Industrial Production

This is part of our Supply Chain Monitoring series usually made available exclusively for our Premium Donors. If you’re interested in gaining access to our Premium Donor distribution, please feel free to reach out to us here for more information.

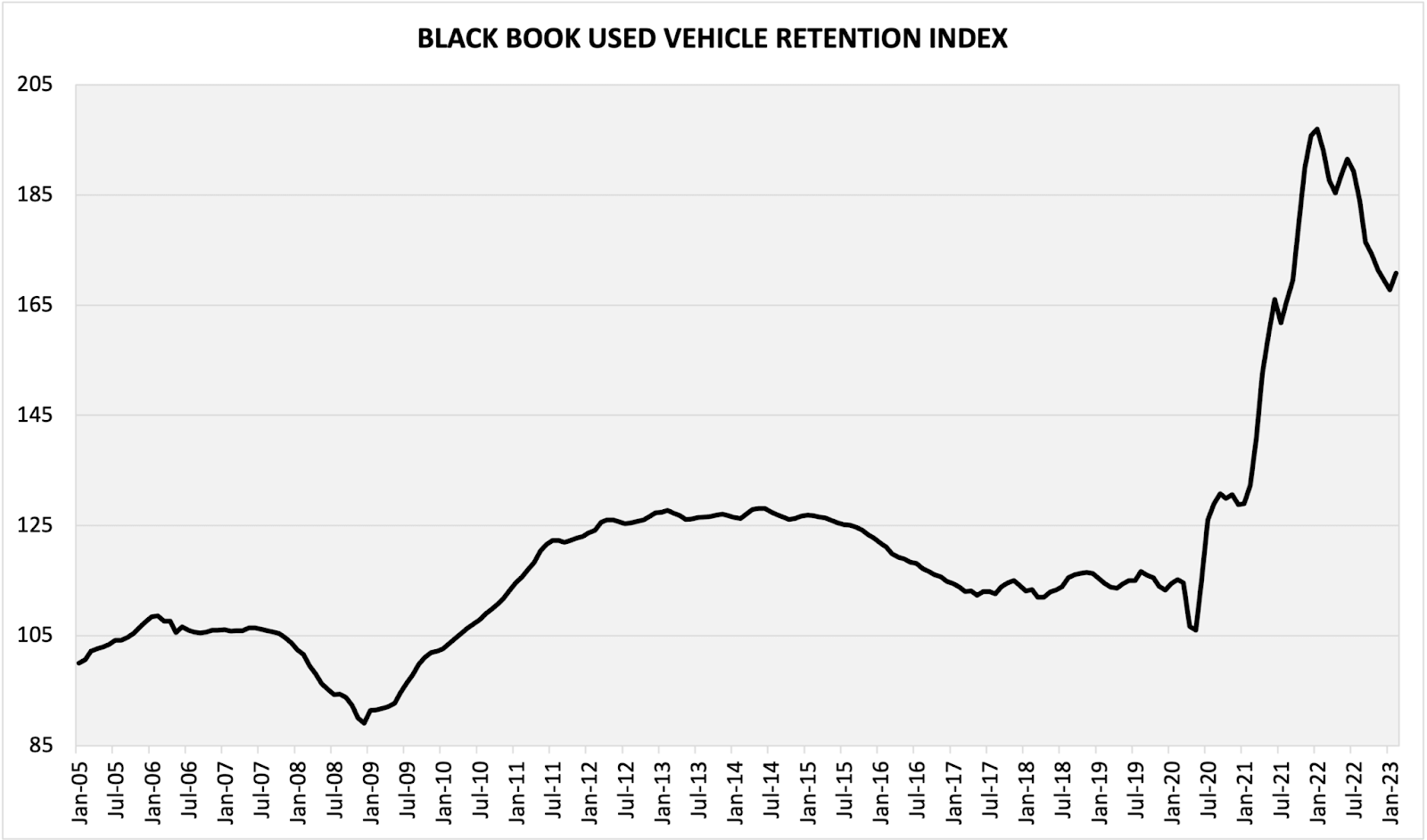

The semiconductor shortage has been a major narrative throughout the pandemic, as has the shortage of automobiles, which has only recently stopped growing.

The two phenomena have been closely linked, with automakers consistently reporting a lack of semiconductors and electronic equipment as a major hurdle to meeting past levels of output. Some have been hoping (myself included) that we would see disinflation or even outright deflation in used and new vehicles, but that has yet to meaningfully materialize. High-frequency used car data is also now showing an uptick in wholesale prices, which is not entirely unexpected as we have seen a 5 Million Car Hole develop on the supply side.

The price of autos is also important as the cost of retail car loans has long been considered a viable transmission channel through which interest rate policy could plausibly lower demand in the near term. Now that we are facing some supply constraints on auto production, we should be seeing at least a partial test of this idea over the next few months.

The fact that this disinflation hasn’t happened yet — and may even be reversing in the used market — has sparked some speculation about “supply discipline” from automakers looking to the upcoming EV transition or expecting falling demand. Given that we saw a similar dynamic from oil and gas producers early in the Ukraine war, that suspicion may prove warranted, but it is hard to say without fully exploring the situation.

So, has the semiconductor shortage really faded for producers now that it has dropped out of the everyday news? We can use our supply chain monitor to take a look at the state of things. Since the price dynamics in new and used autos will continue to be a major driver of the inflation picture throughout much of the rest of the year, whether higher or lower, it’s worth working systematically.

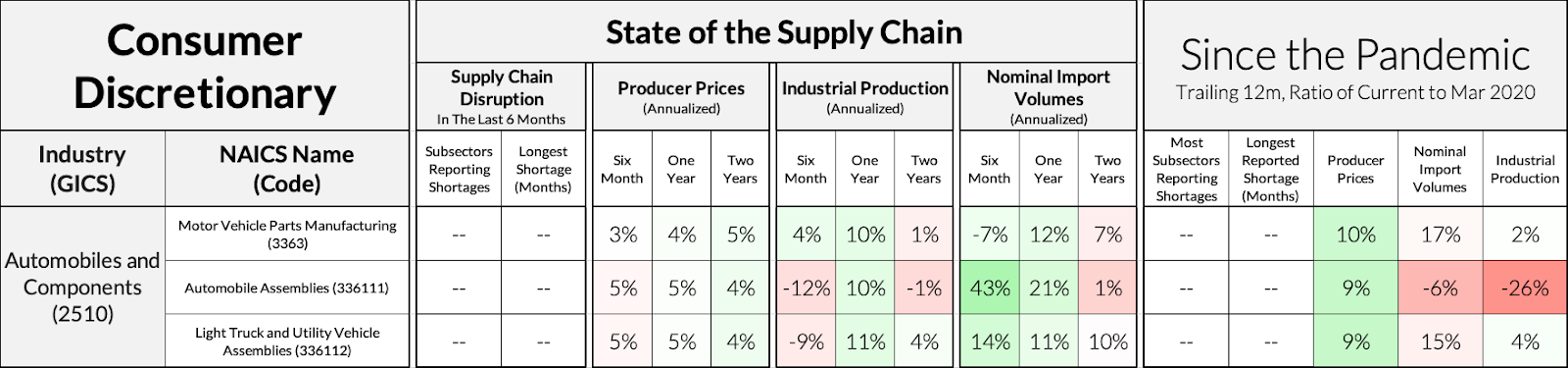

Auto production is down dramatically compared to pre-pandemic, and imports are down as well, exacerbating the problem of “missing vehicles.” Producer prices have increased substantially slower than the rate of consumer inflation over the pandemic, also ruling out rising prices due to cost-push factors. Industrial production has recovered over the last year, but it was recovering to catch up from an extremely depressed level, as we can see in the 26% drop compared to pre-pandemic output.

So that’s motor vehicle assemblies, but now let’s take a look at some other major industries that automobile manufacturers buy from. Per the BEA’s Input-Output tables, the top three supplier industries to auto manufacturing by nominal cost (excluding white collar services, and things like insurance and real estate) are:

- Semiconductor and Related Device Manufacturing

- Other Plastics Product Manufacturing

- Motor Vehicle Electrical and Electronic Equipment Manufacturing

The second and third categories are too granular for our supply chain monitor, but we do have Plastics Product Manufacturing and Electrical and Electronic Equipment Manufacturing, so we will use those as proxies.

That’s an awful lot of red! Each of these three supplier industries has seen substantial, disruptive, and long-lasting shortages both recently and over the duration of the pandemic. Industrial production is down nearly across the board in these industries. The few bright spots here are barely helpful for the problem at hand:

- Producer prices for semiconductors remain low, despite the shortages;

- We are importing substantially more electrical equipment and components than pre-pandemic;

- Domestic semiconductor production may be falling relative to earlier in the recovery, but it is still substantially higher than pre-pandemic.

Earnings calls also support this story of pervasive shortage, with Honda, Ford, and others expressing that although margins are improving, it has often been insufficient to make up for lost expected revenue over the relevant timelines.

But the thing is, we all know the EV transition is coming, and we all know that EV prices have been firmly above ICE prices for as long as both have been on the same market. Elevated prices — and thus padded profit margins — will likely smooth the on-ramp to EV adoption in two ways. On the business side, the higher prices will help offset the cost of capex involved in retooling facilities to build cars designed around batteries rather than gas tanks. Shifting to EV production will likely be a substantial lift in terms of equipment investment. Lower on-hand inventories will also likely help them adapt to finer-grained changes in demand between gasoline and electric vehicles. On the consumer side, one barrier to EV adoption has been the substantial distance in price between comparable internal combustion engine and electric vehicle models, with EVs consistently being around ten thousand dollars pricier. If prices for new and used vehicles remain elevated, that tradeoff may look different to consumers in the large.

So, it’s hard to say how much of this is intentional, but it does look awfully convenient to have to ration on quantity and also price ahead of a large and well-telegraphed (if not fully planned) sectoral shift. They do seem to still be having trouble getting the chips though, and other industries that produce key upstream components have also been reported in shortage. In any event, the timeline for disinflation in new and used autos is likely still longer than was previously appreciated.