Post-June FOMC: By Overreacting Hawkishly, the Fed Risks Being Behind the Ball

If the next month delivers either another round of soft inflation data, or a weak jobs report, the FOMC should be prepared to deliver a cut in July. If they continue to delay beginning rate cuts to gain certainty, they should consider a 50 bps cut for their first cut.

Although we have thought the economic situation merited consideration of normalization cuts since late last year, the FOMC held rates steady at the June meeting while raising their forecasts for interest rates through the end of the year. This hawkish trajectory was attributed to changes in the Committee’s inflation forecast at the press conference. We think the change in the Fed’s interest rate projections represents an overreaction to those changes in the inflation forecast, and would like to see more discussion of cuts as early as the July meeting, as floated by Board Member Alan Blinder, if the June inflation data cooperates.

We continue to advocate for policy in line with the plan we previously laid out for interest rate normalization— adjusted for this year’s path of realized inflation. If the Fed continues to push off the beginning of normalization as inflation cools, they risk finding themselves behind the ball amidst an industrial slowdown and cooling labor market. If they wait too long to start and find themselves playing catch-up, they should consider a 50 basis points cut when they finally start.

Inflation Forecast Worries Rates Forecast

The Fed held rates steady at the June meeting, with members worried about the inflation forecast raising their projections for future interest rates.

This week’s meeting saw the FOMC hold the federal funds rate steady and raise their projections for the interest rate path. The Committee moved from March’s median projection of three cuts in 2024 to an SEP where eleven of nineteen members are projecting one or zero cuts (implying that several members took off at least two cuts for this year). This looks a lot like the hawkish scenario in our FOMC preview.

When asked why the median rate path changed by so much, Powell was clear: the Committee was spooked by changes to their inflation forecast:

Neil Irwin: “Can you provide some color on what change in attitudes on the Committee over the last three months to see a much shallower path of rate cuts this year?”

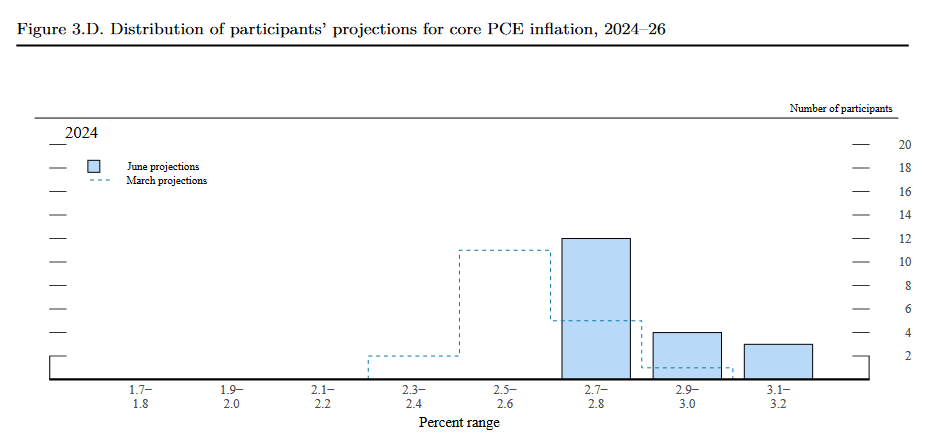

We can see this in the committee’s projections for core PCE inflation. Committee members’ core PCE inflation predictions for this year moved up substantially, with no member projecting lower than 2.7% by Q4 2024.

Between the March and June FOMC meetings, the Committee has seen nearly three months of inflation data come in: March (hot), April (warm), and the CPI read for May on the day of the June FOMC press conference (cool). Powell himself admitted that the inflation projections had a conservative bias:

Even given the conservatism of these inflation projections, taking two cuts off the table for 2024 is an overreaction. The upwards movement in the Committee’s inflation projections are on the order of 25 bps. This could plausibly justify taking one cut off for this year, but a 50 bps increase to the trajectory is an overreaction, especially given how far we are above the interest rate levels recommended by Taylor rule approaches.

Overreacting to Inflation While The Labor Market Cools

From our perspective, the Fed’s changing interest rate projections look like a worrisome overreaction, given the cadence of realized inflation and the slowing of the labor market.

Inflation

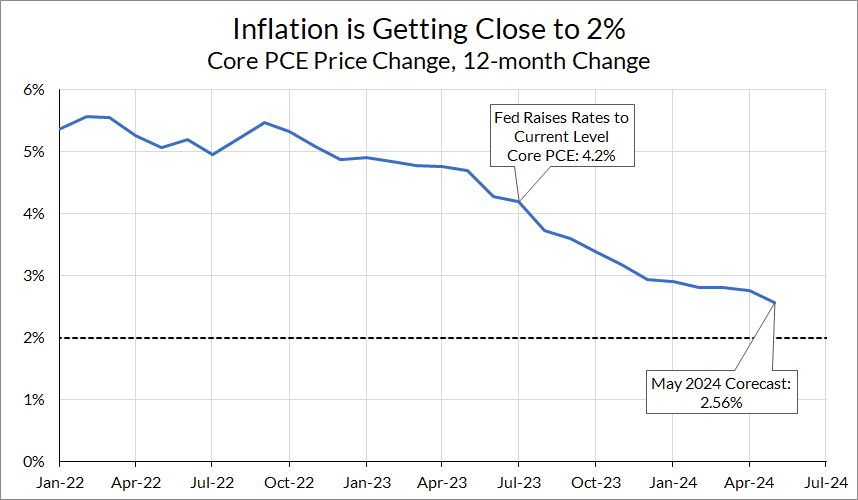

The simple fact is that in a longer-run view, inflation has fallen greatly. Whether you start from its peak at 5.6% in February 2022 or 4.2% when the Fed raised rates to the current level, core PCE inflation—which is on track to deliver a 2.6% year-on-year read for May 2024—is most of the way back to 2%.

Source: Bureau of Economic Analysis, Author’s Calculations

The inflation outlook is pointing towards further cooling. Rent and owner’s equivalent rent now accounts for nearly two-thirds of the excess of core PCE inflation above 2%, which should mechanically follow the much softer new tenant rent indices. The uncertainty there is about when exactly that softening will trickle through to measured inflation, not about the underlying dynamic. Auto prices, which were actually firm in May, are likely to contribute more to disinflation in the coming months given trends in private data on car prices.

Obviously inflation is not at 2 percent, but the steady and significant progress in core PCE inflation should be enough for the Fed to start backing away. As Powell and other Committee members have repeatedly said, the Fed should not wait until inflation is literally at 2% to cut. The threshold for cuts over the next few months should not be very high. As Powell said in his interview with 60 minutes earlier this year:

We just want to see more good data along those lines. It doesn't need to be better than what we've seen [in the latter half of 2023], or even as good. It just needs to be good. And so, we do expect to see that. Jerome Powell, February 2024 60 Minutes Interview

And this week, on the Committee’s new, higher inflation projections:

It is entirely possible that year-on-year core PCE inflation readings stall out or even rise slightly over the next few months, even with good month over month prints (as the Fed’s new inflation projections would imply) due to the base effects from low inflation prints in the back half of last year. It would be a small increase in the longer-run context of inflation, and in the greater context of the inflation trajectory, this should not spook the Fed. Moreover, to the extent that rising year-on-year measures reflect base effects from low inflation prints last year, the Fed should not overreact to those months’ base effects (after all, they promised not to overreact when we got those months’ low inflation prints).

The Labor Market

Meanwhile, the labor market hasn’t quite broken yet, but has been steadily cooling. The unemployment rate is now at 4%, at the committee’s projection for the end of 2024. Quits and hires have fallen below 2019 levels, and the job openings rate, which many committee members have relied on as a sign that the labor market is too tight, is now within pre-Covid levels.

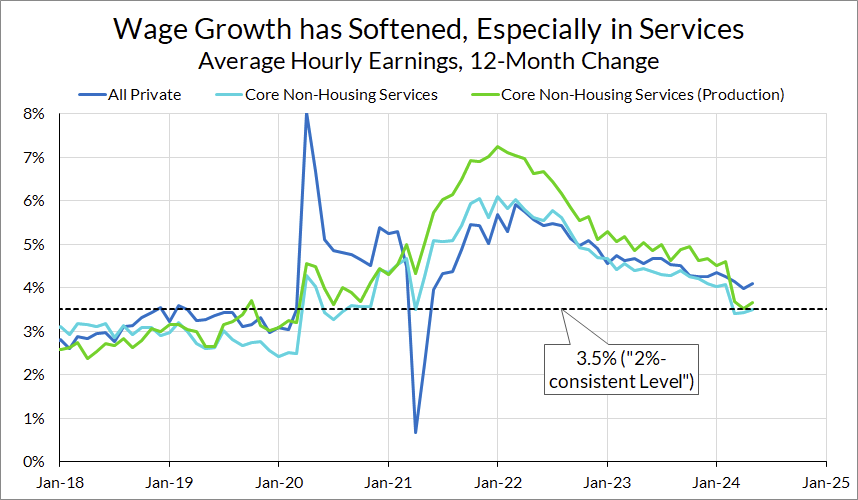

Wage growth, which Powell brought up as one source of inflationary pressure, has been steadily falling:

As I mentioned, the labor market has come into better balance. Wages are still running, you know, I would say, above a sustainable path, which would be that of trend inflation and trend productivity. You're still seeing wage increases moving above that. We haven't thought of wages as being the principal cause of inflation. But at the same time, getting back to 2 percent inflation is likely to require a return to a more sustainable level, which is somewhat below the current level of increases in the aggregate. Jerome Powell, June 12, 2024 FOMC Press Conference

Like inflation, wage growth has also been falling on a year-on-year basis. And in the core services ex-housing sector—the one that Fed officials believe is most driven by wage growth— wages have fallen even further. While wage growth is still a bit above the 3-3.5% range the Fed thinks is 2%-consistent, it’s not far off. Similar to how Committee members have said they should not wait until inflation is literally at 2% to cut, they should also not wait for wage growth to return to its supposed inflation-consistent range to be comfortable cutting.

Source: Bureau of Labor Statistics, Author’s Calculations

In short, there isn’t that much more room for the labor market to cool without falling short of full employment.

The Case for Normalization Continues

We believe the economic situation still merits the policy approach we put forward at the end of last year.

At the beginning of this year, we proposed a three-part framework for how the Fed should approach interest rate normalization. While high inflation readings in the first quarter of the year pushed the timeline for normalization back, we think the general strategies still apply: front-load rate cuts, follow inflation down, and remain flexible with respect to the end destination of the target rate.

With May’s inflation data in hand, inflation looks to be back on the disinflationary trajectory. Based on CPI and PPI data, our current corecast has May Core PCE growth tracking at a mere 0.08% growth rate. Between now and the July FOMC meeting, the Committee will see one more month of both jobs and inflation data. If the next month delivers either another round of soft inflation data, or a weak jobs report, the FOMC should be prepared to deliver a cut in July.

The common refrain from Committee members is that they still need to see more months of good data. If the next month of data is good but the Committee feels like they need even more months of data, they start running into a trade-off between certainty and timeliness; the longer they wait for more months of data to give them more certainty, the more they risk being behind the ball when they finally start normalization.

If the FOMC continues to delay beginning rate cuts to gain certainty, they should consider a 50 bps cut for their first cut when they finally do move, to make up for lost time. As we laid out in our case for rate normalizaton, risk management and uncertainty about where the neutral rate is imply that rate cuts should be faster in the beginning (when we know we’re restrictive) and slower as the Fed feels out the neutral rate.

The Fed has held off on beginning rate normalization so far after a bumpy Q1 in inflation. It was understandable that the Committee wanted to wait to see whether the early 2024 data was a sign of a resurgence of inflation. However, now that evidence is gathering that the hot Q1 prints were more attributable to residual seasonality, it’s time for the Fed to start getting prepared for rate normalization.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.