If you enjoy our content and would like to support our work, we offer a premium, high-frequency macro research service, Macro Suite. If you’re interested in gaining access, please feel free to reach out to us here for more information.

What To Expect

Very little. The Fed signaled a pause after the December meeting, and without any compelling developments in either the labor market or the inflation front, that remains the case for January. Q1, which the Fed has been burned by before, still looms large—remember, we still haven’t received any inflation or labor market data from 2025 yet. Even if this was a non-election year, this would be a meeting where the Fed is looking to keep its options wide open and say as little as possible. Post-election policy risks only compound that desire for optionality. There has been little resolution during the lame duck period about policy uncertainty with the incoming administration.

Given how little has changed since the previous meeting, expect Powell to reveal as little as possible during the press conference. “We’ll be proceeding carefully, watching the data, and paying attention to both sides of our mandate. Policy is well-positioned. We’ll have to wait and see what happens with policies like tariffs and what the effects of those are going to be, there’s just tremendous uncertainty around that and I wouldn’t want to say more than that.” We might even see the return of “we just want to see more good data” when asked about the timing of further interest rates.

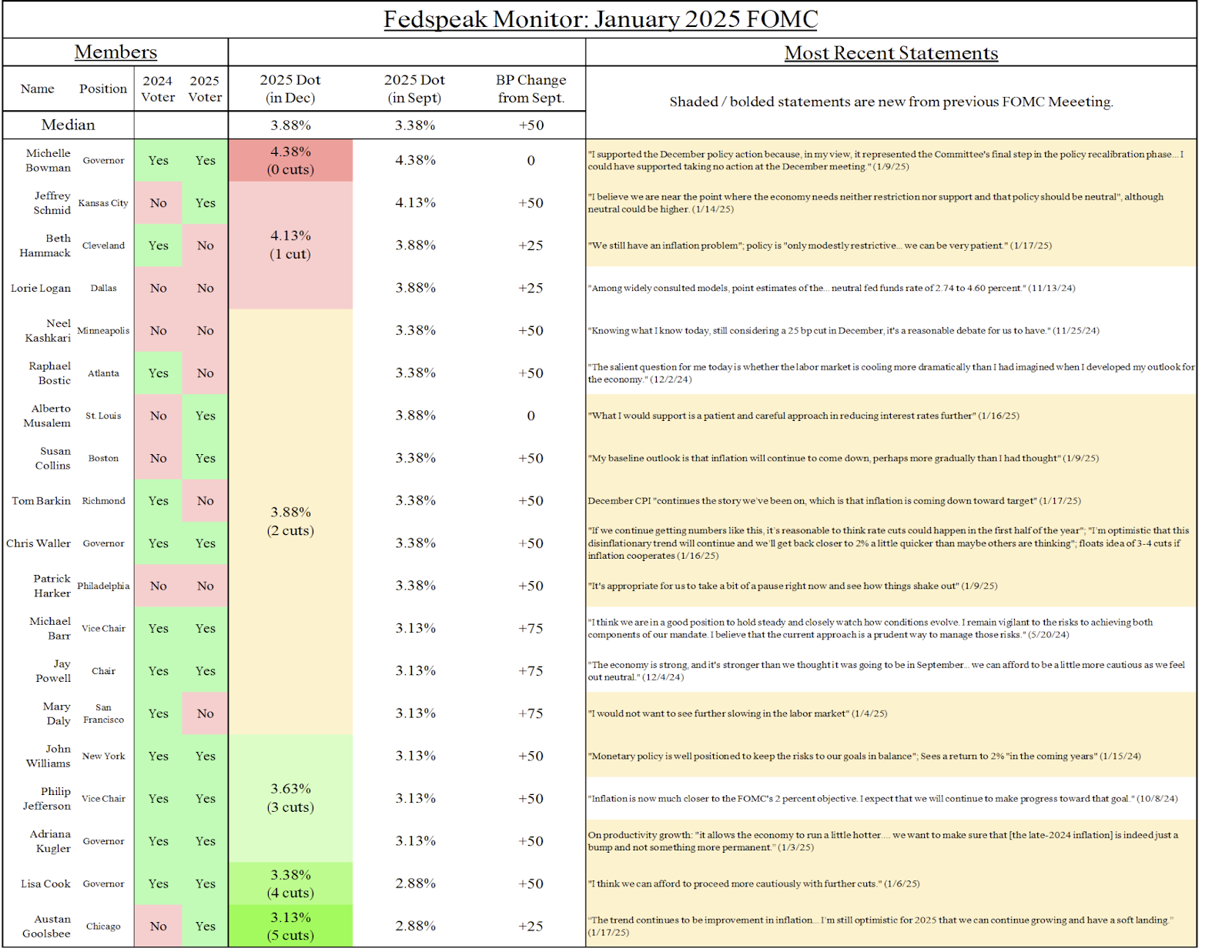

Latest Fedspeak And Dot Projections

The Developments That Matter

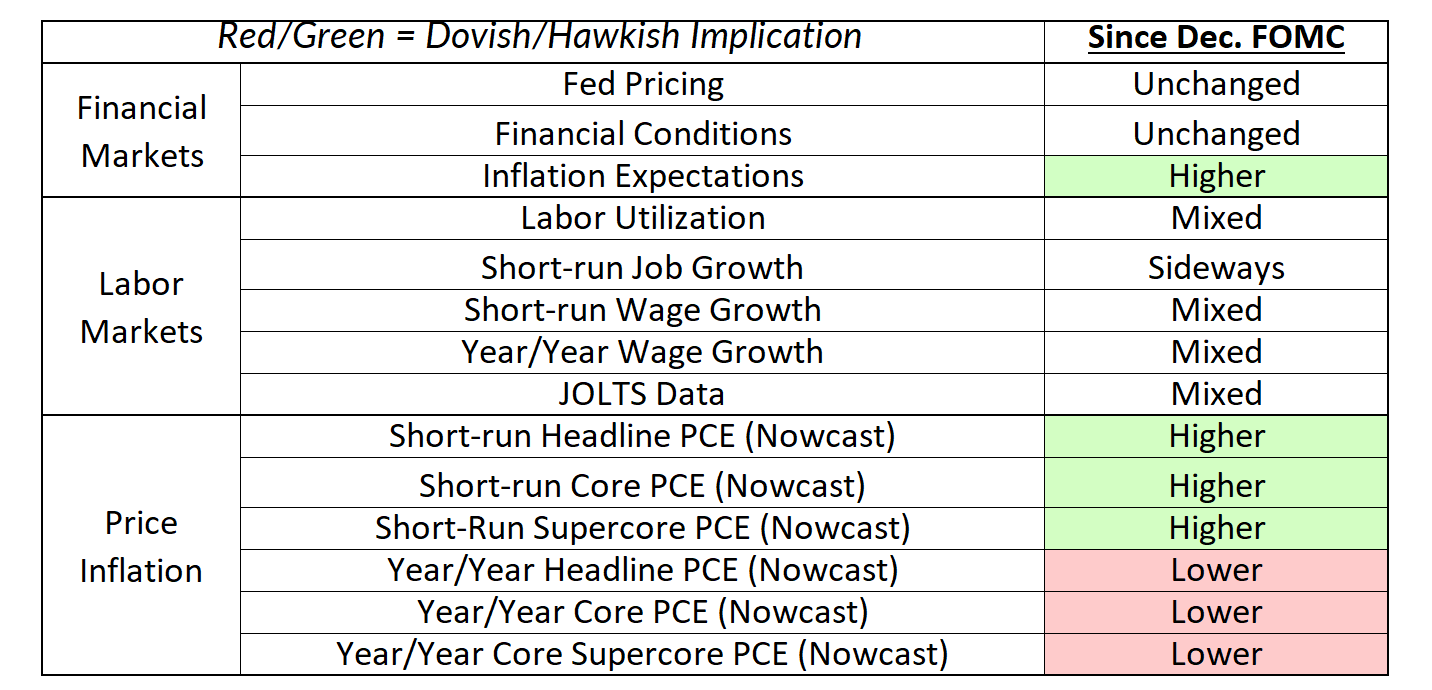

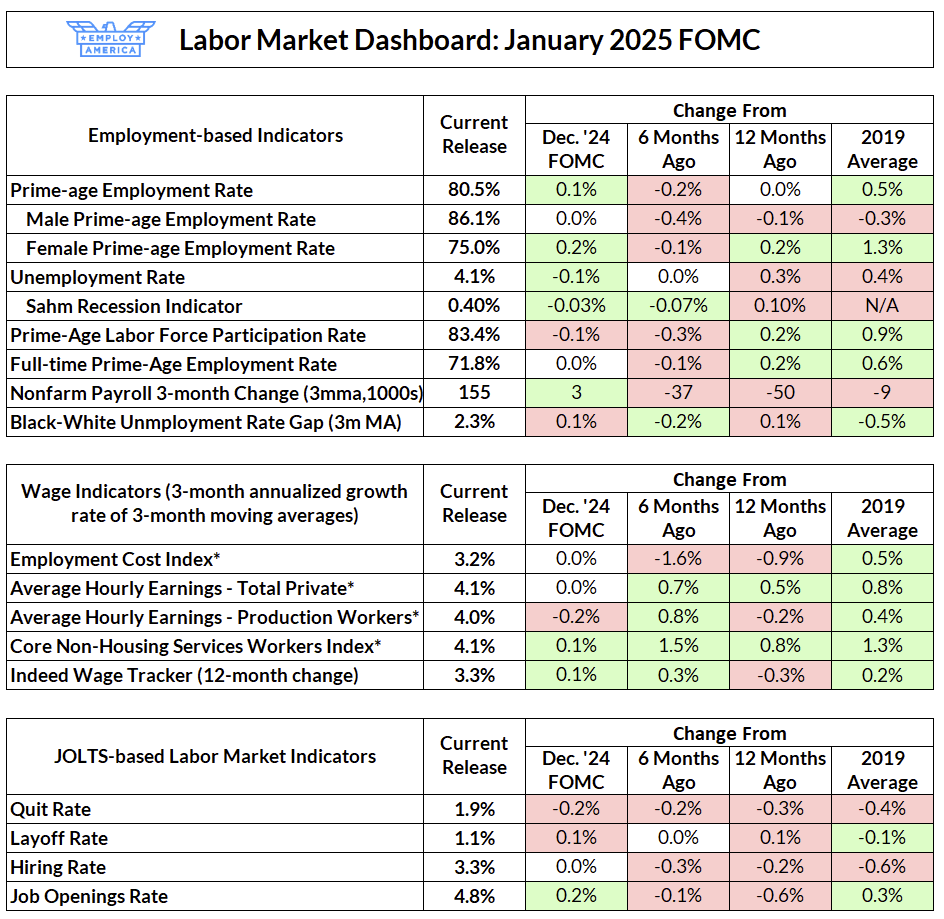

The December labor market data looked reassuring. The unemployment rate fell slightly, and the prime-age employment rate, which had fallen by 0.5pp in just the two prior months, rose slightly. Wage growth still looked solid, and job openings were up (although the quit rate is still below 2%). This doesn’t mean we’re out of the woods yet, but there’s no sign of a further labor market deterioration that would force another Fed pivot towards more cuts.

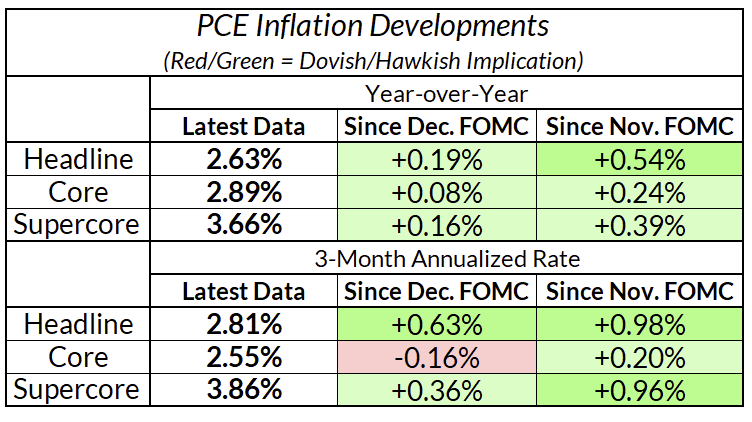

We also got another round of inflation data. While our current nowcast for PCE is for a fairly warm (24bp) increase in core PCE and a hot supercore reading because of airfares, the post-CPI Fedspeak (notably Chris Waller) seems to indicate that the Fed is forecasting a more tepid (but not cold) reading. Either way, the reading was not cold enough and still too soon to put off any fears that inflation is going to be stuck or that they’ll be burned by Q1 again.

Meanwhile, the presidency has changed hands, but we are not much closer to having a clear view of what economic policy will look like under a second Trump administration. Economic policy uncertainty is high, the administration’s tariff policy seems to change by the day, and President Trump is now openly calling for rate cuts. The most recent plan includes a 25% tariff on Canada and Mexico starting Feb 1, and the Financial Times reported that Treasury Secretary Scott Bessent is pushing for a universal, across-the-board tariff of 2.5% each month until tariffs reach 20%.

Finally, on Monday (1/27/2025) a tech-sector selloff occured due to concerns about the emergence of Chinese AI chatbot DeepSeek. DeepSeek operates at a fraction of the cost of comparable American AI chatbots which may put the CapEx plans of US tech and energy companies at risk. Given how heavily concentrated the equity market is around technology and AI adjacent companies, tech is now a macro story and the Fed should be diligently monitoring developments in the sector due to the implications for employment, fixed-investment, and the health of the broader equity market.

Key Fedspeak Since Last Meeting

Bowman: "Wage growth remains indicative of a tight labor market and above the pace consistent with our inflation goal."

Waller: "If we continue getting numbers like this, it’s reasonable to think rate cuts could happen in the first half of the year"

Goolsbee: "If conditions are stable and we don't have an uptick in the inflation rate... I think that the rates should go down to what I consider neutral."

Hammack: "I believe that monetary policy will need to remain modestly restrictive for some time... policy is not far from a neutral stance."

Schmid: "I believe we are near the point where the economy needs neither restriction nor support and that policy should be neutral"

Harker: "It's appropriate for us to take a bit of a pause right now and see how things shake out"

Daly: "[Cutting in December was a close call... we have now completed that recalibration"

Musalem: "What I would support is a patient and careful approach in reducing interest rates further"

What We’re Thinking

Given all the uncertainties facing the Fed, they’re right to want to avoid saying anything that will tie their hands down the road. As we wrote in our 2025 Fed preview, there are many plausible paths for the monetary policy trajectory this year, even without post-election policy uncertainty. This should include risks to the labor market. Even with last month’s labor market data, the unemployment rate is not far from breaching the projection in the SEP for 2025 (4.1% currently vs 4.3% projected by the end of the year). This signals a continuation of the Fed’s pivot in 2023 towards wanting to keep the labor market strong, but it also means that the threshold to adding further cuts is not very high. It is important that they do not foreclose the possibility of putting rate cuts back on the table.