Booming Productivity & Participation Alongside Slowing Income Growth: How The Labor Market Has More Than Rebalanced

Thanks to outperforming supply-side dynamics, the labor market has already rebalanced. At the same time, income growth is still decelerating and the lagging bits of the inflation overshoot are finally normalizing as a result. The August jobs report should shape how much and how fast the Fed should be cutting, but even a benign report would be consistent with normalizing interest rate policy.

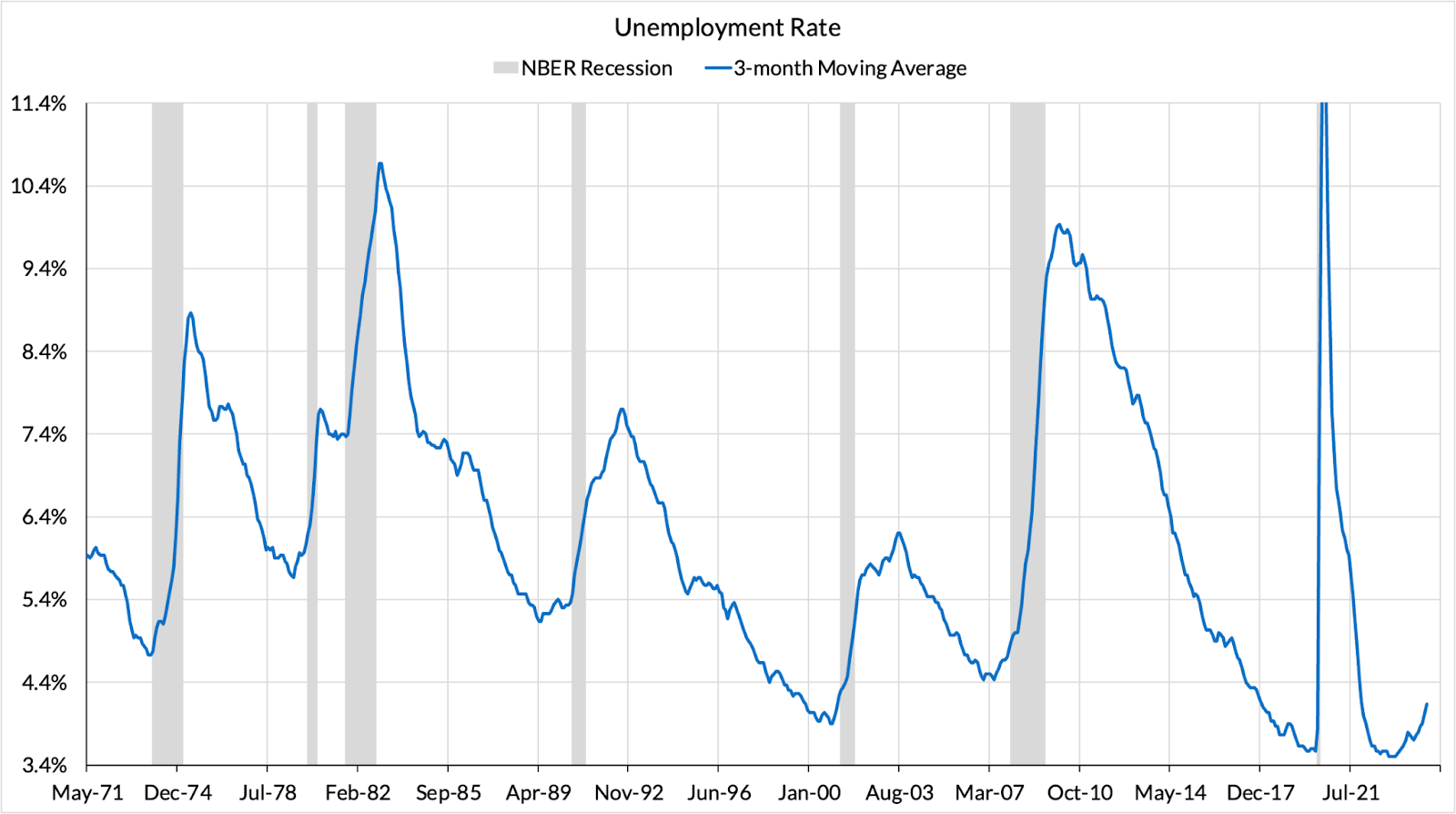

Macro discussions are rightfully fixated on the rise in the unemployment rate and what that might imply for recession risk scenarios. Even if we set aside the risk scenarios, the realized data have also shifted meaningfully:

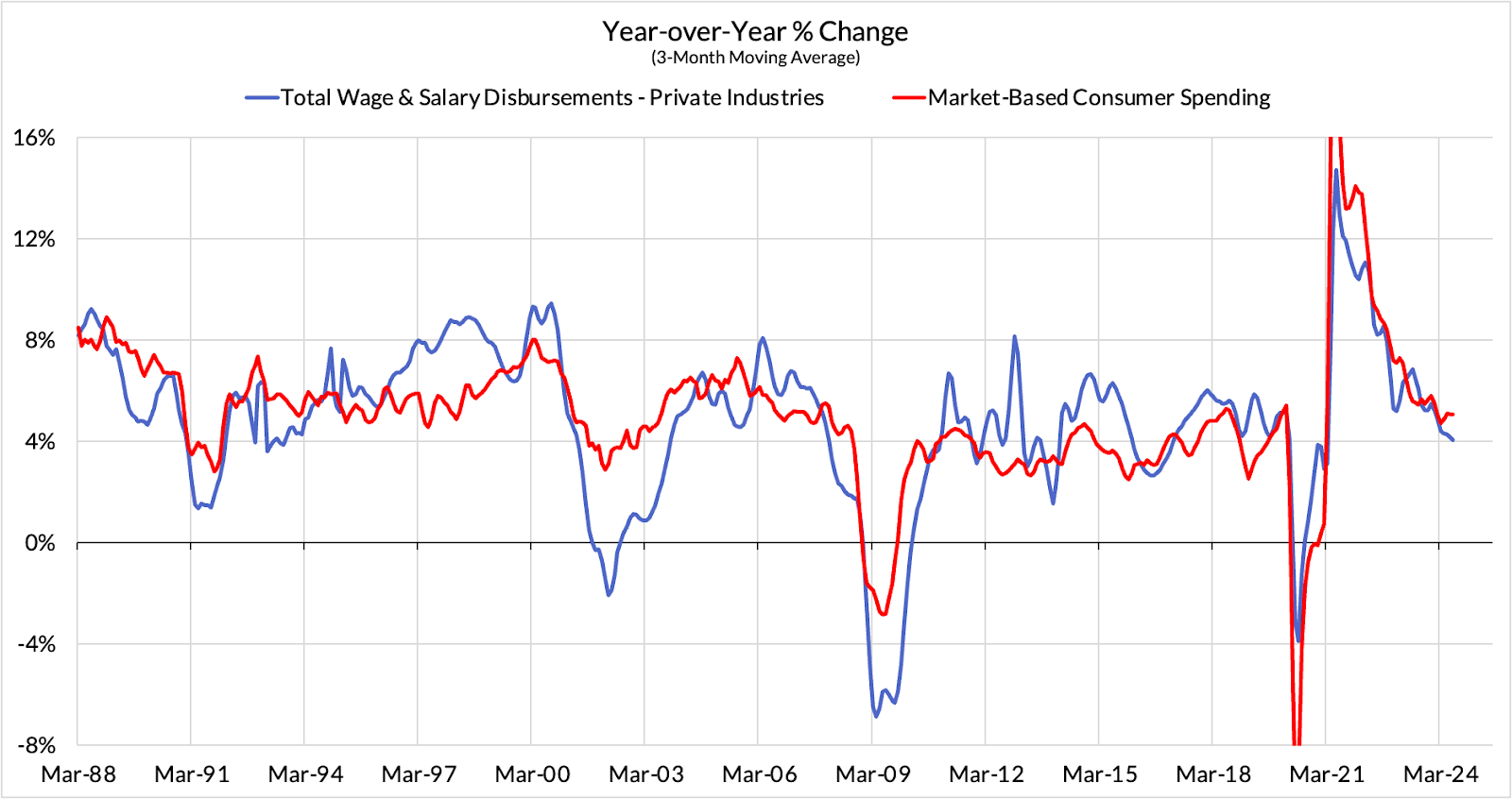

At the same time that these supply-side forces are supporting disinflation, local trends in gross hiring and job switching are implying job and wage deceleration as well. The growth in gross labor income–the cumulative sum of all jobs’ wages–is thus slowing, implying slower growth in consumption demand.

Both from the demand and the supply side, the labor market is increasingly consistent with disinflationary outcomes. The Fed should not require July’s rise in the unemployment rate to hold or deteriorate further in August as a precondition for a September rate cut. We have seen more than a complete rebalancing of the labor market.

Since the initial boom of reopening, the pace of labor takeup has been slowing, albeit from historically strong growth rates. The growth rate in employment was always going to slow, but there is a point at which jobs and hours are growing so slowly that they raise larger concerns. We do not want to see the kind of slowing that precedes and leads to recession. Ideally hours and employment are growing at least proportionally to what demographic and population trends imply. It looks like that is either no longer the case, or only marginally so.

The unemployment rate is one way to compare demand and supply, since it reflects the balance between employed people and labor force participants who are not employed.

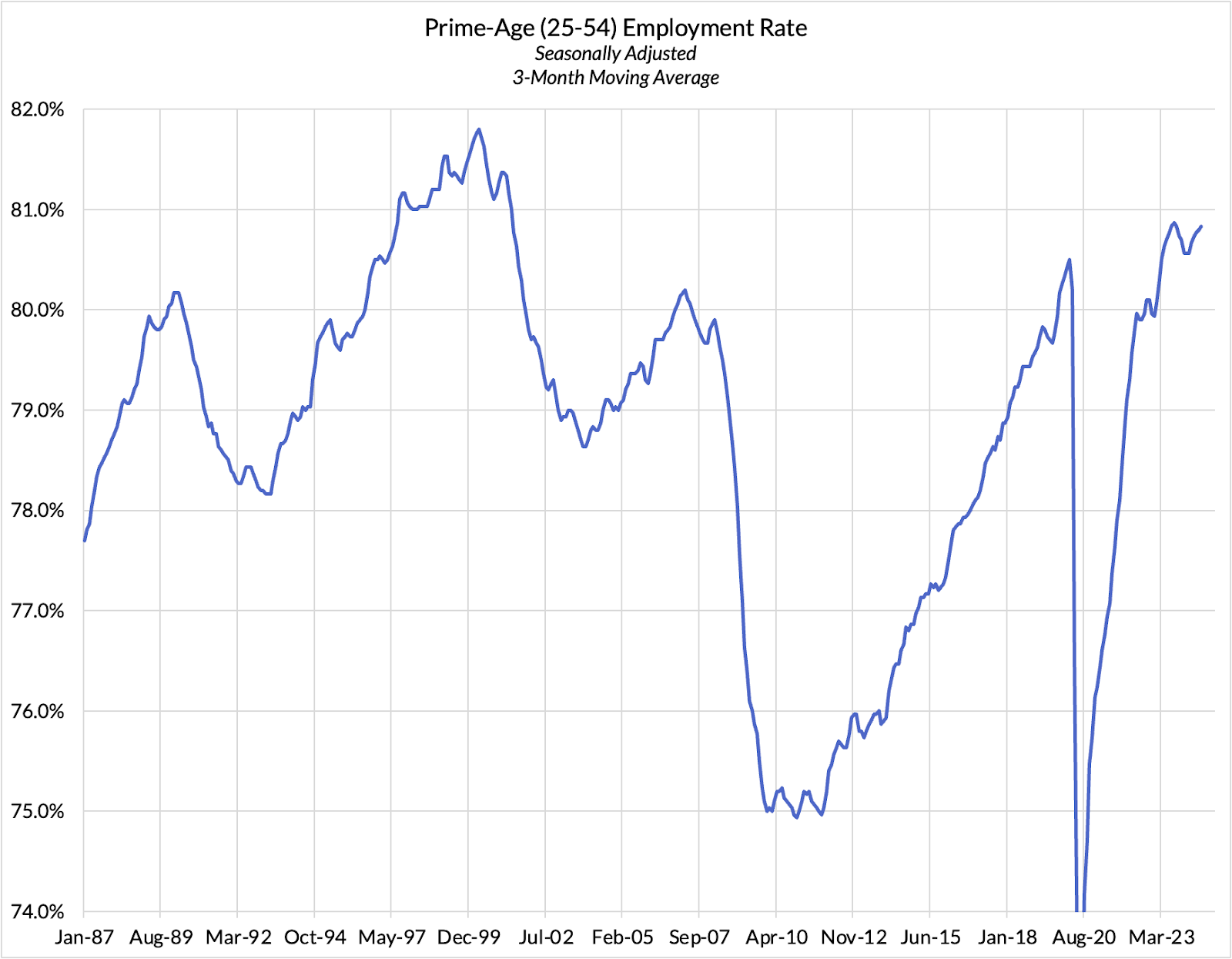

The rise in the unemployment rate has been largely driven by a rise in the number of non-employed who are now being counted as within the labor force. Prime-age 25-54 labor participation rates, which naturally adjust for the aging of the population, reached quarter-century highs in July.

This contrasts with what normally happens as recessions take steam: participation rates typically underperform, and despite that, unemployment rises because employment slows or contracts. That might be a key reason why this time’s unemployment rate increase is not so ominous, but it is still a major piece of evidence that points to a labor market that is now loosening relative to the supply-side.

The level of labor force participation is a tenuous number to measure. It’s hard for people who are not employed to easily identify whether they should be counted within or outside the labor force. For that reason, it’s better to look at more measurable outcomes: who’s employed and compare that to the population. After accounting for the aging of the population, we see that for the population in their prime working years (25-54), employment has gone sideways for 4-5 quarters.

Even though the prime-age employment rate is not obviously declining, the fact that it is no longer rising is itself a fact of note. It suggests that job growth has clearly slowed down, relative to the previous above-population-growth pace.

Historically, a 4-quarter flatlining in prime-age employment rates for all sexes or even individually, for men and women, are warning signs. Two things typically happen subsequently: either (1) a recession materializes and employment rates fall further or (2) policy interventions serve to stabilize the labor market and prevent it from falling into contraction.

Beginning the process of normalizing policy rates would be prudent for ensuring that the current slowdown does not translate into gratuitous labor market slack.

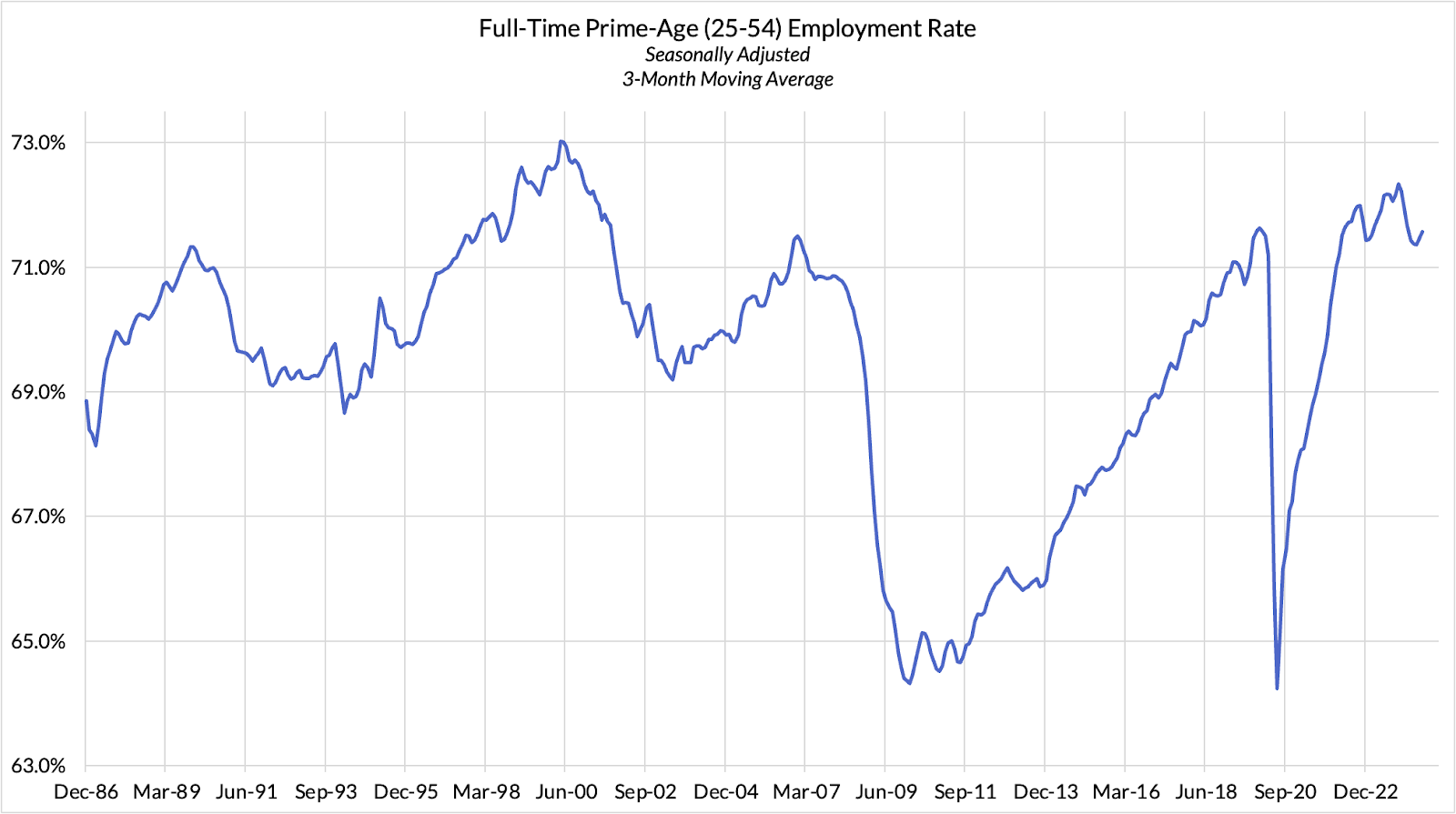

The Prime-Age Employment Rate misses the fact that hours worked per person is also dynamic. Hours can be cut for a given job, or else the composition of jobs created can tilt towards lower- or higher-hour jobs. While it is more volatile, the full-time subcategory of the Prime-Age Employment Rate suggests a less rosy picture.

This fact also matches what we’re seeing in the Establishment Survey: the average workweek is declining as lower-hour jobs represent a higher share of net job growth.

If we could apply a hypothetical hours-adjustment to the prime-age employment rate, we would see that the labor market is loosening relative to trends in population, age demographics, and available hours. Thus the labor market has more than just reverted back to balance. Avoiding further cooling from here should be a policy priority.

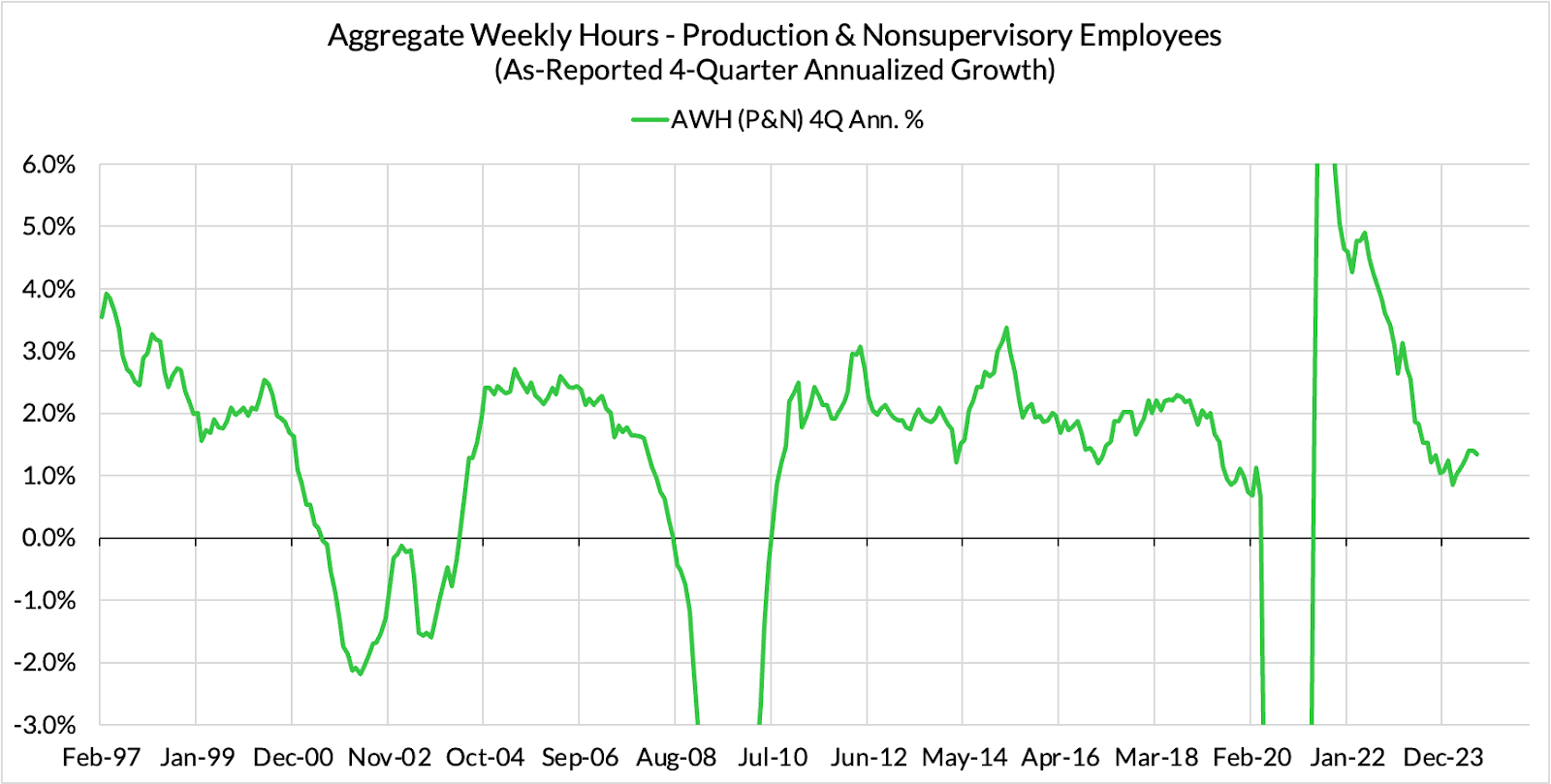

As discussed previously, the establishment survey favors the view that on an hours-adjusted basis, labor takeup has not been all that strong of late. While hours growth is running at a tolerable non-recessionary pace, it’s not obvious that it’s keeping pace with dynamic forces supporting working age population growth now. Nonfarm payroll growth has looked optically strong but aggregate working hours are growing at some of the slowest speeds outside of the last two recessions.

We are not convinced that immigration is playing such a dominant role in shaping macro labor market dynamics, but it is interesting that it is the favored reason for stronger payroll growth. If that favored hypothesis is right, then it is all the more puzzling why immigration is not providing a visible boost to hours growth in the same survey. It’s possible that immigration is boosting the population-adjusted breakeven for job growth and hours growth, but if that’s true, then the downward benchmark revisions to nonfarm payrolls compounds the pre-existing softness in hours data. The labor market has more than rebalanced. Hours growth and employment growth have underperformed labor supply growth.

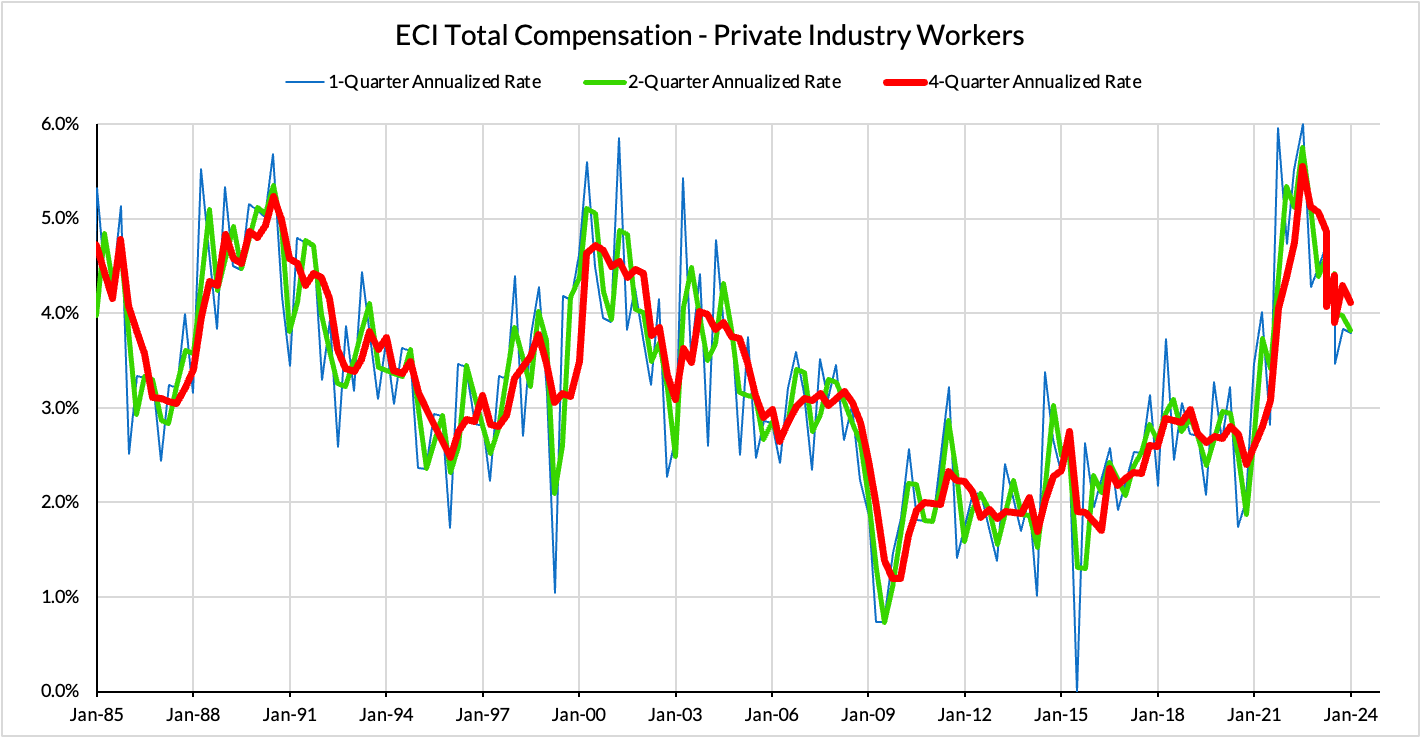

Our most robust measure of labor costs comes from the Employment Cost Index, which we received for Q2 a few weeks ago on the day of the July FOMC meeting. The data there suggested that wage and compensation growth are running somewhere between 3.5-4.2%. That number is lower than prior growth rates but still higher than the 2019 outcomes that preceded the pandemic.

Despite wage growth running marginally stronger than pre-pandemic outcomes, the case for wage growth proving to be inflationary is still weak. Wage growth ultimately has to be compared against productivity outcomes–now consistently over 2% on a year-over-year basis for several quarters–and the inflation target the Fed desires (2%).

There are conventional reasons for believing in such a comparison, but for us, it’s a simpler question: can the economy’s productive capacity support the income and consumer spending that flows from wage growth (and job growth). On that score, the labor market has more than rebalanced.

Prior to the pandemic, charitable estimates of the trend in labor productivity growth were around 1.4-1.5%, a relatively mediocre outcome. Yet on a year-over-year basis, productivity has grown above 2% for four consecutive quarters and now sits at 2.6%. On a quarterly basis, productivity has grown above a 2% annualized pace for six out of the last eight quarters. The elevated pace of productivity growth has persisted long enough to no longer be cast aside as a mere fluke. More importantly, it implies that 4-4.6% wage growth is closer to the “inflation breakeven” and that current rates of wage growth might even prove marginally disinflationary.

We also know that some of the likely revisions to productivity growth in the coming months and quarters. The downward revisions to nonfarm payroll employment and hours, and the likely upward revisions to real GDP over the last five years, the post-pandemic productivity trend is likely to look much stronger once the BEA announces its annual benchmark revision in September 2024 and the BLS formalizes its benchmark revision of the nonfarm payroll data in Q1 of 2025.

For example, real nonresidential fixed investment in structures are likely to be revised up substantially in 2022 and 2023, thereby lifting up the trend in real GDP and real output per hour.

Meanwhile, the much-discussed preliminary benchmark revisions to nonfarm payrolls are likely to yield a similar downward revision to hours worked and upward revision to productivity as we saw occur between August 2019 and early 2020.

When all is said and done with the revisions, even 4-4.5% wage growth may not prove inherently inflationary relative to a 2% inflation target. Even if we receive less favorable revisions than currently anticipated, the current pace of wage growth implied by the Employment Cost Index is now past the range of outcomes consistent with a balanced labor market. Productivity growth is showing signs of outstripping its pre-pandemic trend, and the Fed needs to start showing more openness to the idea that potential GDP growth might be higher now.

The Nexus Between The Labor Market and Inflation Nexus Suggests Current Labor Markets Support Further Inflation Reduction Now

Slower labor income growth reliably coincides with a slower pace of nominal consumer spending growth. While realized rates of consumer spending growth have held up better of late, they are due for further slowing and inducing deeper recession risk the longer the labor market continues to slow.

The trends in jobs and wages, judged by the least vulnerable-to-revision measures, are already at a place where they are not keeping up with conservative estimates of supply-side trends (and would on their own imply rate cuts under our preferred framework for Fed policy).

It’s worth noting that the measures of labor market flows used for guiding our understanding of net job growth and wage growth also signal slowing. The gross hiring rate continues to fall and is now all the way back to early 2010s levels.

Meanwhile, voluntary job-switching has also abated and put less pressure on employers to raise wages to hang on to their existing workforce. With the appropriate lags, the fall in job-switching rates are also likely to yield lower rates of nominal wage growth.

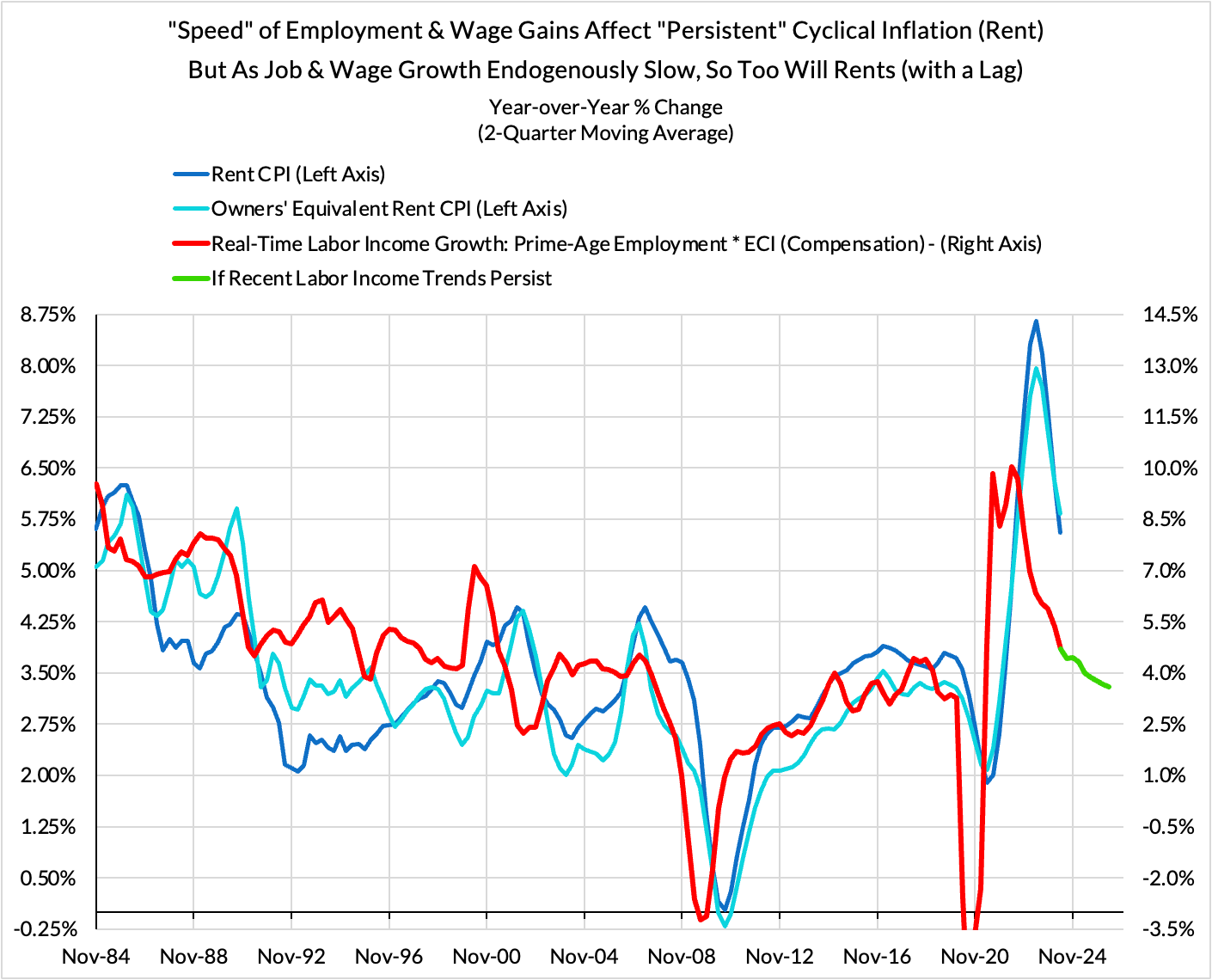

The most relevant component by which the labor market is relevant to inflation runs through the willingness to spend on rent. Rent and owners’ equivalent rent (OER) inflation respond with reasonable reliability to the growth rate of jobs and wages. When job growth and wage growth run strong, housing inflation can bulge due to its local supply inelasticity.

Housing is a prominent example, but there are other examples of how inflation data lag fundamental developments. The good news is that even on other lagging components, like the Fed’s famed ‘supercore’ nonhousing services aggregate, inflation is normalizing there too

The labor market has already rebalanced. And short-term data trends suggest it has now cooled and loosened even further than what a balanced labor market would look like. Whether you take an inflation- or supply-demand-oriented view of the labor market, we have now reached the point where the Fed should not be aiming for any more cooling from here. Any more slowing would meaningfully and gratuitously aggravate recession risk and be directly at odds with their dual mandate objectives for maximum employment and price stability.

Even if the unemployment rate does not look spooky after the August jobs report, the Fed needs to begin backing away from its restrictive policy stance. Job growth, wage growth, and forward-looking inflation dynamics all suggest that the Fed should be leaning towards supporting the economy, not slowing it.