With the labor market still strong and April inflation representing an improvement over Q1 but still not good enough, the committee is in “looking for confidence” mode.

If you enjoy our content and would like to support our work, we make additional content available for our donors. If you’re interested in gaining access to our Premium Donor distribution,please feel free to reach out to us here for more information.

Latest Fedspeak and Dot Projections

What to look for:

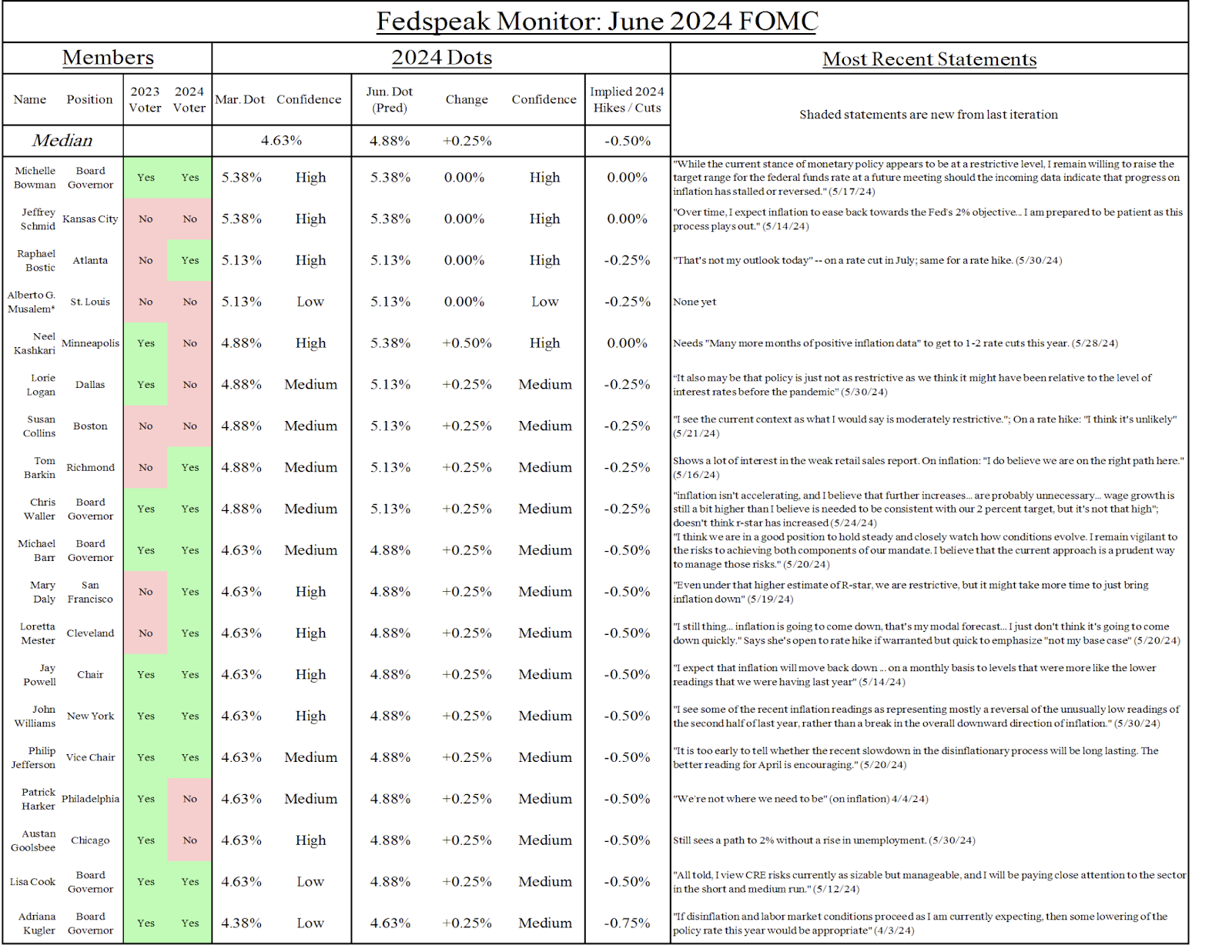

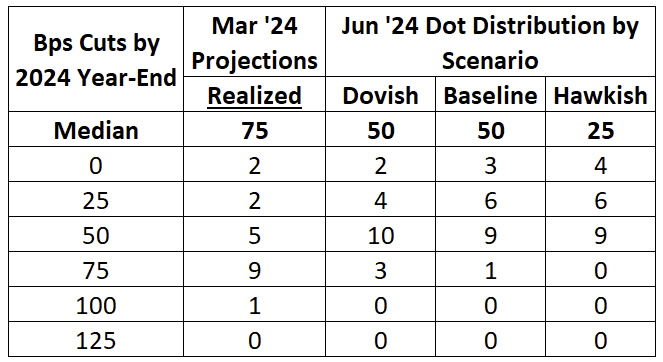

A hold and a movement up in the dots: We expect the dots in the Summary of Economic Projections to move up; the question is, by how much. The previous SEP put the median member at three cuts, but only barely, with nine of nineteen members at two or fewer cuts. We expect the median FOMC member to be at two cuts this meeting, but again only barely. Our baseline has every member except for Bostic (who recently explicitly put himself at one cut), Bowman, Schmid (who we believe are at zero) taking one cut off the table, with Kashkari taking two cuts off and moving to zero cuts.

Why: With the labor market still strong and April inflation representing an improvement over Q1 but still not good enough, the committee is in “looking for confidence” mode. While there has been talk of the potential need for further rate hikes, even the most hawkish members have refrained from rate hikes as their base case. The May labor market report was sufficiently soft in the headline numbers (unemployment rate at 4%, job openings back to 2019 levels) that most of the committee will not want to take off more than one cut.

Hawkish risk: The risk from our baseline is to the hawkish side, and we would not be surprised to see Mester move from three cuts to one cut, moving the median to one. However, the recent fedspeak (see below) has taken on an optimistic enough tone that our baseline remains at two cuts.

Powell will try to keep the press conference as boring as possible. After a hot Q1 for inflation, the committee is going to want to see more months of good inflation data before they feel comfortable lowering rates (barring a sharp downturn in the labor market). To preserve optionality, Powell will likely continue to emphasize data dependence.

The Developments That Matter:

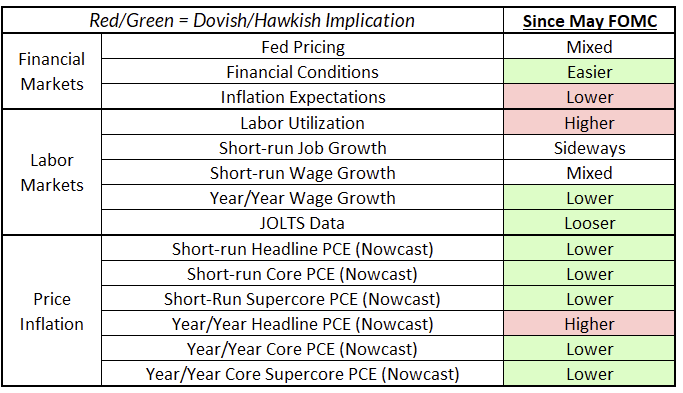

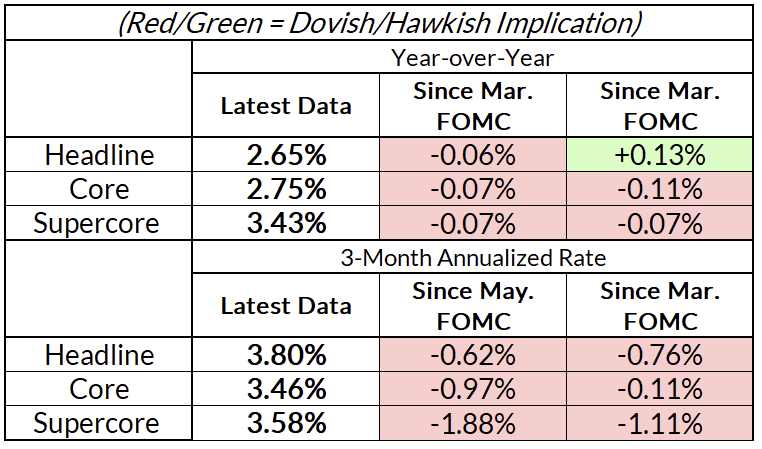

Since the last meeting, the Fed has seen the April jobs report, April inflation, and May’s labor market data. April inflation was certainly not as hot as bad as Q1, but still not sufficient to signal imminent cuts. Core services ex-housing inflation eased but core goods, particularly in apparel, delivered some upside surprise. While we think it’s likely that we will see significant progress over the next few months in rent, owner’s equivalent rent, food services, and weirdly-measured components in financial services and input cost indices-based social services, the Fed is not going to want to move until progress actually materializes. The modal reaction from the committee has been that Q1 was simply a bump in the road, and we now appear to be back on track.

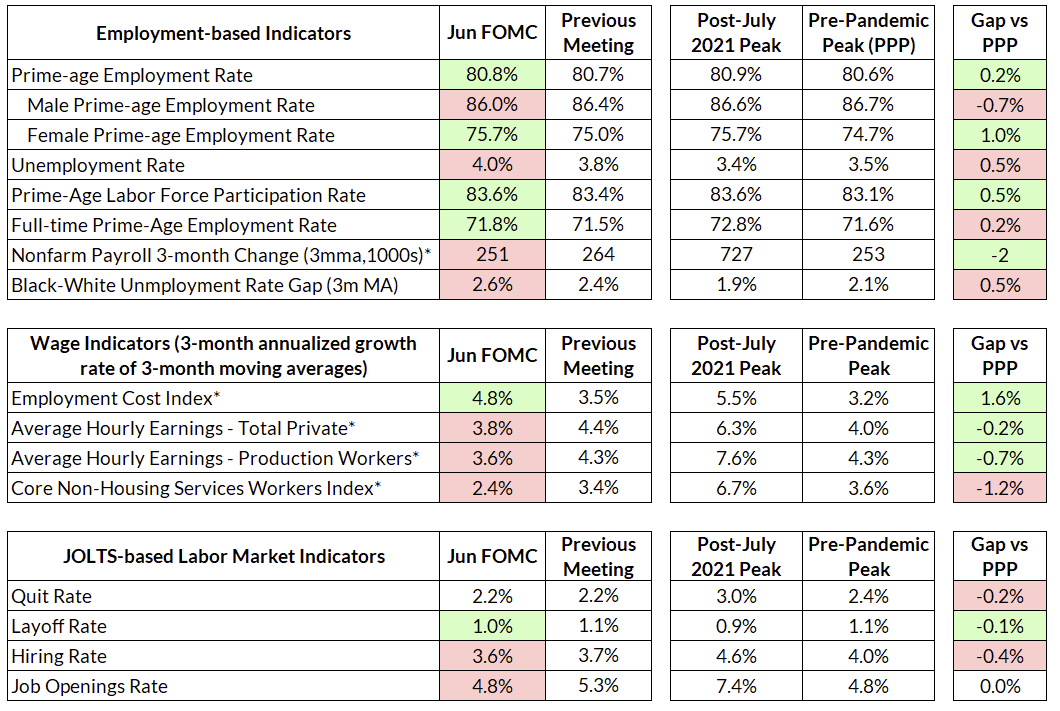

Turning to the labor market, unemployment has steadily crept up over the past few months and is now at 4% for the first time in this cycle. Job openings, a metric the Fed cares a lot about, fell sharply in April and are now at pre-2020 levels. On the other hand, payroll employment growth and wage growth were high in April.

Key Fedspeak Since Last Meeting:

Powell (5/14): "I expect that inflation will move back down ... on a monthly basis to levels that were more like the lower readings that we were having last year"

Waller (5/21): "the inflation data for April suggests that progress toward 2 percent has likely resumed... the data suggests that inflation isn't accelerating, and I believe that further increases in the policy rate are probably unnecessary... If I were still a professor and had to assign a grade to this inflation report, it would be a C+—far from failing but not stellar either."

Collins (5/21): “I think April data was welcome because it showed some additional rebalancing, which I think is important, and I do think suggested that the first quarter was a bit more of an interruption, but it's early.”

Mester (5/20): "I still thing... inflation is going to come down, that's my modal forecast... I just don't think it's going to come down quickly."

Logan (5/30): "I think there's good reasons to think that we're headed to 2% - we're still on that path, perhaps a bit slower and a little bit bumpier than maybe many thought at the beginning of the year”

Kashkari (5/28): On April inflation: "marginally better"; needs “many more months of positive inflation data" to get to 1-2 rate cuts this year.

William (5/30): "I see some of the recent inflation readings as representing mostly a reversal of the unusually low readings of the second half of last year, rather than a break in the overall downward direction of inflation."

Barkin (5/16): "I do believe we are on the right path here."

What we’re thinking

We’ve been saying that what’s important is that the Committee begins cutting as soon as they have that ‘bit more’ confidence, definitely in case of a downturn in the labor market. Not much appears to have changed in the Fed’s commitment to those two principles. We see favorable developments in inflation coming over the next few months, but the Committee will want to see that progress materialize in actual inflation prints before moving. While July is likely too early for the Committee, sufficient progress on inflation plus the notable softening in the labor market we’ve already seen puts September as the base case for the first cut.