The Fed is arguing that inflation is driven by the cost-push impacts of wage growth on service prices. This is a traditional view, but the pandemic recovery has been anything but textbook. In our view, the primary nexus is a demand-pull relationship. The core question for the Fed ought to be how gross labor income growth—that is, the cumulative effect of both job growth and wage increases—translates into nominal consumer spending growth. While wage growth plays a role in both views, the reason for the distinction is critical:

- If we follow the (wage-determined) cost-push view, the flaws and lags embedded in real-time wage growth measures take on an outsized relevance to the inflation outlook.

- If we follow the (gross labor income-determined) demand-pull view, we are able to temper these flaws and lags with more reliable observations of growth in employment and nominal spending.

What should policymakers do if wage growth indicators are hot due to distortions, lags, or simple statistical noise, rather than underlying strength? Based on recent statements from Fed leadership, the only other dynamic that could get the Fed to rethink their tightening campaign is if a recessionary rise in unemployment has already materialized.

The Fed is relying on lagging and flawed dynamics to constrain their tightening efforts. This unnecessarily puts the labor market and the US economy at excessive risk of recession.

Since wage growth measures are subject to flaws and lags, the demand-pull view can be monitored more robustly than the cost-push view in real-time. More importantly, the non-wage data needed to force a pivot under the demand-pull view does not turn on first seeing mass joblessness. If the demand-pull view is right, then the Fed should be taking more seriously the disinflationary implications of slowing growth in employment, gross labor income, and consumer spending, all of which can be observed more reliably than wages and all of which are occurring already.

To address the premise of this piece, here's a run-down of the flaws across major wage indicators:

- Average hourly earnings is subject to composition biases and vulnerable to drastic revisions. It is just a simple ratio of total dollars spent on payroll by total hours worked. A layoff of a low-wage worker mechanically raises wage growth in this measure, leading to spurious signals at critical inflection points in the business cycle.

- The Atlanta Fed Wage Growth Tracker is subject to selection biases, imperfect controls, lagged year-over-year measurements, and small sample size. It only looks at the sample of already-employed and continuously-employed persons. It does not control for the occupational task they are performing (and the wage premium associated with additional experience when performing that task).

- The Employment Cost Index tends to be superior in terms of how it avoids the flaws in the previous two measures, but it is only released at a quarterly frequency and can be subject to varying lags. This has been a problem in evaluating recessions in the past. For example, ECI remained strong even as nominal GDP and employment growth dropped off substantially in 2001 and 2002. Given the substantial degree of sectoral shifts in the post-pandemic labor market, ECI's fixed-weight Laspeyres methodology could leave it vulnerable to similarly long lags now.

- The Indeed Wage Growth Tracker should be superior to ECI in terms of timeliness and even possibly the scale of controls, all without sacrificing sample size. This measure, which tracks advertised wages in job postings at Indeed, is also likely more indicative of marginal wage costs than payments to already-employed workers. But even here, new biases could potentially emerge and the measure is relatively young, only being available over a short history.

The Fed’s job is to interpret imperfect information in real-time. Every observed data point has some methodological flaw, but some data is more reliable for real-time purposes than others. But what do you do if a critical input for your causal view of inflation—whether cost-push or demand-pull—is unobservable?

The Fed is overly focused on the wage Phillips Curve. If nominal wage growth comes in strong—even if for ultimately faulty reasons—the Fed seems unwilling to settle for anything less than a recessionary rise in the unemployment rate. In their view, this is virtually the only way “to bring the labor market back into balance.” Perhaps a fortuitous, non-recessionary, reversion in job openings could provide Chair Powell enough relief to back off of an aggressive tightening policy. But even this kind of data is lousy and unreliable to lean on, for well-documented methodological and empirical reasons. The Fed is effectively taking a binary view: either ECI tracks down quickly or else the Fed will continue to aim for recessionary increases in unemployment.

For us, there is a healthier middle ground. There exists macroeconomic data other than wages that give us clues about the underlying trajectory of household income and spending growth (and by extension, wage growth too!).

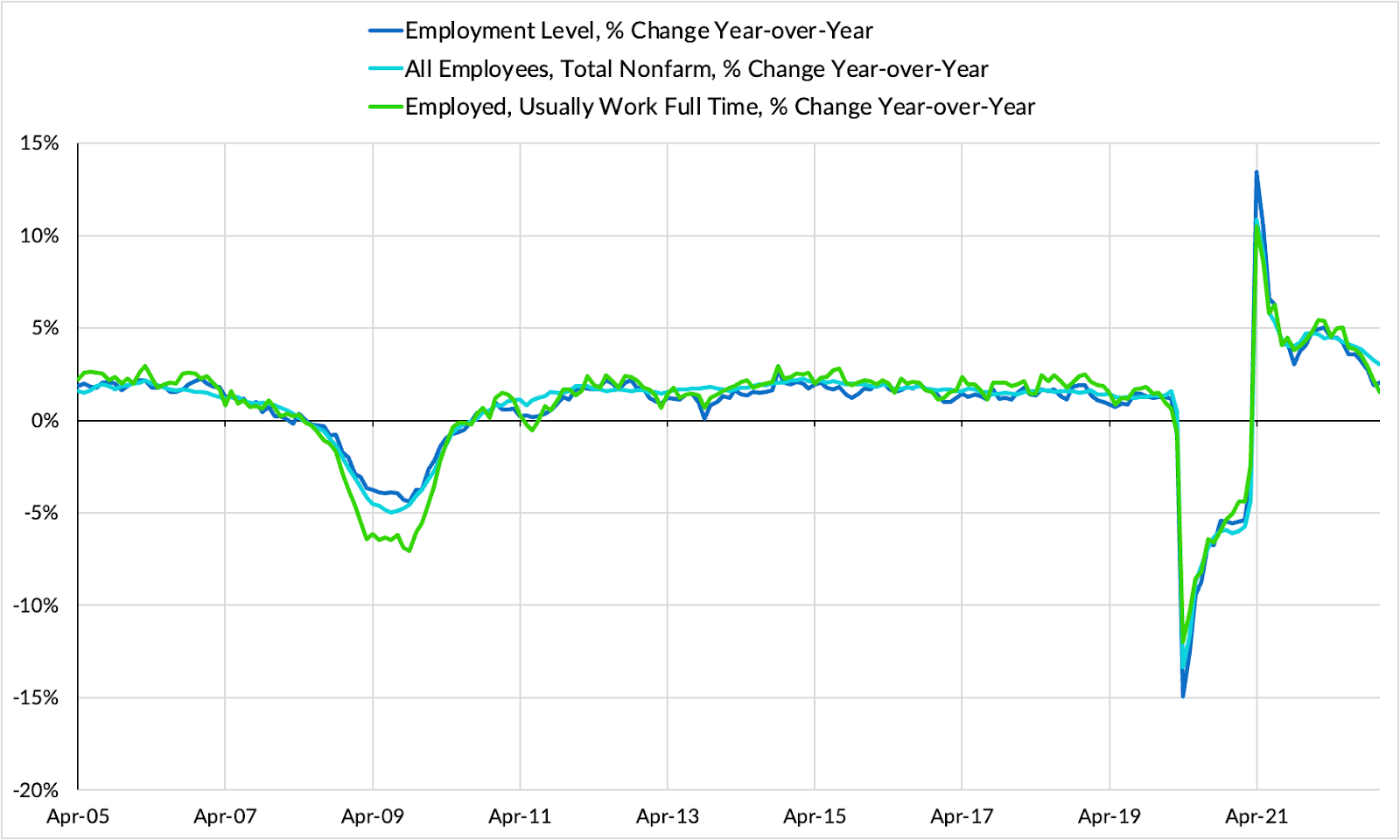

- Job growth. For households that shift to earning an additional market income, whether that be the only paycheck or a second check, the income- and consumption-enhancing effects are nonlinear and deserve to be taken seriously. The demand-pull perspective is arguably more serious about the inflationary implications of job growth than more hawkish commentators or policymakers at the Fed, who often see job growth as primarily adding to the “supply” side of the equation. In reality, net employment gains add at the margin to nominal consumption, real consumption, and consumer prices.

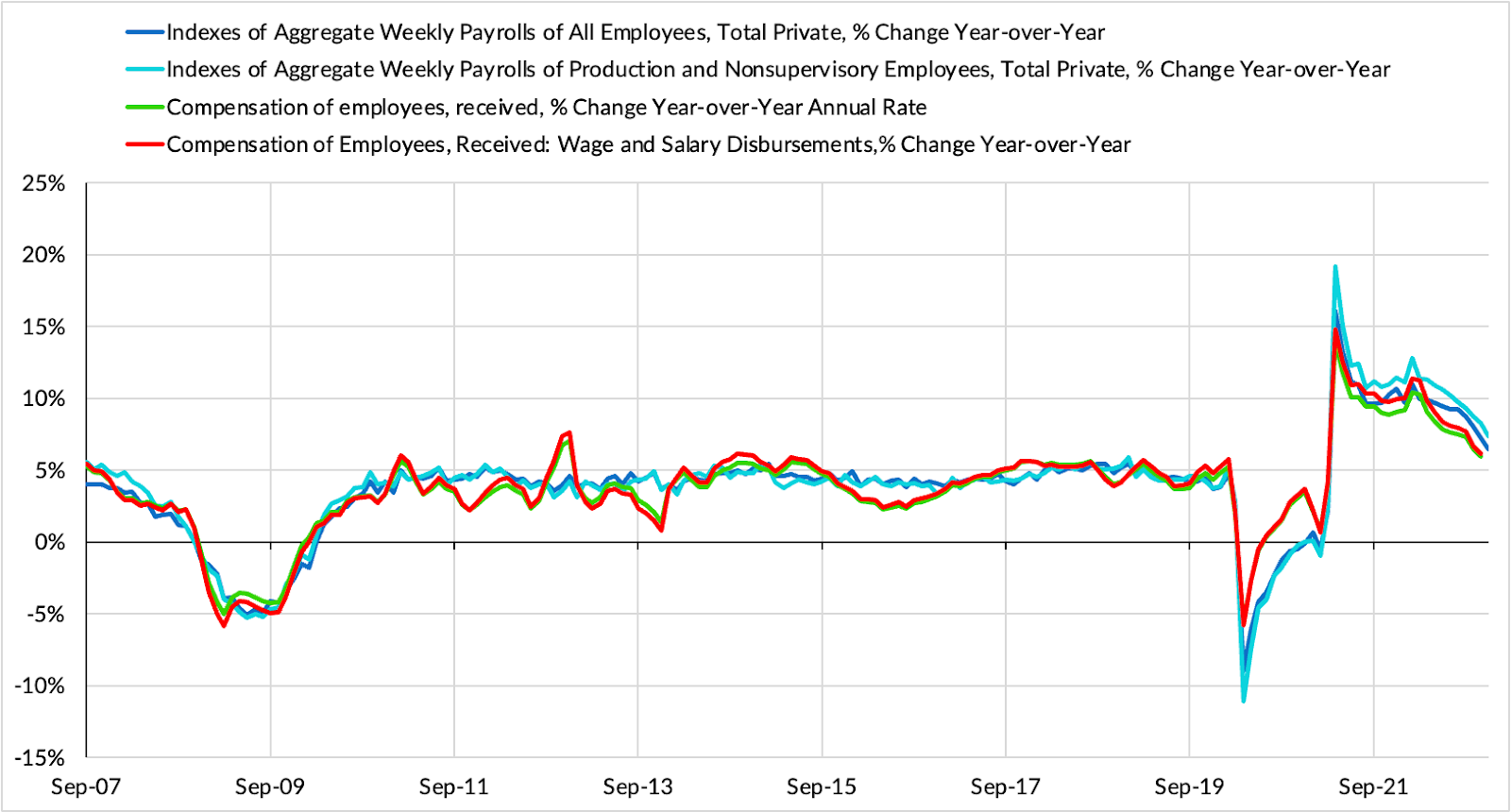

- Gross labor income growth. While we don't have perfect measures of gross labor income growth, they are still better than the corresponding measures of wage growth. We can relatively directly observe total dollar spending on wages and labor compensation in the establishment survey (used for calculating nonfarm payrolls and average hourly earnings) and the personal income release. These estimates are still subject to substantial revisions, but they cut through the composition distortion that play havoc with average hourly earnings.

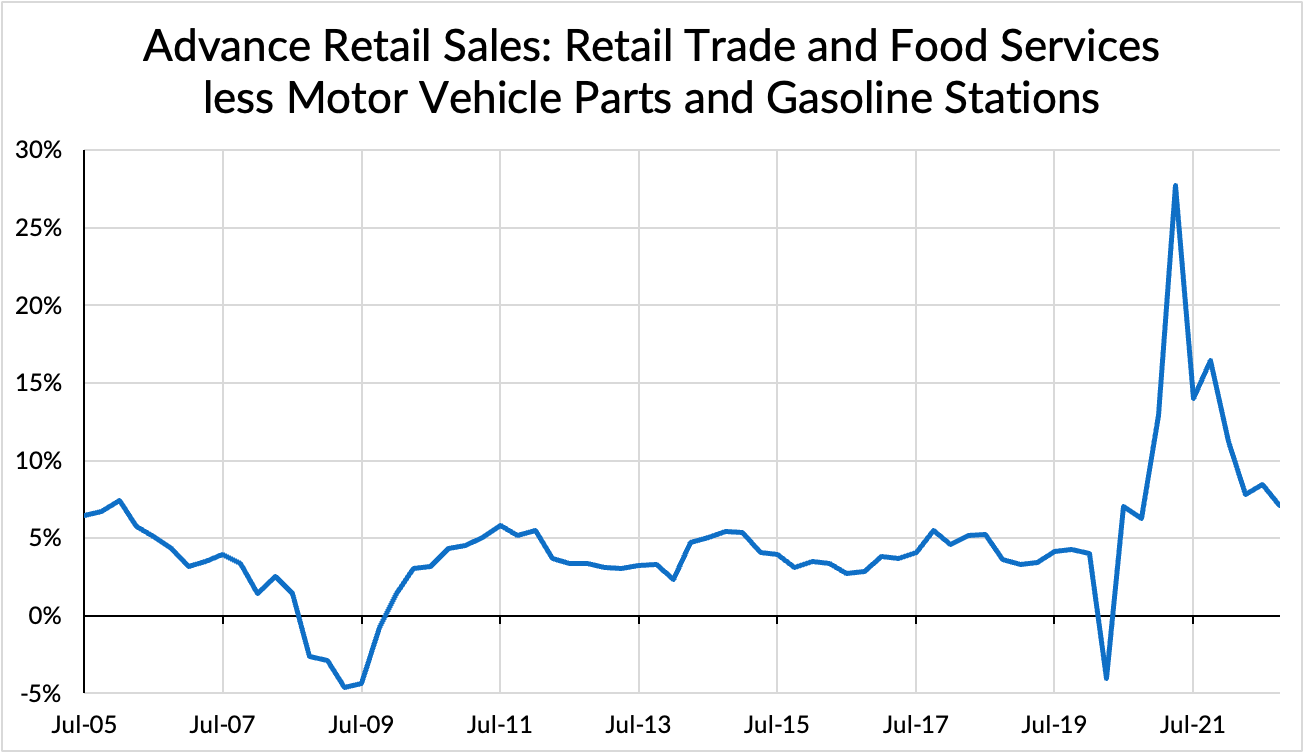

- Nominal consumption growth (including retail sales): Like gross labor income, measures of nominal consumption are superior to wages, even if they are also not perfect. We get our first read on cyclical consumer spending growth from the advanced retail sales release, and a more comprehensive estimate from the personal income release. These estimates can be 1) volatile, 2) subject to substantial revisions, and 3) embed residual seasonality issues. Nevertheless, the year-over-year growth rate of the non-volatile components of retail sales still offers a helpful and timely guide to the trends in nominal spending and income growth.

Right now the data from all three of these metrics are confirming a story of inflation cooling off through the demand-side labor market mechanism:

- Employment is decelerating back to the pre-pandemic growth rate.

- Gross labor income growth is decelerating back to the pre-pandemic growth rate.

- Nominal consumption growth is decelerating back to the pre-pandemic growth rate.

If these decelerating dynamics hold up and trend nominal growth reverts fully back to the pre-pandemic pace, inflation risks should be lowered correspondingly. For a permanent and meaningful regime shift to inflation trends, the pace of gross nominal income and spending growth almost necessarily should shift upward too. Perhaps some of these local trends reverse in the coming months and quarters, but the data is currently validating the idea that demand-side inflation pressures are already cooling. [The charts below are year-over-year growth rates and should ease further in the coming months and quarters given upcoming base-effects]