks increasingly challenging. Mortgage rates haven’t fallen even as the Fed has begun easing, and tariffs may tariffs potentially raise construction costs.

We are likely to see the tech investment boom continue in 2025 and provide a tailwind to investment, GDP and productivity growth, at least in the near-term. The flip side of this is that financial indices are becoming more and more weighted towards the tech, especially the largest tech companies. The risk of a downturn following a tech downturn that is not fully offset by other sectors is rising.

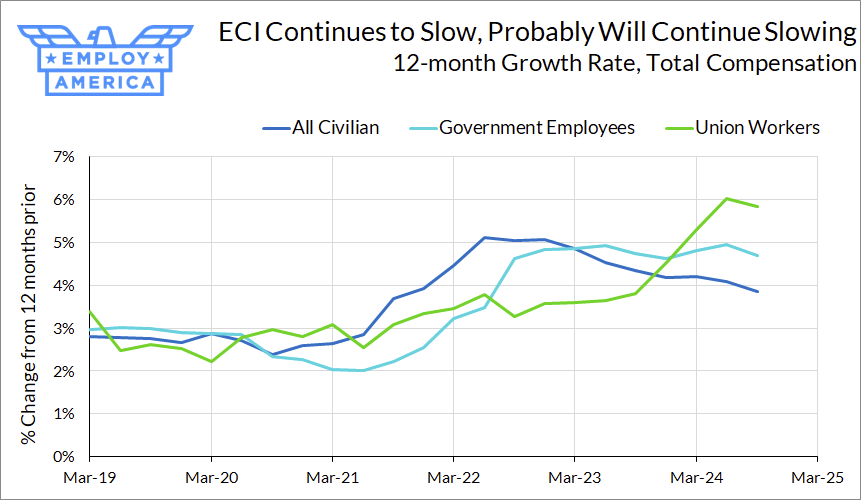

Finally, employment has started to move sideways. This means that sustained labor income growth needs to come from wage growth. Currently, wage growth is robust by historical standards, but there are portents of slowing. The Indeed Wage Tracker is still reading below 3.5%, indicating further room for wages to slow from here. As we observed in the last ECI release, wage growth is highest among government employees and union workers, where wage growth generally lags others workers.

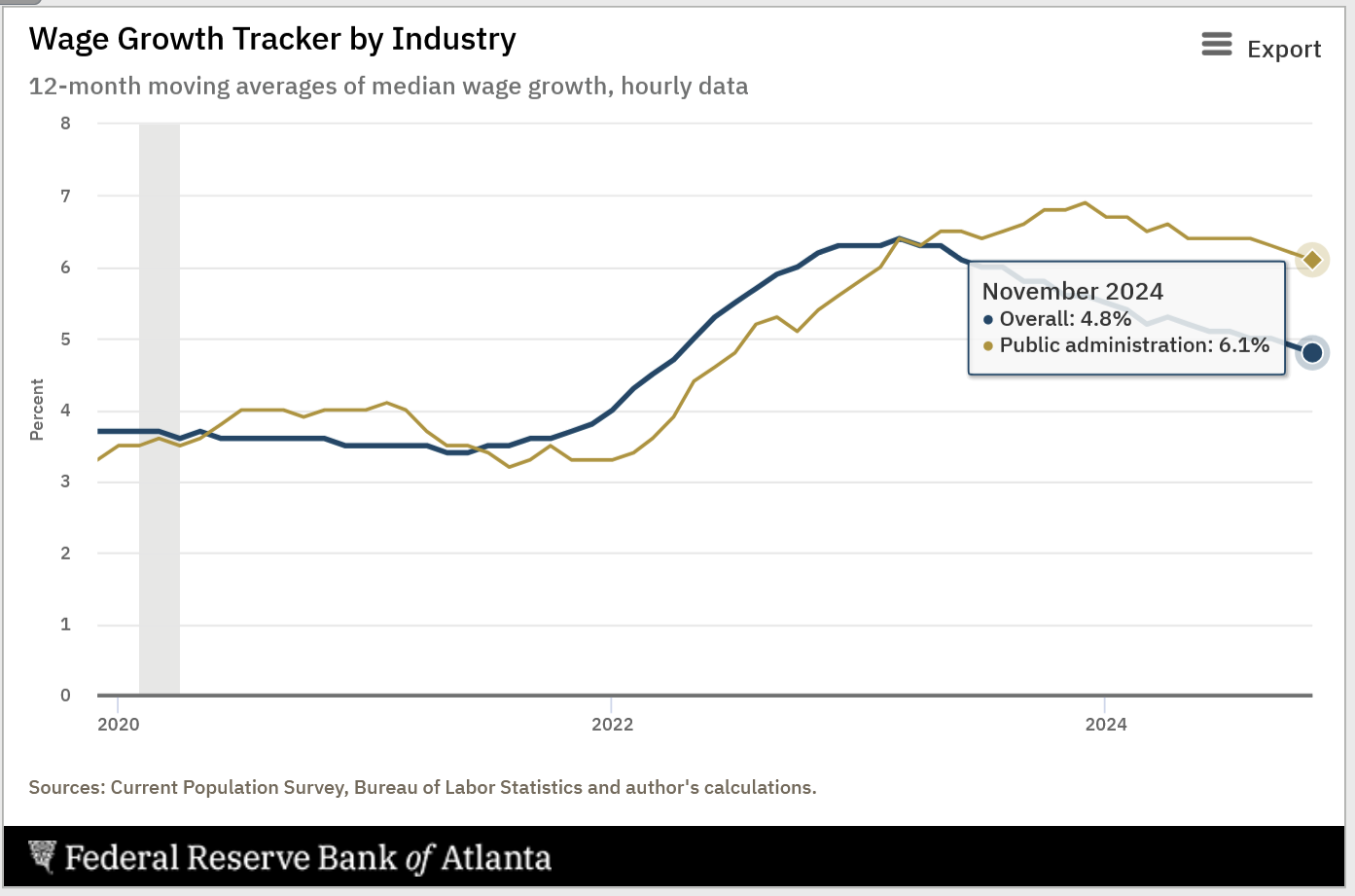

For more recent data, we also see this in the Atlanta Fed’s Wage Growth Tracker, which shows public administration wage growth pulling up overall wage growth.

As we pointed out in our series on productivity growth in the 1990s, the second phase of that expansion was characterized by a rotation from employment growth into wage growth, keeping labor income and consumer demand robust. Now that we’ve seen employment growth stagnate, the labor market needs to keep sustaining wage growth if the expansion is to continue.